- Delays in Australian premium mid-vol production cap prompt cargo supply

- Tight supply, firm Indian demand support Indonesian met coke prices

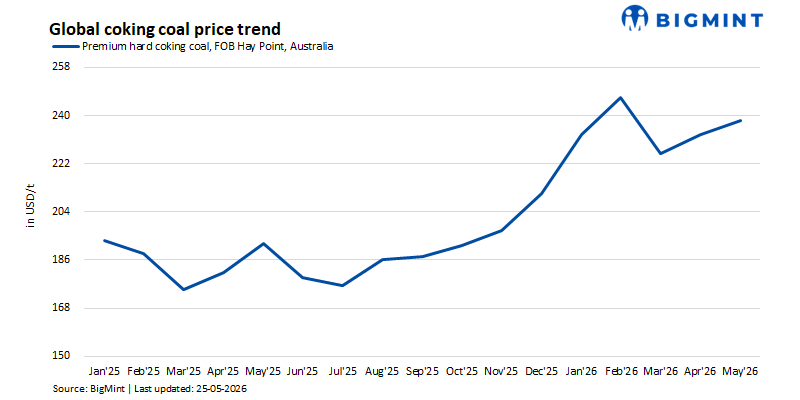

The seaborne metallurgical coal market remained broadly steady in the week ended 22 May 2026, but beneath the surface, regional signals increasingly diverged. Australian premium hard coking coal (PHCC) prices found support from persistent supply concerns and a key premium mid-vol trade, while weak Chinese buying interest and currency-led resistance from Indian buyers capped upside momentum. At the same time, the US East Coast market softened amid sluggish spot demand, even as Indonesian metallurgical coke continued to strengthen on tight availability and rising freight costs.

The market is increasingly caught between tightening supply in select origins and weakening affordability among buyers, leaving prices supported but vulnerable.

Goonyella trade anchors premium market

The premium end of the seaborne metallurgical coal market remained firm after a producer sold 75,000 t of Premium Mid-Volatility (PMV) Goonyella coal at $244/t FOB Australia for June loading on 19 May, reinforcing prevailing market strength in premium Australian grades.

The trade effectively anchored sentiment for higher-quality hard coking coal and reinforced the market’s view that supply-side constraints remain unresolved. Delays across Australian premium mid-vol production continued to limit prompt cargo availability, keeping sellers firm despite patchy buying activity.

Benchmark premium low-volatility hard coking coal (PLV HCC) prices held at around $241/t FOB Australia, remaining stable through the week. Market participants indicated that although spot buying remained cautious, miners and traders showed limited willingness to lower offers amid uncertainty around supply.

Many participants increasingly viewed the market as supply-driven rather than demand-led, particularly in the premium coal segment.

Indian buyers resist high-priced cargoes as rupee weakness bites

Indian steelmakers remained cautious in the spot market, with the depreciation of the Indian rupee against the US dollar adding pressure to procurement economics.

Indicative replacement levels for premium mid-volatility cargoes into India were heard in the high-$260s/t to mid-$270s/t CFR range, but buyers showed resistance at prevailing price levels. Instead of committing to fresh seaborne cargoes, several consumers explored stock-and-sale opportunities and lower-cost alternatives.

Despite near-term caution, underlying demand fundamentals remain relatively supportive. Mills continue to operate at healthy utilisation levels, meaning deferred purchases are likely to re-emerge later, particularly if supply tightness persists into June and July.

However, elevated freight rates and expensive dollar-denominated cargoes continue to weigh on purchasing decisions.

China weakness limits seaborne upside

In contrast to the relatively resilient Australian FOB market, sentiment in China remained notably weaker.

Domestic premium low-volatility coking coal prices in Shanxi softened during the week, with values easing to around RMB 1,550-1,600/t ($228-$235)/t ex-washplant, reducing the attractiveness of imported seaborne cargoes. At the same time, softer futures sentiment and weakening steel prices encouraged mills to remain cautious.

Chinese buyers largely refrained from forward purchases of premium seaborne cargoes, with many market participants indicating that import appetite would remain subdued unless offers corrected meaningfully lower.

Portside inventories of seaborne hard coking coal also continued to soften, adding further downward pressure on sentiment. While supply concerns in Australia prevented sharp corrections in FOB prices, the absence of strong Chinese buying continued to limit upward momentum.

US coking coal market weakens as spot demand softens

Unlike Australia, the US East Coast coking coal market came under renewed pressure during the week as weak buying interest from India and discounted competition into Turkiye weighed on sentiment.

US low-volatility hard coking coal values softened to around $194/t FOB USEC, while High Volatile A (HVA) grades declined more sharply, with tradable levels heard considerably below earlier market expectations as sellers sought to move spot cargoes.

The weakness highlighted a growing disconnect between supportive long-term fundamentals and softer near-term spot demand. Although US producers continue to benefit from favourable policy sentiment and expectations of stronger export competitiveness over time, immediate market conditions remain difficult.

For many buyers, US-origin cargoes increasingly represent a lower-cost substitute to expensive Australian premium grades, though transaction volumes remain selective.

Indonesian metallurgical coke strengthens on tight supply

The metallurgical coke market remained one of the stronger pockets of the ferrous raw materials complex, supported by tight Indonesian supply and firm Indian demand.

Indonesian 65/63 CSR blast furnace coke FOB prices strengthened to around $273/t, while delivered prices into India remained stable w-o-w, as per BigMint’s assessment. Indonesian-origin met coke was assessed at $302/t, CNF East Coast, India, supported by firmer freight costs and limited cargo availability.

Market participants indicated that several Indonesian cokeries remain effectively sold out over the coming months, allowing suppliers to maintain firm pricing.

Chinese coke prices, meanwhile, remained broadly stable, reflecting balanced supply-demand conditions and softer domestic steel market sentiment.

Russian PCI gains favour as buyers seek lower-cost options

The pulverised coal injection (PCI) market remained subdued overall, though competitively priced Russian material continued to find buyers in Asia.

Australian low-vol PCI prices held broadly stable near $157/t FOB Australia, while Russian low-vol PCI cargoes into China were heard around $143-144/t CFR river port, with at least one trade confirmed during the week.

In India, Russian mid-tier PCI continued to attract interest at around $151-153/t CFR, as steelmakers explored lower-cost feedstock alternatives to expensive premium hard coking coal.

The economics of coal blending and substitution increasingly influenced procurement strategies, particularly for buyers facing margin pressures.

Outlook

The seaborne metallurgical coal market remains balanced but increasingly fragile. Australian supply constraints continue to support premium coal prices, while weak Chinese sentiment and Indian affordability pressures prevent stronger upward momentum.

For now, the market appears stable rather than bullish. Much will depend on whether Australian supply disruptions persist into June, how far Chinese domestic coal prices soften, and whether Indian buyers return to the market after delaying purchases.

Absent a fresh supply shock, the market may struggle to sustain current highs through the second half of the quarter, particularly if steel market weakness in China intensifies.

Leave a Reply