- Softer coal, iron ore inquiries, higher vessel supply pressure Capesize earnings

- Supramax hits near four-year high, while Panamax remains largely stable

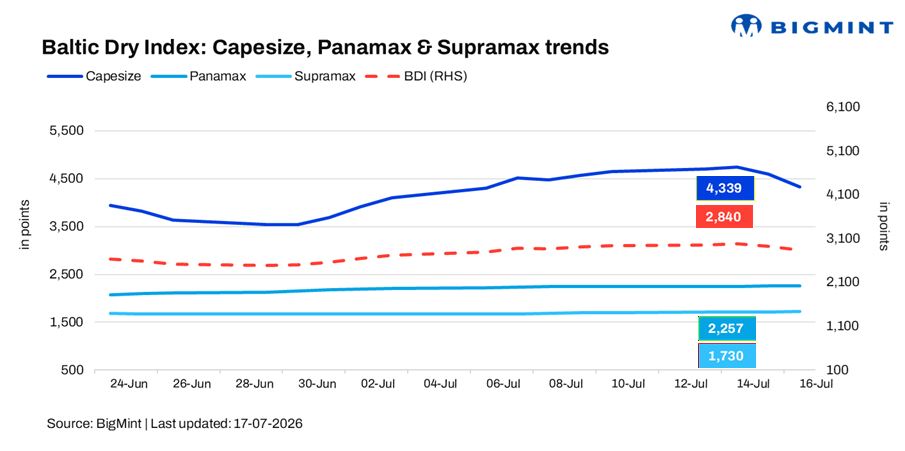

The Baltic Exchange Dry Bulk Index (BDI) declined for the second consecutive session on 16 July 2026, falling 2.9% (89 points) to 2,840 points, its lowest level since 6 July. The decline was primarily driven by weaker Capesize earnings, as softer iron ore and coal cargo enquiries and improved vessel availability weighed on spot freights, offsetting the relatively stable performance of smaller vessel segments.

Despite the recent correction, overall freights remain above those seen earlier in the month, indicating that underlying demand across key dry bulk trade routes continues to provide support. While easing geopolitical tensions have reduced some of the risk premium in freight markets, steady commodity trade flows have helped limit a sharper decline in the index.

Segment-wise performance

- Baltic Capesize Index (BCI): BCI declined 5.4% (255 points) d-o-d to 4,339 points on 16 July 2026, marking its lowest level in over a week. The sharp decline was primarily driven by softer spot earnings on key iron ore and coal trade routes, particularly from Brazil and Australia to China, amid easing cargo enquiries and increased vessel availability. The weakness in the Capesize segment was the main factor behind the broader decline in the Baltic Dry Index during the session.

- Baltic Panamax Index (BPI): BPI edged down by 0.04% (1 point) d-o-d to 2,257 points on 16 July 2026. The index remained largely stable as balanced cargo demand across grain, coal, and minor bulk trades offset limited fluctuations in vessel availability.

- Baltic Supramax Index (BSI): BSI rose 0.6% (10 points) d-o-d to 1,730 points on 16 July 2026, its highest level since August 2022. The gains were supported by sustained demand for minor bulk cargoes, including steel products, fertilisers, cement, and agricultural commodities, coupled with healthy vessel utilisation across key trading regions.

Outlook

The Baltic Dry Index is expected to remain volatile in the near term, with the Capesize segment continuing to drive overall market direction. Softer iron ore cargo enquiries and improving vessel availability may keep pressure on freights, although healthy underlying commodity demand should limit sharper declines.

Meanwhile, steady grain, coal, and minor bulk trade is likely to support the Panamax and Supramax segments, helping cushion the downside for the broader dry bulk market.

Leave a Reply