- Naphtha-dependent producers face production cuts and higher costs

- China’s diversified feedstock model shields chemical sector from supply shock

- Regional players accelerate consolidation and supply-chain cooperation

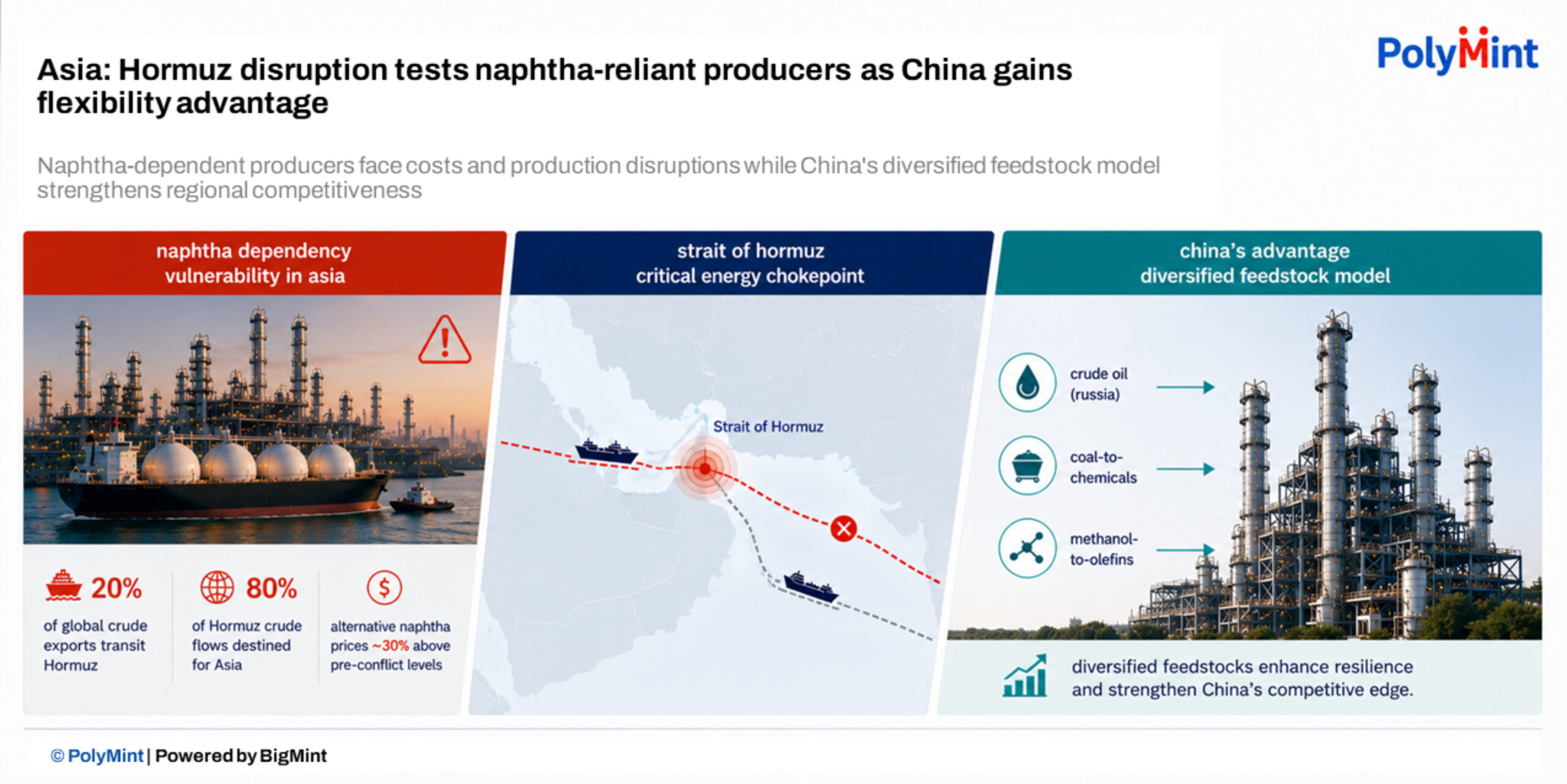

The disruption of Middle Eastern energy flows following the Iran conflict is exposing a structural weakness at the heart of Asia’s petrochemical industry. While Japan, South Korea and several Southeast Asian producers are grappling with higher feedstock costs and operational disruptions, China has emerged relatively insulated, highlighting how divergent feedstock strategies are increasingly shaping competitiveness in the global chemicals market.

The de facto closure of the Strait of Hormuz, through which around 20% of global crude oil exports transit, has hit Asia disproportionately. More than 80% of the crude passing through the strategic waterway is destined for Asian markets, making the region particularly vulnerable to supply disruptions.

The impact has been immediate for naphtha-dependent producers. Japan has reduced operating rates at ethylene facilities, while some petrochemical plants in South Korea and Vietnam have reportedly shut down. Producers across the region have been forced to source alternative naphtha cargoes outside the Middle East, pushing feedstock costs sharply higher.

At one stage, non-Middle Eastern naphtha prices doubled from pre-conflict levels. Although prices have since moderated, they remain around 30% higher, eroding cracker margins at a time when the sector was already struggling with weak profitability and persistent oversupply.

“The recent blockade of the Strait of Hormuz has emerged as a major crisis that exposes the Asian petrochemical industry’s structural vulnerabilities,” said Baek Jong-hoon, acting chairman of the Korea Chemical Industry Association and chief executive officer of Kumho Petrochemical.

China’s advantage goes beyond crude sourcing

The current crisis has reinforced the benefits of China’s decade-long effort to diversify both crude sources and petrochemical feedstocks.

Unlike Japan and South Korea, where naphtha remains the dominant feedstock for ethylene production, Chinese producers operate a broader feedstock mix that includes coal-to-chemicals, coal-derived methanol, ethane-based production, and naphtha. In addition, China’s crude imports are less concentrated in the Middle East and include significant volumes from Russia.

As a result, Chinese producers can continue supplying chemicals even if Middle Eastern naphtha availability remains constrained. The situation is particularly significant because Chinese chemical manufacturers already enjoy a cost advantage in export markets.

Industry participants warn that prolonged disruption could further strengthen China’s position in regional chemical trade.

“The competitiveness of Asia’s petrochemical industry, including Japan, will further decline,” a senior executive at a major Japanese chemical company said.

Existing industry pressures intensify

The Hormuz disruption arrives at a time when Asian petrochemical producers are already facing intense pressure from low-cost Chinese exports.

For several years, Japanese, Korean, and Southeast Asian producers have struggled with a glut of competitively priced Chinese chemicals that compressed margins and weakened profitability across commodity petrochemical chains.

According to market participants, the current feedstock disruption represents a second major challenge for an industry already under stress.

South Korea has responded by promoting consolidation of ethylene assets under government leadership to improve efficiency and address overcapacity. In Thailand, state-owned PTT and Siam Cement Group (SCG) announced plans to explore the merger of their commodity chemicals and basic plastics businesses.

The objective is clear: improve utilisation rates, reduce costs and shift toward specialty and higher-value products where margins are less vulnerable to commodity cycles and Chinese competition.

“Today, that transition is moving faster and with greater urgency,” said Toasaporn Boonyapipat, chairman of a Thai petrochemical industry association.

Supply security moves to the forefront

Beyond pricing and profitability, the crisis is reshaping how Asian governments and companies view resource security.

In response to the disruption, Japan has proposed the POWERR Asia initiative, aimed at strengthening cooperation on resource procurement and supply-chain resilience across the region.

Industry leaders increasingly believe that collaboration will be essential as geopolitical risks, overcapacity concerns, and decarbonisation pressures converge.

“In an era defined by geopolitical uncertainty, overcapacity, and the urgent call for climate action, collaboration is no longer a choice; it is essential,” said Tsao Mihn, chairman of a Taiwanese industry association and chairman of Formosa Petrochemical.

Japanese chemical companies have already spent years restructuring capacity to match declining domestic demand. However, industry executives argue that resilience requires more than rationalisation.

“With unexpected changes possible, it is also necessary to have a buffer and respond flexibly,” said Koshiro Kudo, chairman of the Japan Petrochemical Industry Association and president of Asahi Kasei. He added that greater cooperation with geographically close partners such as South Korea could provide meaningful risk diversification.

Outlook

The Hormuz disruption is not merely a short-term feedstock crisis. It is exposing a growing structural divide within Asia’s petrochemical industry.

While Japan, South Korea, and Southeast Asia remain heavily exposed to imported naphtha and Middle Eastern supply chains, China has built a more flexible production model based on diversified crude sourcing and alternative feedstocks. The current crisis is therefore accelerating a trend already underway: a widening competitiveness gap between China’s chemical industry and the rest of Asia.

Unless regional producers successfully consolidate assets, diversify feedstocks and strengthen supply-chain cooperation, prolonged disruptions could allow Chinese chemical exports to capture an even larger share of Asian and global markets.

Leave a Reply