- Low and mid-CV coal: bullish bias on Indonesian supply risk

- High-CV coal: range-bound due to Atlantic oversupply

Market Developments

Asian thermal coal markets firmed at the low- and mid-calorific value (CV) end, even as high-CV benchmarks remained range-bound. Spot physical prices in Indonesia and Australia edged higher, while financial contracts recovered mid-week following earlier losses.

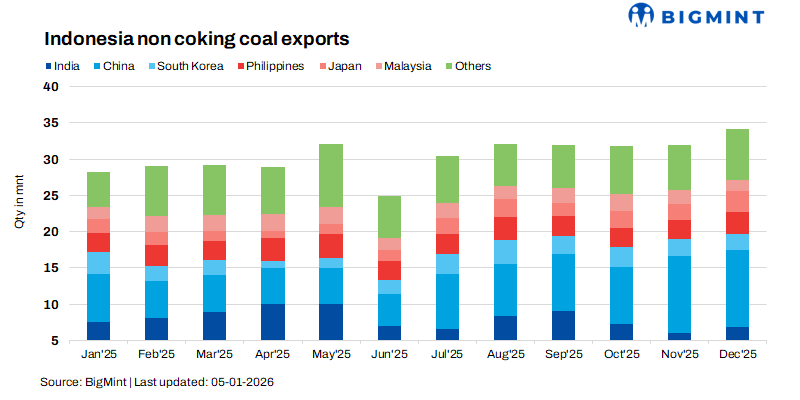

Indonesia’s thermal coal exports declined sharply in 2025, falling 7.8% year-on-year to 364.6 million tonnes. Shipments to China dropped to 77.7 million tonnes (-9%), while exports to India fell to 99.7 million tonnes (-7%). Despite stronger-than-expected exports in December, forward expectations deteriorated, with Q1 2026 exports forecast at 108 million tonnes, down 15 million tonnes year-on-year.

Low-CV Indonesian 4,200 GAR coal rose to $48/t, while Newcastle 5,500 kcal/kg coal increased to $76/t. In contrast, Newcastle 6,000 kcal/kg prices were flat at $113/t, capped by weakness in the Atlantic basin.

Key drivers

Market sentiment is shifting from short-term volatility to structural supply risk in Indonesia. While government discussions around a potential 2026 production cap near 600 million tonnes remain unresolved, uncertainty surrounding the RKAB approval process has already altered buyer behaviour.

Producers are resisting sharp output cuts, warning of operational shutdowns, contract breaches, and long-term investment damage. Importers, meanwhile, are increasingly uncomfortable delaying procurement into the second half of 2026, given declining Indonesian export availability and limited alternative low-CV supply.

This has encouraged early, defensive buying, particularly among Asian utilities exposed to Indonesian coal.

Price direction and market implications

High-CV coal prices remain supported by Pacific demand but constrained by Atlantic oversupply and soft European fundamentals. By contrast, mid- and low-CV prices retain a firmer bias, especially if Indonesian export flows undershoot expectations in early 2026.

Any formal confirmation of production caps – even if phased or revised mid-year – could accelerate pre-buying and tighten physical availability.

Big picture takeaway

Asian coal markets are tightening gradually rather than dramatically, with Indonesian supply uncertainty beginning to reshape procurement strategies, particularly for low- and mid-CV coal.

Leave a Reply