- Australia’s exports fell on weak Asian restocking and demand

- Northern ports gained while major Asian buyers cut intake

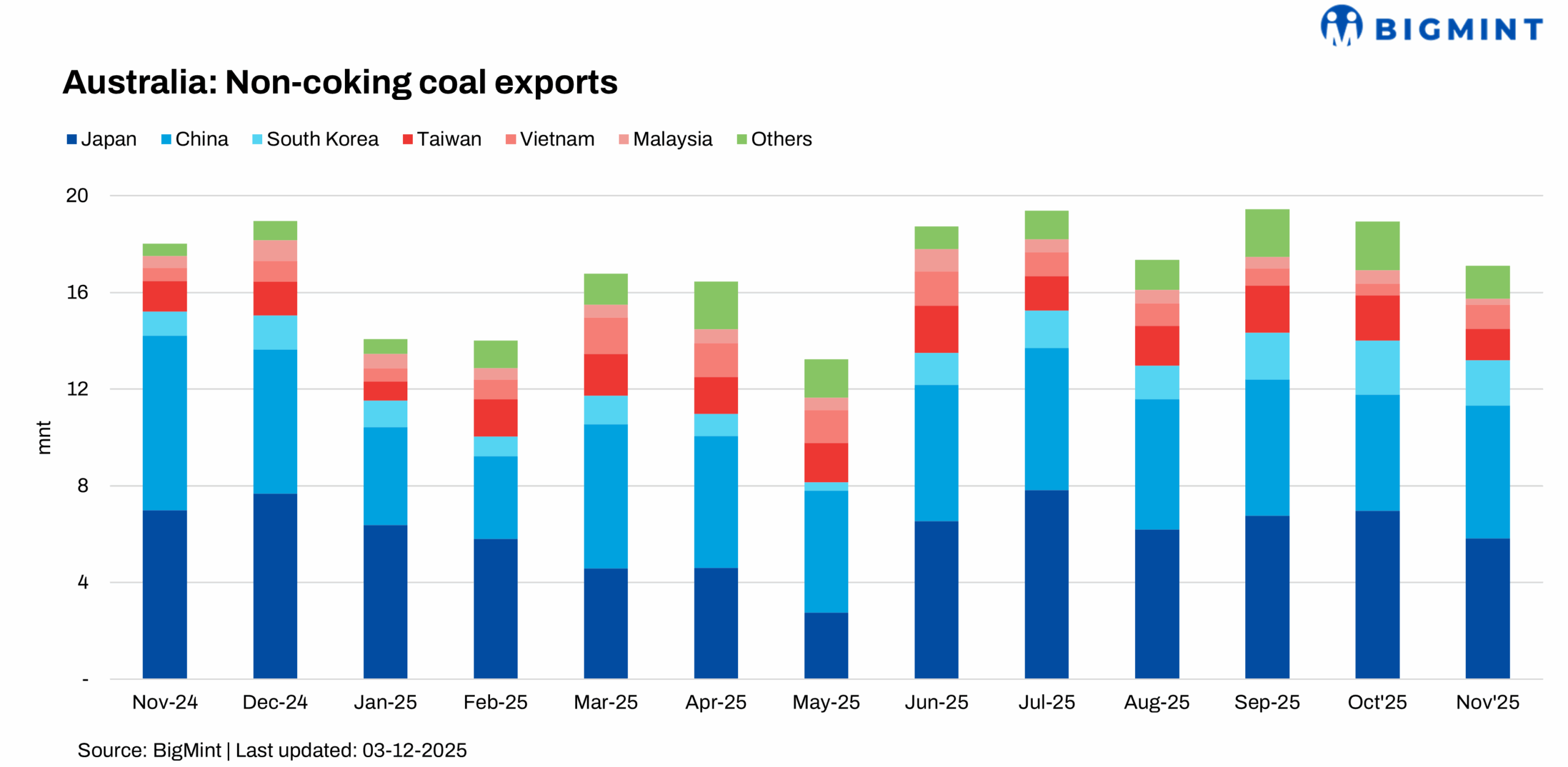

Australia’s non coking coal exports fell sharply by 9.6% month-on-month (m-o-m) to 17.11 million tonnes (mnt) in November, from 18.94 mnt in October. On a yearly basis, shipments were down 5.1% compared to 18.03 mnt in November 2024, reflecting subdued buying momentum across key Asian markets.

Asian demand softens as restocking slows

Weaker restocking activity across major Asian buyers — particularly Japan, South Korea, Taiwan, and Malaysia — dampened Australia’s export volumes. Overall Asian demand remained mixed, shaped by divergent power sector conditions across the region.

China stood out as the most resilient buyer. The country’s imports rose 6.4% m-o-m to 5.51 mnt, supported by steady coastal power plant consumption. Vietnam’s intake surged by a sharp 78.1% to 1.01 mnt.

However, other markets saw notable declines. Malaysia’s imports plunged 66.1% to 0.24 mnt, signalling weak industrial generation. Taiwan’s intake fell 30.7% m-o-m to 1.3 mnt due to softer power demand. Japan — the top buyer of Australian non coking coal, reduced purchases by 17.1% m-o-m to 5.83 mnt as utility demand remained muted. South Korea’s imports also dropped 17.6% to 1.86 mnt, driven by slower restocking cycles.

Export terminals see divergent performance

Australia’s major coal ports reported mixed operational trends in November. Newcastle Port handled 12.21 mnt, a 12.6% m-o-m decline, reflecting weaker cargo movements. Gladstone Port saw shipments fall 19.4% to 1.69 mnt, while Brisbane Port registered a sharp 35.2% drop to 0.37 mnt.

In contrast, other terminals posted strong gains. Abbot Point recorded a 21.8% growth to 1.46 mnt amid higher vessel loadings. Dalrymple Bay Coal Terminal (DBCT) delivered a robust 36.5% increase to 1.19 mnt, supported by improved berth availability. Port Kembla, however, saw its volumes fall 13% to 0.2 mnt due to reduced vessel arrivals.

Outlook

Australia’s non coking coal exports are expected to remain broadly stable in the near term, supported by China’s steady buying and seasonal demand in Southeast Asia. However, sustained weakness in Japan and South Korea, coupled with fluctuating industrial activity in Taiwan and Malaysia, may cap any significant upside. Port performance is likely to remain uneven, with northern terminals better positioned to handle emerging demand pockets.

Leave a Reply