- Queensland, NSW output drops; sales show modest recovery

- Strong coal demand persists; production guidance unchanged

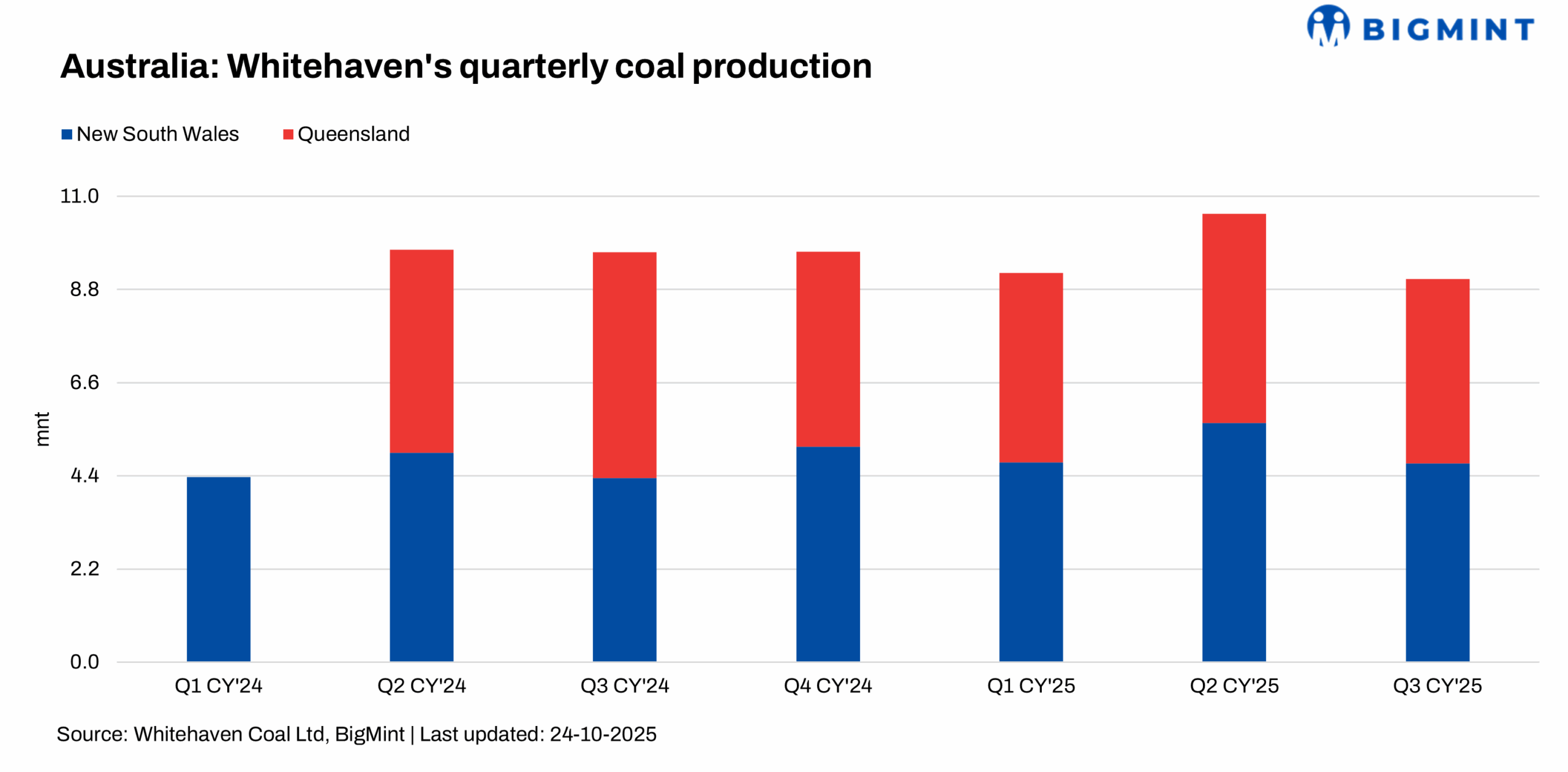

Whitehaven Coal recorded a slight slip in Q3CY’25 (July-September 2025), with managed run-of-mine (ROM) production at 9 million tonnes (mnt), reflecting a 15% decline q-o-q. Equity sales of produced coal stood at 5.9 mnt, down marginally by 1%.

The miner maintained operational discipline despite weather challenges and mine sequencing.

Queensland shows weak output after strong Apr-Jun quarter

In Queensland, managed ROM production reached 4.7 mnt, down 17% q-o-q, after an exceptionally strong April-June quarter. The decline was attributed to dragline sequencing and planned pre-strip works.

Blackwater produced 3.2 mnt, with volumes dropping sharply by 21%, as focus shifted towards overburden removal to support future production. However, sales volumes improved 5% to 3.0 mnt due to healthy starting inventories and better port throughput.

Daunia maintained stable ROM production of 1.5 mnt, though sales volumes eased 26% owing to shipment timing and strong sales in the prior quarter.

NSW coal output impacted by floods, sales show recovery

Operations in New South Wales (NSW) faced early-quarter flooding. Managed ROM output stood at 4.4 mnt, down by 12% q-o-q, with sequential improvement in sales volumes, up 6% q-o-q.

Maules Creek production fell 39% to 2.2 mnt due to mine sequencing and weather delays, though sales grew 5%. Narrabri delivered 1.2 mnt, rebounding after the longwall move, while sales were 0.7 mnt. The Gunnedah Open Cuts sustained steady output of 0.9 mnt q-o-q, selling 0.6 mnt of coal.

Market dynamics, financials

In Q3CY’25, the PLV HCC Index stayed weak due to soft global demand and uncertainties around US trade. Indian coal imports were hit by cheaper Chinese steel, while China’s production cuts and Northern Hemisphere demand supported gC NEWC prices. Whitehaven saw strong coal demand and focused on margins, costs, and smart capital use.

Development, exploration

Whitehaven spent A$10.1M on development (Winchester South, Narrabri Stage 3, Vickery) and A$4.3M on exploration in NSW and QLD during the September quarter, with expenditures managed amid low coal prices.

- Narrabri Stage 3 extends mine life to 2044, using existing infrastructure; operations began 1 August 2025, with a second mining lease application lodged for the western area.

- Winchester South received Queensland environmental approval; EPBC approval is ongoing, with Land Court hearings on objections continuing, while feasibility studies progress, including synergies with Daunia.

Outlook

Whitehaven closed the quarter with net debt of around A$0.8 billion as of 30 September 2025, maintaining financial resilience. The company reaffirmed its FY’26 (July 2025-June 2026) production guidance at 37-41 mnt of managed ROM. Looking ahead, Whitehaven expects long-term market support from structural supply shortfalls in metallurgical coal and sustained demand for high-CV thermal coal.

Leave a Reply