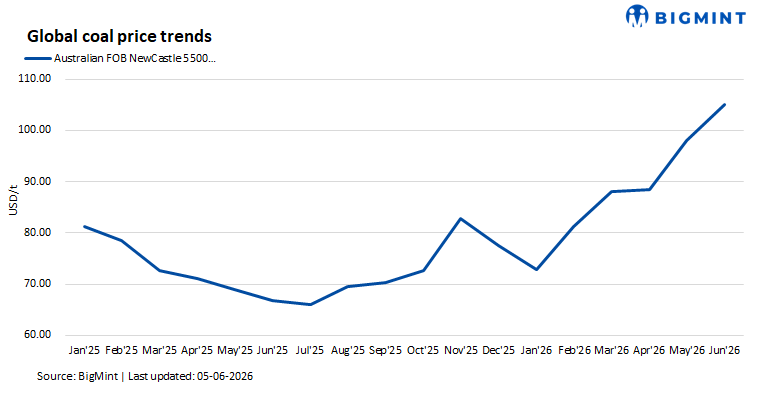

- Prompt tightness drives price surge

- Forward curve shifts to backwardation

The FOB Newcastle 6,000 kcal/kg thermal coal market has seen a sharp curve adjustment, with the forward structure flipping from contango into backwardation within a week. Spot physical prices surged by $7/t to $147/t, supported by four 25,000 t parcels traded for July-August loading at $148.50-150/t.

However, the rally was not matched by the paper market. The Q3 2026 contract slipped $0.50/t to $147.50/t, while Cal-27 fell $1/t to $145.50/t. This divergence suggests that prompt physical tightness is real, but the market is not yet pricing a sustained demand-led rally.

Physical catches up after paper-led strength

The sharp rise in physical NEWC appears to have been a catch-up move after paper had already rallied earlier. Once the physical-paper gap closed, momentum weakened during the European session.

This is important because a true demand-led rally would usually pull the full forward curve higher. Instead, the near-dated market strengthened while forward contracts softened, pointing to short-term tightness rather than a broader structural repricing.

Supply risks remain concentrated in Asia

The prompt tightness is linked partly to restricted alternative supply. Indonesian availability remains affected by the DSI export transition, pending RKAB quota approvals and firm seller offers. This has pushed some buyers towards Australian high-calorific value coal.

At the same time, demand signals are mixed. Chinese domestic Qinhuangdao prices rose RMB 5/t to RMB 865/t, but Chinese buyers remain selective. Indian buyers remain largely cautious due to adequate domestic stocks, high freight and the onset of monsoon-related demand moderation.

Outlook

The backwardation is justified by prompt supply tightness, but the speed of the $7/t move suggests the market may have moved too quickly. With Q3 and Cal-27 paper softening, NEWC 6,000 kcal/kg may consolidate in the near term.

A sustained move above $150/t would require fresh Chinese restocking, further Indonesian disruption, or stronger utility buying. Otherwise, the market could ease back towards the $142-145/t range.

Leave a Reply