BHP Group Limited announced its calendar year 2022 (CY22) results recently. Iron ore production for CY22 from its Western Australia mines was recorded at 284.8 million tonnes (mnt) on 100% basis, remaining largely stable y-o-y as against 284.1 mnt in CY21. The above-mentioned figures relate to production from all its mines.

The marginal increase in output was due to a strong supply chain, lower labour constraints and lower Covid-19-related impacts than the previous period, which were partially offset by wet weather impacts.

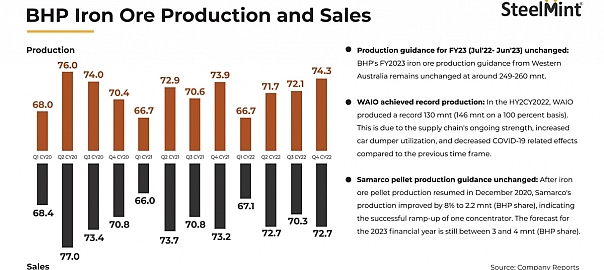

BHP’s output inched up by 3% to 74.3 mnt q-o-q in Q4CY22 compared to 72.1 mnt in Q3CY22. BHP’s production remained stable against Q4CY21 with 73.9 mnt iron ore.

Iron ore sales stable in CY22

The company’s total iron ore sales from Pilbara on 100% basis were recorded at 282.9 mnt in CY22, which remained stable y-o-y as compared to 283.7 mnt in CY21.

Sales increased by 3% to 72.7 mnt in Q4CY22 q-o-q as against 70.3 mnt in Q3CY22. BHP’s sales remained stable against Q4CY21 with 73.2 mnt.

Other highlights

- Production guidance for FY23 (July 2022- June 2023) unchanged: BHP’s FY23 iron ore production guidance from Western Australia remains unchanged at around 249-260 mnt.

- WAIO achieved record production: In the second half (H2) of H2CY22, WAIO produced a record 130 mnt (146 mnt on a 100% basis). This is due to the supply chain’s ongoing strength, increased car dumper utilisation, and decreased Covid-19-related effects compared to the previous time frame.

However, WAIO’s production guidance for FY23 remains unchanged at 246-256 mnt (278-290 mnt on a 100% basis). - South Flank to reach full capacity in 3 years: The South Flank ramp-up to the full production capacity of 80 mntpa (on a 100% basis) is proceeding as planned. Natural fluctuation in ore grade is to be expected as the mine moves through the near-surface material, but this is expected to stabilise.

- Samarco’s pellet production guidance unchanged: After iron ore pellet production resumed in December 2020, Samarco’s production improved by 8% to 2.2 mnt (BHP share), indicating the successful ramp-up of one concentrator. The forecast for the FY23 is still between 3 and 4 mnt (BHP share).

Leave a Reply