- Global sell-off hits aluminium, copper, and gold

- Warehouse stocks continue downward trend

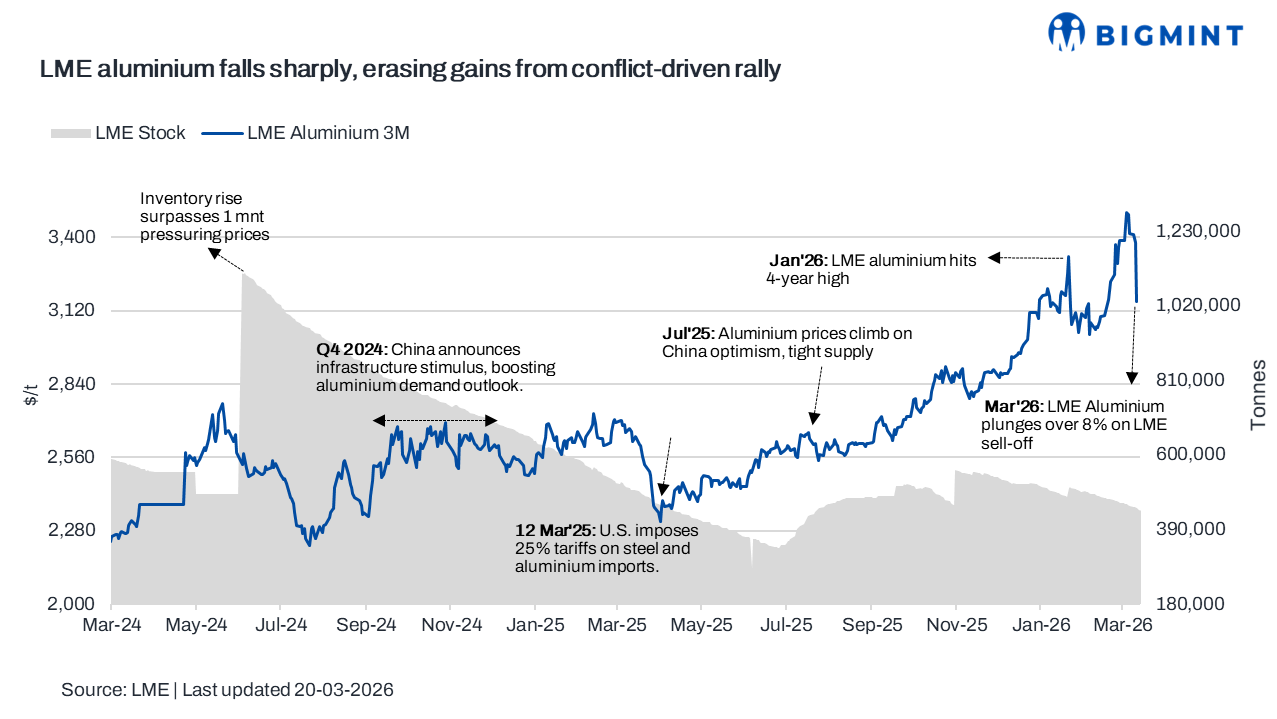

Aluminium prices on the London Metal Exchange (LME) tumbled more than 8% on 19 March 2026, marking the steepest single-day decline since 2018, as escalating concerns over the economic impact of the Iran conflict triggered a broad-based sell-off across global financial and commodity markets. Prices fell as much as 8.4% to around $3,115/t, wiping out gains accumulated since the onset of geopolitical tensions in the Middle East, which had earlier supported prices on fears of supply disruptions.

The sharp correction came amid widespread risk aversion, with industrial metals and broader asset classes facing heavy selling pressure. Copper prices declined by over 4%, while gold dropped more than 5-6%, and global equity markets also registered significant losses. The synchronized fall across asset classes reflects a shift in market focus from supply-side concerns to fears of weakening global economic growth and industrial demand.

Initially, aluminium prices had surged to multi-year highs as the Iran conflict raised concerns over disruptions to key supply chains, including smelter operations and critical shipping routes such as the Strait of Hormuz. However, sentiment reversed sharply as investors began pricing in the potential negative impact of prolonged geopolitical tensions on global trade, manufacturing activity, and overall economic stability.

Market participants also pointed to profit booking and liquidation of long positions following the recent rally, which further accelerated the downward momentum. The sell-off was amplified by broader macroeconomic pressures, including tighter financial conditions and uncertainty over monetary policy direction, which have weighed on base metals.

Despite the recent decline, underlying market fundamentals remain relatively tight. LME inventories have been trending lower, and physical premiums–particularly in Asia–remain elevated due to supply constraints, logistical challenges, and steady demand from sectors such as renewable energy and electric vehicles. However, in the near term, macroeconomic sentiment and geopolitical developments are expected to dominate price movements.

Going forward, aluminium markets are likely to remain highly volatile, with prices sensitive to developments in the Middle East conflict, global economic indicators, and investor risk appetite. While supply-side risks continue to provide underlying support, concerns over demand and financial market stability are expected to dictate short-term trends.

Outlook

Aluminium prices are expected to remain volatile, with downside risks linked to global economic uncertainty and continued geopolitical tensions. While tight inventories and supply-side constraints may offer some support, market direction will largely depend on demand outlook, macroeconomic trends, and developments in the Middle East.

Leave a Reply