- Century Aluminium to curtail output from Iceland smelter

- Beijing cuts 2025-26 base metal output target to 1.5% from 5%

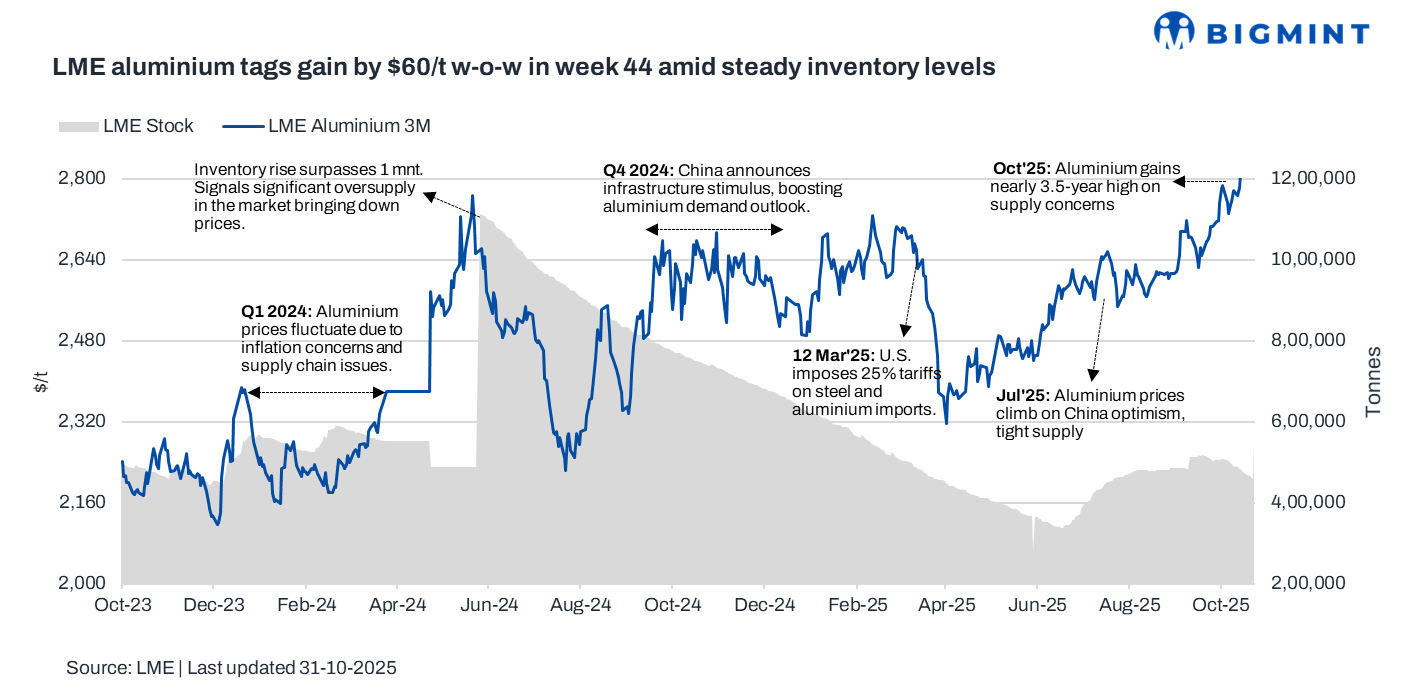

LME aluminium prices edged higher during week 44 of CY’25 (27-31 October), extending their upward momentum amid persistent supply concerns. Gains were supported by production disruptions, slower capacity growth in China, and resilient global demand indicators.

Pricing, inventory trends

LME aluminium prices averaged $2,872/tonne (t) in week 44, marking a $61/t or 2% rise w-o-w from week 43 (20-24 October). The week began with prices at $2,877/t, which inched up to around $2,892/t mid-week and closed at $2,882/t.

Supporting the price, LME aluminium inventories maintained stability for the week at 483,050 t from 480,915 t in week 43.

What drove the gains?

Aluminium prices increased, supported by tightening global supply conditions following Century Aluminium’s decision to curtail two-thirds of production at its Iceland smelter due to an electrical equipment failure.

The disruption added to mounting concerns that China could breach its 45 mnt aluminium output cap this year, heightening fears of near-term shortages. Further supporting sentiment, Beijing announced a slowdown in industrial capacity growth — cutting its annual base-metal output target for 2025-26 to 1.5% from 5% previously — reinforcing expectations of a tighter supply outlook.

In physical markets, aluminium stocks at Japan’s three major ports rose modestly by 1.8% to 341,300 t. China’s aluminium trade data were mixed: exports of unwrought aluminium and products fell to 521,000 t in September from 534,000 t in August, while imports surged 35.4% y-o-y to 360,000 t. Over the first nine months of 2025, total imports reached 3.01 mnt, up 5.7% from a year earlier, reflecting resilient domestic demand.

Adding to the bullish tone, Alcoa’s plan to close its Kwinana alumina refinery in Australia and growing aluminium usage in data centre construction have strengthened prospects of a long-term price uptrend.

Outlook

Aluminium prices are likely to remain supported in the near term amid tightening global supply and resilient demand. Production curtailments, China’s output cap, and steady import growth point to a firm market tone. However, macroeconomic uncertainties and demand risks from slower industrial activity could temper further upside momentum.

Leave a Reply