- BDI retreats after four sessions of gains

- Panamax and Supramax extend positive momentum

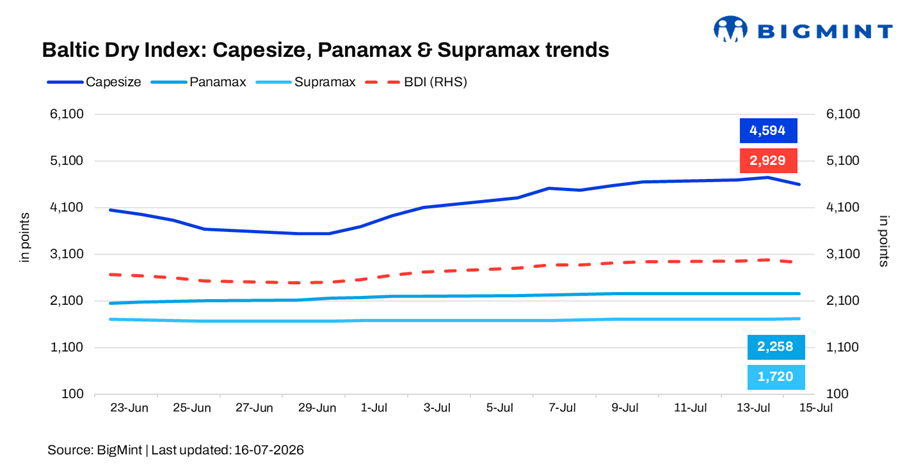

The Baltic Exchange Dry Bulk Index (BDI) declined 1.7% d-o-d (51 points) to 2,929 points on 15 July 2026, snapping a four-day rally as weakness in the Capesize segment outweighed continued gains in the smaller vessel segments. While Capesize rates eased after a strong rally, Panamax and Supramax segments continued to strengthen, indicating resilient demand across agricultural and minor bulk trades.

Overall freight sentiment remains cautiously optimistic as iron ore shipments from Australia, consistent cargo enquiries, and tighter vessel availability continue to provide support to the dry bulk market.

Segment-wise Performance

- Capesize (BCI): Down 3.3% (157 points) to 4,594 points, ending a four-session advance as profit-taking and softer fixture activity weighed on the market. Despite the decline, underlying sentiment remained constructive, supported by robust iron ore exports and tighter Pacific tonnage.

- Panamax (BPI): Up 0.3% (7 points) to 2,258 points, supported by stable coal and grain cargo demand across both Atlantic and Pacific basins.

- Supramax (BSI): Rose 0.6% (10 points) to 1,720 points, marking its highest level since August 2022, driven by sustained demand for minor bulks, steel products, fertilizers, and grains across regional trade routes.

Outlook

The index is expected to remain firm but volatile in the near term, supported by healthy iron ore and coal shipments, particularly from Australia and Brazil, along with sustained grain exports. Seasonal cargo demand and improving vessel utilisation, especially in the Capesize segment, are likely to keep overall freight sentiment positive.

However, the pace of gains may be capped by fluctuations in Chinese steel demand, changing commodity trade flows, fleet availability, and geopolitical developments. While short-term corrections are possible after the recent rally, the broader outlook remains constructive as long as seaborne bulk cargo volumes continue to support vessel demand.

Leave a Reply