*Exports rise attributed to drop in coking coal prices

*Export volumes to India fall 21% m-o-m in March

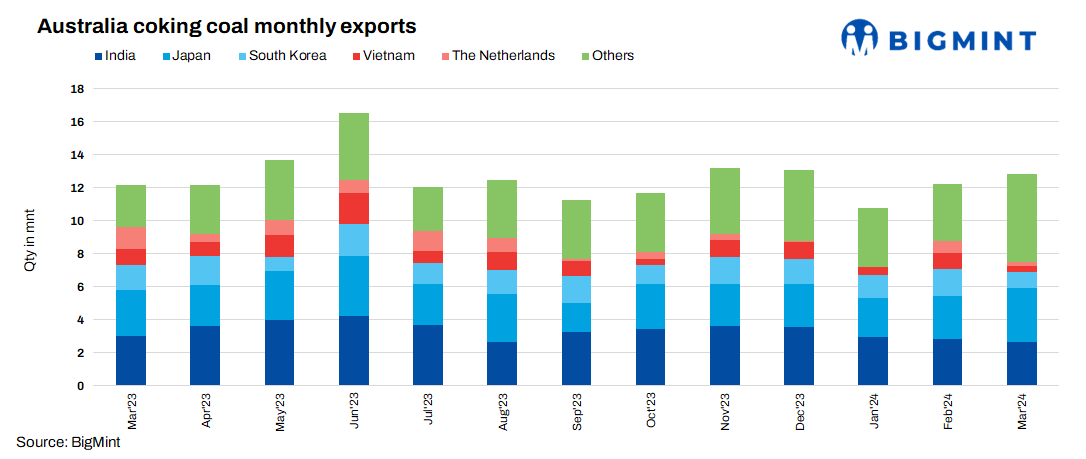

Australian coking coal exports increased by 5% m-o-m to 12.83 million tonnes (mnt) in March 2024 as against 12.24 mnt in February 2024.However, exports increased 5% to 12.83 mnt in March 2024 as against 12.17 mnt in March 2023. This increase in Australian coking coal exports can be attributed to the drop in coking coal prices.

Drop in coking coal prices

Australia remains the dominant supplier of coking coal, accounting for 60% of global shipments. Its PHCC FOB Australia prices dropped 11% in March 2024 to $280.36/t, down from $316.44/t in February. This decline occurred alongside an increase in import volumes due to a softening in seaborne prices.

India, the world’s second-largest producer of crude steel after China, continues to face a shortage of coking coal supplies, particularly in the domestic market. Indian mills primarily rely on imports, making the country the largest importer of coking coal. Exports to other countries, such as Japan and South Korea, have also increased. The softening in seaborne prices has benefited Australia by causing an increase in exports.

Exports to India stood at 2.58 mnt, in March 2024, down 21% m-o-m. Shipments to Japan increased by 8% m-o-m to 2.86 mnt in March 2024 as against 2.86 mnt in February.

Exports to South Korea surged by 75% at 1.64 mnt in March 2024. Imports by China (up by 80%) and Taiwan (up by 4%) were recorded at 1.33 mnt and 0.46 mnt, respectively. Shipments to Vietnam and The Netherlands increased significantly m-o-m to 1.00 mnt and 0.69 mnt.

Exports from Gladstone increased by 22% m-o-m to 4.07 mnt in March 2024 as against 3.34 mnt in February 2024. Shipments from DBCT stood at 3.65 mnt in March 2024 as against 3.95 mnt in February 2024. Supplies from Hay Point and Abbot Point rose by 8% and 3%, respectively, in the month under review.

Outlook

Coking coal exports might decline from India due to the upcoming elections, as India’s major steel demand stems from infrastructure and construction projects, which may see delays due to the elections. This could directly reduce demand from India, while subdued demand from China’s steel sector could also have an impact.

Additionally, with the drop in Australian coking coal prices, buyers are in a wait-and-watch mode, anticipating further price reductions.