- OMC raises high-grade iron ore fines base prices for 20 Jul auction

- PELLEX rises on improving buying interest, tighter pellet availability

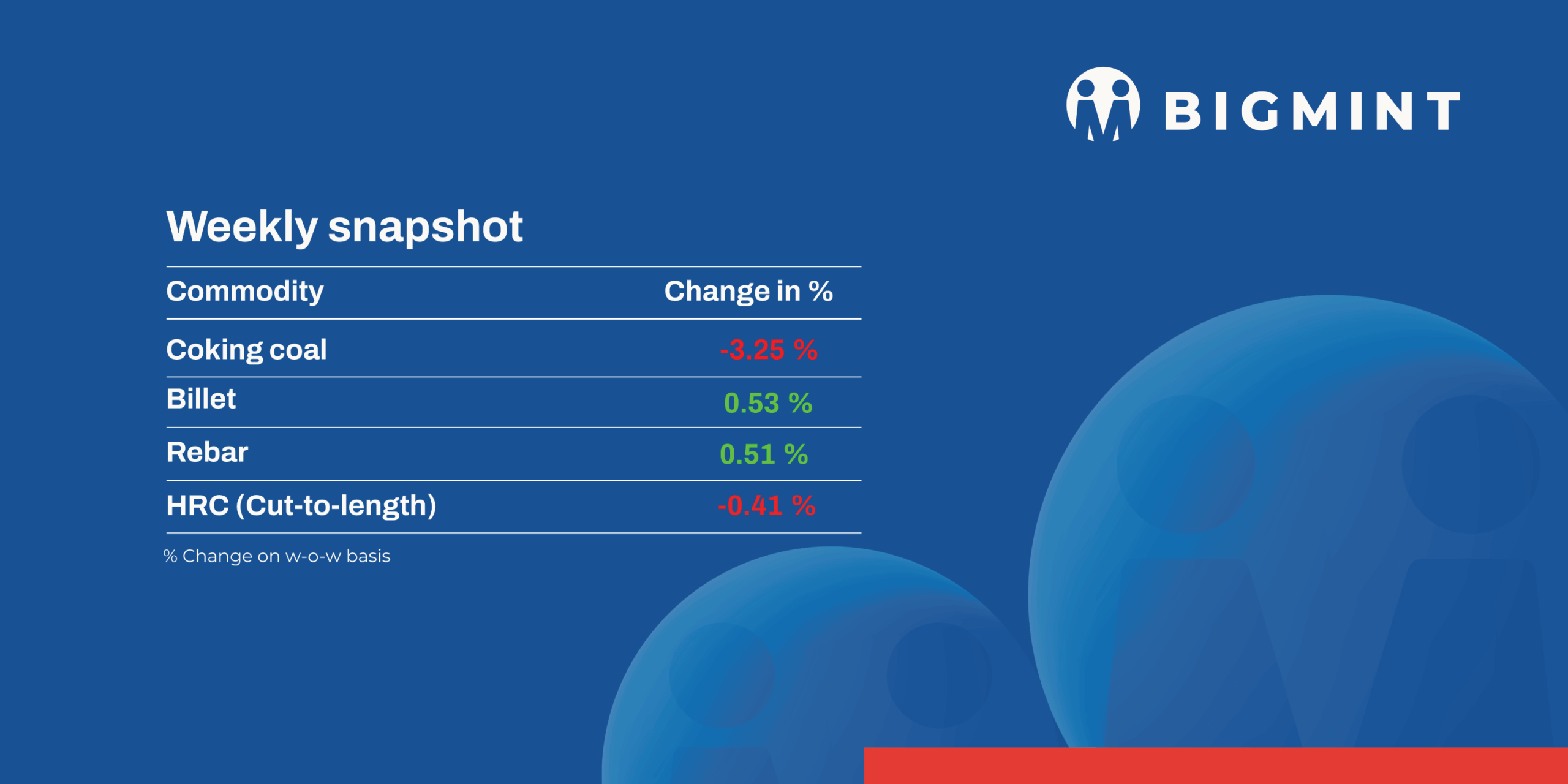

India’s steel and raw materials markets presented a mixed picture during the week ended 18 July, with strengthening raw material and semi-finished steel prices contrasting with continued weakness in finished steel prices, especially in the blast furnace (BF) segment.

Billet, sponge iron, and pellet prices rose on improving procurement and tighter availability, while BF rebar prices remained under pressure as aggressive mill price cuts failed to revive demand amid monsoon disruptions and cautious distributor buying.

Weak steel consumption also continued to weigh on coking coal, ferrous scrap, and ferro alloy markets, although firmer freights and selective export demand provided support to some raw materials.

Iron ore, pellet

- Odisha Mining Corporation (OMC) will auction 2.54 million tonnes (mnt) of iron ore on 20 July 2026, comprising 1.66 mnt of fines and 0.83 mnt of lumps. For the upcoming auction, the miner has kept floor prices of lump ore unchanged, while reducing floor prices for mid-grade fines by INR 50/tonne (t) m-o-m and raising base prices for higher-grade fines by INR 100/t. OMC has also reduced the offered volume by around 0.62 mnt from the previous month’s auction, following restrictions imposed by the Directorate of Mines and Geology (DMG), Odisha, on Fe 55-60% grade iron ore dispatches.

- BigMint’s India pellet (Fe 63%, 3-3.5% Al₂O₃) export index increased by $2/t w-o-w to $103/t FOB east coast on 15 July, supported by stronger export bookings. Despite seasonally weak steel demand in China, mills stepped up purchases of Indian pellets as lump ore premiums exceeded $20/dmtu, while export realisations remained broadly at par with domestic prices. More than 400,000 t of pellet export deals were reportedly concluded over the past two weeks at $116-118/t CFR China, supporting overall market sentiment.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, increased by INR 250/t to INR 9,550/t ($99/t) DAP, supported by improving buying interest and tighter material availability. Market participants reported that procurement activity has gradually picked up, with buyers returning to the market for need-based purchases after adopting a cautious stance over the past few weeks, resulting in firmer pellet prices in the Raipur market.

Coal

- The South African thermal coal market remained subdued during the week as weak sponge iron demand and comfortable inventories continued to limit buying interest despite firmer global offers. Lower port arrivals reduced inventories, but consumers continued requirement-based procurement, resulting in limited trading activity and a wide bid-offer gap. RB2 (5,500 NAR) remained stable at INR 10,450/t ex-Paradip, while RB3 (4,800 NAR) increased INR 50/t to INR 8,900/t. At Vizag, RB2 rose INR 50/t to INR 10,300/t, while RB3 declined INR 50/t to INR 8,800/t.

- Trading activity remained extremely limited, with around 5-6 deals totalling around 3,000-3,500 t concluded during the week, including Costa Rica-origin HMS 60:40 at $298/t CFR, HMS 80:20 at $333/t CFR, and Europe-origin turnings/borings at $300-305/t CFR Mundra.

- The met coke market remained cautious during the week as weak steel demand, comfortable inventories, and uncertainty over the continuation of the anti-dumping duty discouraged fresh buying and kept both domestic and imported trading activity limited. BF-grade met coke prices in eastern India declined INR 100/t to INR 35,150/t ex-Jajpur, while prices in western India remained stable at INR 34,000/t ex-Gandhidham. Foundry-grade coke remained unchanged at INR 36,400/t ex-Rajkot, while Indonesian-origin BF-grade metallurgical coke (65/63 CSR) eased $1/t to $318/t CFR India.

- BigMint’s premium hard coking coal (PHCC) index declined $4/t w-o-w to $250/t CNF Paradip on 17 July 2026, reflecting subdued coking coal market sentiment. A cargo of around 35,000 t of premium hard coking coal was reportedly booked at nearly $230/t FOB during the week. Prices remained under pressure amid cautious procurement by steelmakers and subdued downstream demand. Meanwhile, firmer Australia-India freights increased import costs, partially offsetting the weakness in coking coal prices and limiting the pace of further declines.

Ferrous scrap

- India’s imported ferrous scrap market remained subdued during the week ended 16 July as poor import viability, weak steel demand, and rising freight costs continued to discourage buying. Mills largely preferred domestic scrap and sponge iron over imported material, while renewed Middle East tensions tightened vessel availability and supported freight rates.

- Trading activity remained extremely limited, with only two containerised deals totaling around 600-1,000 t concluded during the week, including Costa Rica-origin HMS 60:40 at $298/t CFR Chennai and Europe-origin turnings/borings at $291/t CFR Mundra.

- EU/UK-origin HMS 80:20 was offered at $330-335/t CFR, Chile-origin HMS 80:20 at around $330/t CFR, West Africa-origin HMS at $340-345/t CFR, and Australia-origin HMS at $335-340/t CFR. UK-origin shredded scrap offers stood at $395-400/t CFR West Coast India against buyer indications of $365-370/t CFR, while containerised HMS was offered at $325-335/t CFR versus bids of $310-320/t CFR. Market participants expect import prices to remain under pressure in the coming weeks as limited procurement and weak steel demand continue to weigh on market sentiment.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices dropped by INR 850/t ($9/t) w-o-w to INR 74,100-74,700/t ($770-776/t) across key markets. Prices remained under pressure, extending their downtrend as weak procurement by domestic steel mills and sluggish finished steel demand weighed on sentiment. Comfortable alloy inventories, ample spot availability, and resistance to higher offers kept transaction activity subdued and limited producers’ pricing power.

Meanwhile, HC 65-16 silico manganese export prices edged down by $4/t to $914/t FOB Vizag/Haldia. - Ferro manganese: Indian ferro manganese (70%) prices remained largely steady with a slight w-o-w decline of INR 200/t ($2/t) to INR 78,300/t ($814/t) in Raipur and by INR 200/t ($4/t) to INR 78,200/t ($813/t) in Durgapur. Prices eased as buyers restricted purchases to immediate requirements and resisted higher offers, prompting suppliers to make minor price adjustments to conclude deals.

Meanwhile, export prices for the 75% grade also dipped by $6/t w-o-w to $920/t FOB Vizag/Haldia. - Ferro silicon: India ferro silicon (Si 70%) prices edged up by INR 500/t ($5/t) w-o-w to INR 88,500/t ($920/t) ex-works Guwahati, while Bhutan prices also rose by INR 400/t ($4/t) to INR 89,100/t ($926/t). Prices edged up slightly due to limited material availability, supported by healthy domestic demand and improved export enquiries, enabling producers to maintain firmer offers despite stable production levels.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices remained broadly stable, edging down by INR 300/t ($3/t) w-o-w to INR 122,500/t ($1,273/t) exw-Jajpur. India’s ferro chrome market remained under pressure as ample domestic availability continued to outpace subdued demand from stainless steel producers. Improved supply across key producing regions intensified competition among sellers, weighing on overall market sentiment.

- Additionally, Vedanta-FACOR’s ferro chrome auction on 15 July witnessed strong participation, with the larger lot (Cr: 58% min) closing at INR 121,400/t ($1,255/t) exw, up INR 600/t over the base price, while the smaller lot fetched INR 122,900/t ($1,277/t) exw, up INR 1,600/t. The entire offered volume was booked, reflecting healthy buying interest.

Semi finished

- India’s semi-finished steel market recovered during the week ended 18 July, supported by stronger buying activity, improved downstream demand, and increased procurement from neighbouring markets. As per BigMint’s assessment, domestic billet prices increased by INR 50-1,500/t ($0.5-15/t) w-o-w across major producing regions, as aggressive bookings and balanced availability of quality material helped lift spot prices.

- Market sentiment improved steadily through the week after an extended period of subdued trading. Good demand from re-rollers and neighbouring markets encouraged buyers to replenish inventories, while suppliers maintained disciplined sales amid relatively tighter availability of quality material. Improved bookings across multiple regions enabled producers to raise spot offers, supporting the overall recovery in the semi-finished steel market.

- Western and southern regions like Mumbai, Jalna, Chennai, and Gujarat in India witnessed price increases of INR 500-1,500/t ($5-15/t) w-o-w, supported by improved offtake from the finished steel segment and healthy procurement by re-rollers. The recovery in steel demand also contributed to stronger billet consumption, providing additional support to market sentiment.

- The sponge iron market displayed a mixed trend during the week. Prices across major producing regions increased by INR 100-500/t ($1-5/t) w-o-w, supported by a significant improvement in bookings and relatively limited spot availability. Producers were able to strengthen offers as buying activity improved across key sponge iron clusters. However, prices in Durgapur and Ramgarh were stable or edged down by INR 300/t ($3/t) w-o-w on regional variations in demand.

- Concerns over future supplies of quality raw material encouraged consumers to secure forward bookings, while higher pellet offers pushed up production costs for sponge iron manufacturers. The combination of improved demand and tighter raw material availability underpinned this week’s price recovery.

- In contrast, India’s direct reduced iron (DRI) export market remained under pressure due to limited buying interest from neighbouring countries. Exporters continued to lower their offers to improve competitiveness. Pellet-based sponge iron export offers to Nepal declined by $5/t w-o-w to $262/t CPT Raxaul, while CDRI/mix sponge iron offers also fell by $5/t to $290/t CPT Raxaul. Export offers to Bangladesh eased by $1/t to $300/t CPT Benapole.

Finished long steel

- IF-rebar: IF-route rebar prices witnessed a mixed trend across major regions during the week, with the sharpest increase of INR 900/t recorded in the Mumbai market, while most other markets remained largely stable or witnessed minor corrections.

- Overall, trading activity remained moderate throughout the week. A wide bid-offer gap encouraged active negotiations between buyers and sellers, with most deals concluded below the initial offer prices. However, the overall decline in prices remained limited as tight raw material availability and firm input costs restricted mills from offering steeper corrections.

- Mill inventories were maintained at around 10-15 days, while order booking visibility remained limited to approximately 3-5 days, indicating continued short-term procurement. IF-route rebar prices are expected to remain under pressure in the near term. While monsoon-led slowdown is likely to keep demand need-based, firm raw material prices and tight availability should prevent any sharp correction.

- W-o-w, rebar prices showed mixed trends in the range of INR 200-900/t across key regions, with the sharpest increase of INR 900/t seen in the Mumbai market, according to BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 39,500-39,900/t exw Raipur and INR 43,400-44,000/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 42,600–43,000/t exw Raipur.

- Trade reference prices of wire rod stood at INR 41,700-42,300/t exw Raipur.

- BF-rebar: BigMint’s benchmark BF-route rebar (IS 1786 Fe550D, 12-32 mm) prices declined by INR 100/t w-o-w to INR 47,900/t ex-Mumbai (distributor-to-dealer, excluding GST) on 17 July 2026. Month-to-date, Mumbai BF-route rebar prices have declined by around INR 2,100/t in July, reflecting persistent weak demand, cautious buying, and aggressive pricing by primary steelmakers to improve dispatches.

- The Indian BF-route rebar market is expected to remain under pressure in the near term as monsoon-led disruptions continue to affect construction activity and project execution. Despite multiple price reductions by primary mills, buying interest remains weak, with distributors continuing need-based procurement amid comfortable inventories and expectations of further price corrections. Although lower raw material costs have eased production expenses, a sustained recovery in demand is likely only after construction activity improves post-monsoon.

Flate steel

- BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) in Mumbai declined by INR 100/t w-o-w to INR 57,800/t ($606/t) as on 17 July from INR 57,900 ($610/t) in the previous assessment.

- Likewise, the benchmark assessment for CRC (IS513, Grade O, 0.9 mm/CTL) remained stable w-o-w INR 65,000/t ($680/t) as of 17 July.

- India’s trade-level HRC market dipped as buyers stayed on the sidelines. Sentiment remained weak on pricing and margin losses. Northern labour shortages disrupted operations, though OEM dealings continued; Southern prices dipped though work continued, while Western and Eastern markets held broadly stable.

- Import volumes: India’s bulk HRC imports stood at 91,381 t as of 10 July and are expected to reach 189,349 t by mid-August.

- Export volumes: India’s bulk HRC exports stood at 120,160 t as of 10 uly, with an additional 75,710 t expected to be added by end-July.

- Indian HRC exports are set for a mixed run ahead. EU demand is slowly recovering as clarity on quota rules improves, while Middle East shipments remain stuck over Hormuz concerns, and Vietnam continues to stay weak, weighed down by excess stock levels.

Leave a Reply