- Weather disruptions impact production, sales

- Queensland output falls 3%, NSW down 7% q-o-q

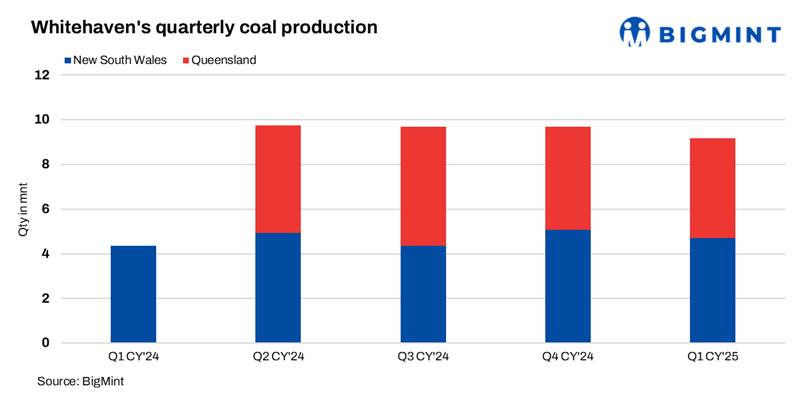

Whitehaven Coal posted a 5% q-o-q decline in managed run of mine (ROM) production to 9.2 million tonnes (mnt) in Q1CY’25 (January-March 2025). Production fell, as operations at various sites were impacted by adverse weather conditions.

Despite operational headwinds, the company maintained its full-year production guidance of 35-40 mnt for FY’25 (July 2024-June 2025), reaffirming its focus on operational resilience and disciplined capital allocation amid volatile market conditions.

Queensland operations hit by weather disruptions

Whitehaven’s Queensland operations delivered 4.5 mnt of ROM coal, a 3% decline from the previous quarter, with weather disruptions notably impacting coal shipments. Sales volumes fell 26% q-o-q to 3.4 mnt, as logistical bottlenecks, particularly in February, disrupted rail and port access.

At Daunia, ROM production dropped 18% q-o-q to 1.2 mnt due to significant rainfall. However, proactive site planning and water management allowed operations to continue. Still, sales volumes declined sharply by 43% q-o-q, impacted by rail and port delays.

Blackwater, in contrast, recorded a 4% q-o-q increase in ROM output to 3.2 mnt. Yet, similar weather-related logistics issues led to an 18% q-o-q fall in sales volumes.

Production from New South Wales falls amid seasonal factors

New South Wales operations saw a 7% q-o-q reduction in ROM production to 4.7 mnt. While NSW open-cut mines achieved a 2% q-o-q lift in output despite wet conditions late in the quarter, total sales of produced coal declined by 12% to 3.6 mnt.

Maules Creek reported a modest 4% q-o-q fall in ROM output to 2.8 mnt. However, improved coal processing and efficient railings led to a 22% q-o-q increase in sales volumes, to 2.3 mnt.

Narrabri’s output dropped sharply by 31% to 0.95 mnt, as the longwall approached the end of panel 203, reducing productivity. Sales fell even further, down 61%, to 0.7 mnt due to constrained output and continued transport challenges.

In contrast, the Gunnedah Open Cuts delivered strong performance, with ROM production up 20% to 1 mnt and sales rising 52% to 0.6 mnt, reflecting improved operational efficiency.

Tarrawonga’s production remained stable at 0.5 mnt. Meanwhile, early-stage mining at Vickery progressed well, with ROM production increasing 25% to 0.5 mnt, as box cut development continued.

Project development continues despite regulatory hurdles

Whitehaven is advancing key development projects aimed at securing long-term growth.

- The Narrabri Stage 3 Project – approved by the Federal Government in December 2024, subject to conditions – extends the mine’s life from 2031 to 2044. The project will tap into adjacent resources using existing infrastructure and longwall mining methods.

- The Winchester South project continues to progress through environmental approvals. Objections to the project are set for review in the Queensland Land Court in July 2025. Feasibility studies remain underway, including potential operational synergies with the Daunia mine.

Coal prices fall despite strong demand

In the March quarter, coal demand remained strong, especially from Japan, but prices weakened due to oversupply, lower steel production, and trade uncertainty. Indian demand lagged amid cheap Chinese steel exports. Amid these market pressures, Whitehaven is focusing on cost control, margin optimisation, and disciplined capital use.

Leave a Reply