- Slowing trades across key commodities impact freight market

- Panamax strength tempers broader freight caution

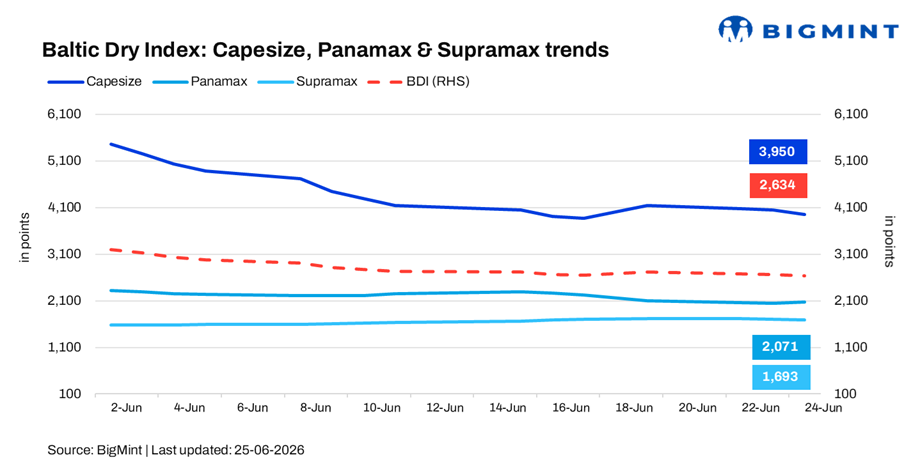

The Baltic Exchange’s Dry Bulk Index (BDI) declined by 1.24% (33 points) d-o-d to 2,634 points on 24 June 2026, marking its third consecutive daily decline and falling to its lowest level in around two months.

The downturn was driven by softer Capesize earnings and weaker Supramax activity, which more than offset continued strength in the Panamax segment. The decline reflects a more cautious sentiment across the dry bulk market as slowing activity in key commodity trades weighed on overall freight performance.

Segment-wise performance

- Capesize: The Capesize index fell 2.4% (96 points) to 3,950 points, its lowest level since 18 June, amid softer iron ore and coal fixtures and subdued chartering activity on key long-haul routes.

- Panamax: The Panamax index gained 1.3% (26 points) to 2,071 points, supported by steady coal and grain cargo demand, particularly across Atlantic and regional grain trades.

- Supramax: The Supramax index edged down 0.7% (12 points) to 1,693 points, reflecting limited fresh enquiries and slower fixture activity in the minor bulk segment.

Outlook

Baltic Dry Index sentiment is expected to remain cautious, with further downside pressure likely as persistent weakness in the Capesize segment continues to outweigh support from stronger Panamax earnings.

Market activity remains below historical averages as participants assess the long-term impact of the recent US-Iran de-escalation. While easing geopolitical tensions have improved confidence and reduced concerns over trade disruptions, a sustained recovery in the BDI will likely require stronger iron ore exports, firmer commodity demand, and a broader improvement in global industrial activity.

Leave a Reply