- Exports to India plunge by over 32% m-o-m

- Market recovery hinges on Chinese, Indian demand

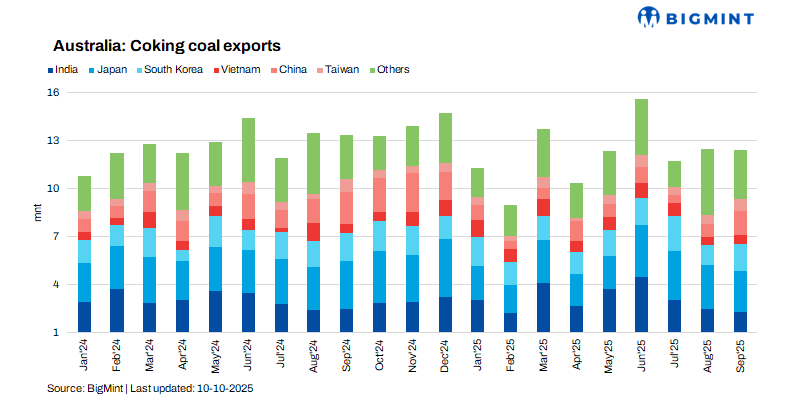

Australia’s coking coal exports held largely steady in September 2025, totaling 12.46 million tonnes (mnt), indicating a pause in the recent volatility in trade flows.

While monthly exports remained stable, the broader trend for 2025 continues to point to a contraction, reflecting subdued steel production and cautious raw material procurement by major Asian buyers.

Year-to-date volumes drop

Cumulative exports during January-September 2025 stood at 109.1 mnt, marking a 4.6% year-on-year (y-o-y) decline from 114.3 mnt during the same period in 2024. The decline highlights the enduring softness in global steel demand, which has kept end-users across Asia restrained in their buying strategies amid uncertain macroeconomic conditions and volatile margins.

China, South Korea drive partial recovery

Export distribution data showed a sharp divergence in buying patterns across key Asian markets. Shipments to India, a major destination for Australian coking coal, plunged 32.4% m-o-m to 2.33 mnt amid lower steel output and high inventories.

Japan also reduced intake by 9% to 2.52 mnt, while Vietnam’s imports declined 18.9% to 0.57 mnt due to weak margins and restrained production.

Conversely, China drove export stability, with volumes surging 69.7% m-o-m to 1.51 mnt on stronger mill operations and improved coke margins. South Korea and Taiwan followed suit, with imports up 37.7% and 29.7%, respectively, supported by restocking and stable output.

The rebound in Northeast Asian demand partially offset weakness in South and Southeast Asia, indicating a gradual rebalancing in regional trade flows.

Mixed port performance reflects trade shifts

Australian port activity in September reflected mixed trade dynamics across key terminals. Dalrymple Bay Coal Terminal (DBCT) saw shipments rise 2.2% to 4.05 mnt, supported by steady vessel arrivals and firm Chinese demand, while Hay Point declined 2.7% to 2.93 mnt amid lower loadings for India and Japan. Gladstone Port exports fell 3.6% to 3.91 mnt on weaker Northeast Asian demand, whereas Abbot Point inched up 1.6% to 1.14 mnt.

Among smaller ports, Newcastle recorded a sharp 54% increase to 0.12 mnt, and Port Kembla led gains with a 33.6% rise to 0.32 mnt, driven by higher metallurgical coal shipments to niche Asian buyers. The mixed performance highlights evolving trade patterns and the flexibility of Australian miners in aligning exports with regional demand shifts.

Prices firm slightly amid renewed buying interest

Australian coking coal prices firmed slightly by $1/tonne (t) m-o-m in September, reflecting renewed buying interest from select Asian markets and tighter spot availability. Market participants noted that restocking demand from China and South Korea, combined with minor logistical constraints, provided limited upward support to prices.

Outlook

Australia’s coking coal market shows tentative stabilization, aided by stronger Northeast Asian demand and steady exports. Yet, subdued steel production and global uncertainties may cap recovery, with sustained Chinese demand and renewed Indian buying key to driving momentum ahead.

Leave a Reply