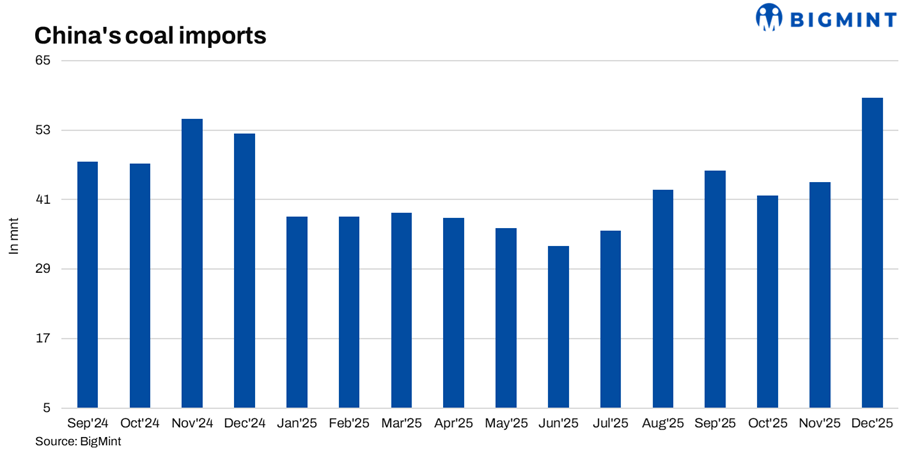

- Stronger domestic coal prices, RMB make imports more competitive

- Coal consumption falls 17% y-o-y, power plant inventories remain high

China’s thermal coal story right now has two sides. On paper, imports look more attractive. But on the ground, power demand remains weak. That tension is shaping how the market behaves, leading to selective import purchases despite favourable arbitrage.

Import economics improve

Import arbitrage into China has strengthened over the past week, driven by two factors: the firming of domestic coal prices and the strengthening of the renminbi to around 6.84 against the US dollar. A stronger domestic price and currency make imported coal more competitive.

Russian coal is the biggest beneficiary. The importing arbitrage for Russian mid-calorific value (CV) coal widened sharply, rising from roughly $13/tonne (t) to more than $20/t. That is a significant improvement in margin for Chinese buyers.

In addition, some Russian high-calorific coal is being sold into the mid-calorific segment. Buyers pay mid-CV prices but receive higher energy content. That improves value per tonne and makes Russian supply especially attractive.

Indonesian coal has also regained some competitiveness after lagging previous rallies. Australian coal remains at a premium. South African and Colombian coals are still largely uncompetitive into China at current price levels.

On pure economics, imports make sense again — particularly from Russia.

But demand remains muted

However, improved arbitrage does not automatically mean stronger buying.

Coal consumption at China’s top six thermal power plants recovered w-o-w after the Spring Festival holidays, but it remains 17% lower y-o-y for the second week in a row.

That is important.

Consumption is also below the seasonal average. In other words, even after the holiday slowdown ended, power demand has not bounced back strongly.

Inventories tell a similar story: Stocks at the six major power plants stand at 13.7 million tonnes (mnt), slightly down w-o-w but still 3.7% higher y-o-y. Stocks are also above the average seasonal level since 2021.

At Qinhuangdao Port, inventories recovered w-o-w to 5.3 mnt, but they remain significantly lower than last year. Even so, there is no sign of shortage.

The key takeaway is simple: China is not short of coal.

What this means for the market

China is the world’s largest coal importer. When Chinese demand is strong, global prices rise quickly. When demand is soft, rallies struggle to sustain momentum.

At present, market signals remain mixed. On the positive side, import economics are supportive, with competitively priced Russian coal offering a clear pricing advantage, while favourable currency movements are improving purchasing viability for buyers. However, these supportive external factors are being offset by subdued domestic fundamentals. Power plant consumption remains weak on a y-o-y basis, inventory levels are comfortable, and industrial activity has yet to show a strong acceleration. As a result, the market continues to balance cost-side support against muted demand conditions.

This explains why China is buying selectively rather than aggressively. Buyers are taking advantage of favourable arbitrage where it exists, especially for Russian cargoes. But they are not chasing the market higher.

If domestic power demand improves in the coming weeks, imports could increase more meaningfully. That would add fuel to the global rally.

If demand stays soft, improved arbitrage alone will not be enough to push prices much higher.

For now, China is acting as a stabiliser rather than a driver. The economics encourage imports, but weak consumption keeps the market balanced.

Leave a Reply