- Australian coal prices soften amid weak demand and high inventories

- Indonesian coal remains firm due to supply constraints and producer discipline

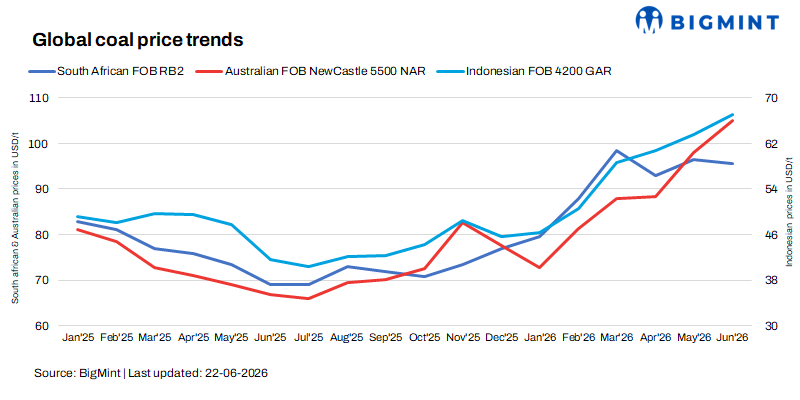

The Asian thermal coal market entered a corrective phase during the week ending June 19, with Australian high-calorific value coal surrendering part of the sharp gains recorded over the previous fortnight. The correction was driven by cautious buying, elevated inventories across Asia and softer paper markets rather than any meaningful deterioration in supply fundamentals.

FOB Newcastle 6,000 NAR July cargoes traded at $146/t, down from the $152-157/t levels recorded a week earlier. August bids retreated further to $133-140/t FOB, while sellers continued to seek $138-143/t, reflecting a market that remains divided over near-term direction.

The correction was considerably sharper in the 5,500 NAR segment.

After attracting bids around $107-108/t only a week earlier, July Panamax cargoes changed hands at just $94-95/t FOB, representing a decline of almost 12% in one week. The absence of firm buying interest and the willingness of sellers to transact below previously indicated levels suggest that speculative support has largely disappeared from this segment.

Indonesian coal proves more resilient

In contrast, Indonesian low-rank coal continued to soften only gradually.

Multiple trades for 4,200 GAR coal were concluded between $66.50-68/t FOB, compared with approximately $70.50/tthe previous week. The decline has been orderly rather than disorderly, reflecting continuing supply-side support.

Although bids have weakened, miners remain reluctant to reduce offers aggressively amid ongoing uncertainty surrounding RKAB production approvals and Indonesia’s Domestic Market Obligation (DMO) requirements.

Government discussions regarding revisions to production quotas to address PLN’s estimated 20 million tonne supply shortfall continue to dominate market sentiment. Until greater clarity emerges, producers appear comfortable restricting spot availability rather than chasing lower prices.

Higher CV Indonesian coal has remained considerably more stable, with 5,500 GAR material trading at $107/t FOB, highlighting the differentiated behaviour across quality segments.

China continues to dictate regional sentiment

China remains the dominant influence on Asian thermal coal pricing.

The domestic market continues to exhibit what traders describe as a “hot production area, cold port market” structure.

Safety inspections and production constraints have kept mine-mouth prices relatively firm, while portside trading activity remains subdued due to comfortable utility inventories and ample long-term contract supplies.

Qinhuangdao FOB markers have begun to roll over after peaking in early June.

The benchmark 5,500 NAR marker declined from $127.25/t to $126.20/t, while 6,000 NAR eased from $142.46/t to $140.75/t during the week.

The moderation reflects abundant utility stocks rather than weak structural demand.

Coal inventories at China’s centrally dispatched power plants remain around 210 million tonnes, equivalent to approximately 34 days of consumption, reducing the urgency for spot purchases despite expectations of stronger summer electricity demand.

Tender activity also points towards increasing competition among exporters.

Australian 5,500 NAR coal traded around $117/t CFR South China, while comparable Russian cargoes were concluded near $115/t CFR.

Meanwhile, Indonesian low-CV cargoes continue to dominate tender activity, with 3,800 NAR offers clustered between RMB 597-618/t DDP South China, down from RMB 633/t recorded earlier this month.

Indian buyers remain largely absent

Indian utilities and industrial consumers continued to adopt a wait-and-watch approach.

Despite the recent correction in Australian prices, import demand remained limited as domestic coal availability stays comfortable and the southwest monsoon reduces immediate consumption requirements.

Sponge iron producers have also remained cautious amid weak finished steel prices, limiting demand for imported South African material.

Consequently, India has contributed little incremental buying support to the regional market during the week, leaving China as the primary driver of price discovery.

Freight markets reinforce softer tone

Freight indicators also point towards a cooling market.

Chinese coastal freight rates declined during the week, reflecting slower spot procurement and reduced cargo movements.

Similarly, Panamax freight from Kalimantan and Richards Bay into India remained stable to slightly weaker, preventing freight costs from providing any meaningful support to delivered coal prices.

Outlook: Correction or consolidation?

The correction in Australian high-CV coal appears to have removed much of the speculative premium that built up during late May and early June.

However, the broader Asian market does not yet exhibit characteristics of a sustained bearish cycle.

Three factors should continue to provide support:

- Indonesian production uncertainty, particularly surrounding RKAB revisions and DMO obligations

- Chinese mine supply constraints arising from safety inspections; and

- Potential summer power demand growth across North Asia as temperatures rise

Against these supportive factors stand equally important bearish influences:

- exceptionally high Chinese utility inventories,

- subdued Indian import demand,

- weakening paper markets, and

- abundant prompt cargo availability.

As a result, the market appears to be moving from the sharp rally witnessed in early June into a period of consolidation, with Australian high-CV coal likely to remain under pressure while Indonesian low-CV prices continue to find support from supply-side discipline.

Overall, the divergence between Australian and Indonesian coal is emerging as the defining theme of the Asian thermal coal market heading into the second half of June.

Leave a Reply