- Moranbah North’s output falls 63% post Mar’25 underground explosion

- Hard coking coal realisation rate declines to 85% from 93% last year

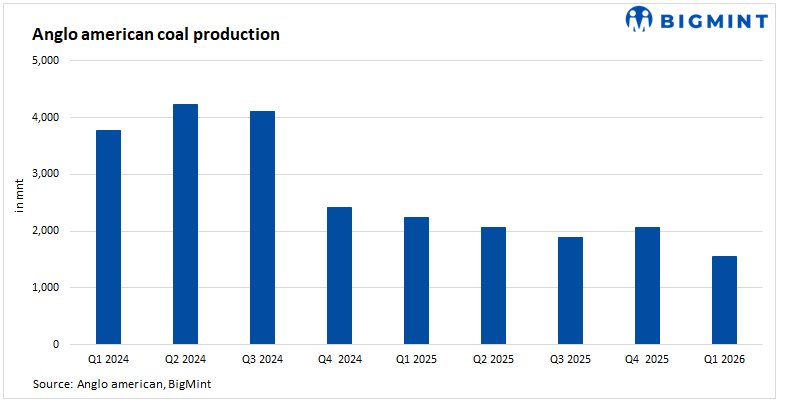

Anglo American reported a sharp 31% y-o-y decline in its steelmaking coal production in Q1CY’26 to 1.55 million tonnes (mnt) from 2.24 mnt in Q1CY’25 amid operational disruptions. Sales volumes also fell 10% y-o-y and 34% q-o-q to 1.47 mnt, reflecting both lower output and shipment constraints.

Segment-wise, hard coking coal production declined 30% to 1.22 mnt, while PCI/semi-soft coal output dropped 33% to 0.32 mnt. Thermal coal was the only positive, rising 25% y-o-y to 0.30 mnt, partially offsetting the overall decline.

Mine-level performance and pricing pressure

At the mine level, Moranbah North was the worst affected, with output plunging 63% y-o-y in Q1CY’26 to 0.20 mnt, followed by Dawson, which fell 55% to 0.28 mnt. In contrast, Aquila (Capcoal) remained relatively stable, registering only a 1% y-o-y dip to 1.07 mnt.

Despite a stable product mix of 79% hard coking coal and 21% PCI/semi-soft coal, price realisations weakened. Hard coking coal realised $199/t versus a $235/t benchmark, translating to an 85% realisation rate, down from 93% last year.

Operational and weather-related disruptions

The primary driver was the continued impact of the March 2025 incident at Moranbah North, which significantly disrupted production. Notably, a small contained ignition incident had occurred in the goaf at the Moranbah North mine on 31 March 2025. Although regulatory approvals were lifted in February 2026, the mine operated under a phased restart, limiting output during the quarter.

Adverse weather conditions further affected production at the Dawson open-cut operations, adding to the overall decline. These disruptions led to lower availability and weaker sales volumes across segments.

Product mix and limited recovery support

Additionally, a reduced share of premium hard coking coal from Moranbah North impacted the overall product quality mix, resulting in lower price realisations.

While Grosvenor showed operational progress with limited infrastructure damage and ongoing rectification work, it did not contribute to production, restricting near-term recovery.

Recovery outlook and strategic shift

The company is now moving into a gradual recovery phase, supported by the ramp-up of Moranbah North following its restart. Production is expected to improve sequentially as operations stabilise and output levels normalise.

Grosvenor is expected to resume longwall production by late 2027, which could provide a stronger production boost over the longer term, subject to final approvals. In the near term, however, performance may remain under pressure due to the gradual pace of recovery and operational normalisation across key assets.

Strategically, Anglo American’s plan to divest its steelmaking coal business — likely to conclude in Q2CY’26 — marks a significant shift. This indicates that the current recovery phase is also part of a broader transition, as the company reshapes its portfolio and reduces exposure to steelmaking coal.

Leave a Reply