- China’s strong demand drove Australia’s June export rebound and H1 growth

- Weak steel demand limited PHCC price gains despite tight supply

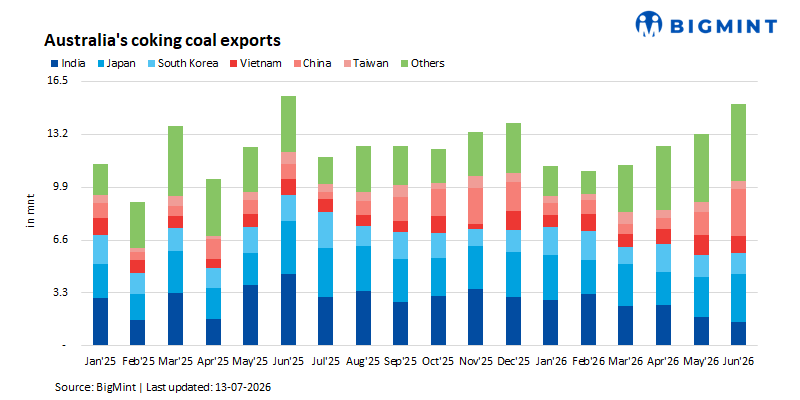

Australia’s coking coal exports rebounded strongly in June 2026, rising 14% month-on-month (m-o-m) to 15.06 million tonnes (mnt) from 13.22 mnt in May. The recovery was driven by stronger procurement from key Asian steel-producing nations, improved cargo availability and smoother port operations following earlier shipment disruptions.

However, exports remained 3% lower year-on-year (y-o-y) compared with 15.6 mnt in June 2025, reflecting relatively softer demand from some traditional importing markets. On a cumulative basis, exports reached 74.1 mnt during January-June 2026, up 2.4% y-o-y from 72.4 mnt in the corresponding period last year, highlighting resilient global demand for premium metallurgical coal despite uneven regional buying patterns.

China drives growth while Indian demand weakens

Import demand across Australia’s major Asian customers remained mixed during June. China emerged as the key growth driver, with imports surging 99% m-o-m to 2.93 mnt and 199% y-o-y, supported by stronger procurement amid domestic supply constraints, improved demand from steelmakers and the competitive pricing of Australian cargoes.

In contrast, India’s imports declined sharply by 52% m-o-m to 1.47 mnt, down 55% y-o-y, primarily due to elevated imported coking coal prices, comfortable raw material inventories at steel mills, softer domestic steel prices and cautious procurement strategies. Japan’s imports increased 12% m-o-m to 3.03 mnt, supported by stable steel production and routine inventory replenishment.

Meanwhile, South Korea’s imports fell 5% m-o-m to 1.28 mnt, down 19% y-o-y, reflecting weaker steel margins and restrained raw material purchasing. Vietnam’s imports declined 25% m-o-m to 1.05 mnt, although they remained 30% higher y-o-y, while Taiwan’s imports eased 12% m-o-m to 0.54 mnt, declining 27% y-o-y amid subdued steel demand.

H1 2026 exports supported by strong Asian demand

During the first half (Jan-Jun) of 2026, Australia’s coking coal exports increased 2.4% y-o-y to 74.1 mnt, supported by sustained demand from major Asian steel-producing economies. China recorded the strongest growth, with imports rising 43% to 7.5 mnt as domestic supply constraints and favourable pricing enhanced the competitiveness of Australian material.

Exports to Japan (+12.4% to 15.4 mnt), Vietnam (+13.2% to 6 mnt) and Taiwan (+9.6% to 3.1 mnt) also increased, reflecting stable steel production and continued preference for premium-quality coking coal.

Conversely, shipments to India declined 10% to 16.5 mnt, primarily due to cautious procurement by steel mills, softer steel market conditions, increased met coke imports and greater sourcing diversification. Exports to South Korea remained broadly stable at 9.1 mnt, while shipments to other destinations increased 19% to 21.1 mnt, contributing to the overall growth in Australia’s export volumes.

PHCC prices strengthen despite uneven trade flows

Australian Premium Hard Coking Coal (PHCC) prices increased by $4/t m-o-m during June 2026, supported by tight domestic coking coal availability in China following accidents at Shanxi leading to mine suspension, supply-side constraints and stronger buying interest from Chinese consumers. However, gains remained limited by weaker steel prices and cautious procurement across several importing markets.

Major coal terminals report higher throughput

Export performance across Australia’s major coal terminals improved during June, reflecting smoother logistics, better vessel scheduling and higher cargo nominations. Dalrymple Bay Coal Terminal (DBCT) recorded a 22% m-o-m increase in shipments to 5.15 mnt, supported by improved vessel turnaround times.

Gladstone and Hay Point exported 4.41 mnt and 3.84 mnt, up 7% and 1% m-o-m, respectively, driven by higher loading activity. Abbot Point shipments rose 37% m-o-m to 1.11 mnt, while Port Kembla registered the strongest growth, with exports increasing 146% m-o-m to 0.43 mnt, reflecting the normalisation of shipment schedules following lower dispatches in the previous month.

Outlook

Australia’s coking coal exports are expected to remain supported by resilient Chinese demand, stable Japanese procurement and improved export logistics. However, subdued steel market fundamentals, cautious buying by Indian and South Korean steelmakers, and weaker global steel margins may continue to constrain seaborne demand. Premium hard coking coal prices are likely to remain supported by China’s supply-side constraints, although a sustained market recovery will depend on stronger global steel production and consumption.

Leave a Reply