- Prices retreat after mid-week recovery; exchange stocks extend decline

- MCX eases from weekly high, while SHFE gains on improving sentiment

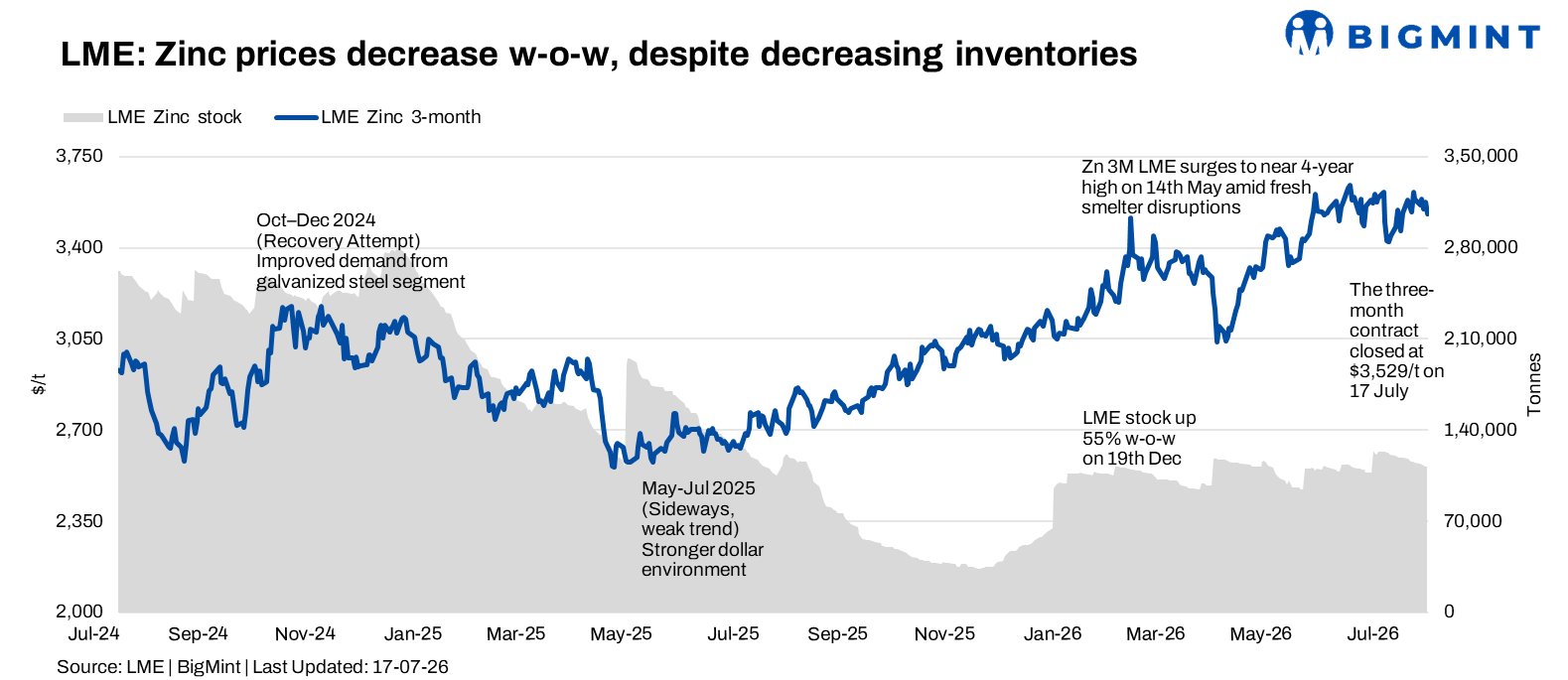

London Metal Exchange (LME) zinc prices declined during the week ended 17 July 2026, despite continued drawdowns in exchange inventories and periods of renewed buying interest. Prices remained volatile through the week, recovering sharply on 16 July before easing again on Friday as profit-booking and cautious market sentiment weighed on the market.

On a w-o-w basis, LME zinc cash settlement prices declined 1.5% to $3,549/t on 17 July from $3,602/t recorded on 10 July. Prices traded in a broad range during the week, with a sharp correction in the first half followed by a recovery before ending lower amid renewed selling pressure.

Price trends

LME zinc cash settlement prices opened the week at $3,571/t on 13 July, easing from the previous week’s close. Prices subsequently recovered to $3,589.5/t on 14 July before falling sharply to $3,553.5/t on 15 July amid renewed selling pressure across the base metals complex.

Buying interest strengthened on 16 July, lifting prices to $3,591/t. However, the recovery proved short-lived, with prices declining to a weekly low of $3,549/t on 17 July as profit-booking and cautious sentiment returned to the market.

The three-month contract broadly mirrored movements in the cash market. Prices stood at $3,565/t on 13 July before rising to $3,587/t on 14 July. The contract subsequently eased to $3,550/t on 15 July, recovered to $3,576.5/t on 16 July and then declined sharply to $3,529/t by the end of the week.

The narrowing of the three-month price against the cash market towards the end of the week reflected relatively firm nearby market conditions, even as forward prices remained under pressure.

Inventory analysis

LME zinc inventories continued to decline throughout the reporting week, extending the recent drawdown trend and providing underlying support to the market.

Stocks declined from 114,800 t on 10 July to 114,275 t on 13 July before falling further to 113,450 t on 14 July and 112,450 t on 15 July. The downtrend continued through the remainder of the week, with inventories easing to 111,875 t on 16 July and 111,725 t on 17 July.

Overall, exchange inventories declined by 3,075 t w-o-w. The continued drawdown in warehouse stocks remained a key supportive factor for zinc prices, although the persistent decline was not sufficient to prevent short-term price corrections amid profit-booking and broader market volatility.

MCX zinc trends (13-17 July)

On the Multi Commodity Exchange (MCX), zinc futures remained volatile during the reporting week, with prices initially easing before recovering sharply and subsequently correcting towards the end of the week.

The July contract settled at INR 374,150/t on 13 July before rising to INR 376,800/t on 14 July. Prices subsequently eased to INR 374,150/t on 15 July before rebounding sharply to INR 377,300/t on 16 July.

However, selling pressure emerged on the final trading day, with the contract closing at INR 373,150/t on 17 July. The weekly high stood at INR 378,300/t on 16 July, while the weekly low was INR 373,300/t on 13 July.

Open interest declined moderately during the week, ending at 2,530 lots on 17 July compared with 2,696 lots on 13 July. The movement suggested that the sharp price swings were accompanied by selective participation rather than a sustained build-up of fresh positions.

Domestic consumers largely continued with calibrated procurement, tracking global price movements and replenishing inventories on a need basis amid volatile international cues.

SHFE zinc trends

On the Shanghai Futures Exchange (SHFE), zinc prices strengthened during the reporting week as improving sentiment and firm global market cues supported the market.

SHFE zinc stood at $3,443/t on 13 July before moving higher during the week. Prices were reported at around $3,420/t on 14 July based on the earlier available series, before recovering to $3,460/t on 15 July. Prices subsequently eased marginally to $3,453/t on 16 July before rising to $3,476/t on 17 July.

The overall recovery reflected improving sentiment across the Chinese market, although downstream purchasing remained measured amid concerns over the pace of demand recovery and broader macroeconomic uncertainty.

Market updates

Market sentiment remained mixed during the week. Continued declines in LME warehouse inventories provided underlying support to zinc prices and reinforced expectations of tightening exchange availability. However, the market remained vulnerable to profit-booking, with prices unable to sustain the recovery seen during the second half of the week.

The sharp recovery on 16 July highlighted renewed buying interest, but the subsequent decline on 17 July indicated that market participants remained cautious at higher price levels. MCX zinc followed the volatile international trend, with domestic prices recovering mid-week before correcting sharply on the final trading day.

Meanwhile, the continued drawdown in LME inventories remained a key supportive factor for the zinc market. However, the impact of tighter exchange stocks was partly offset by cautious downstream buying and broader uncertainty across global base metals markets.

Overall, zinc prices remained supported by declining exchange inventories and firm underlying physical market conditions, but short-term volatility increased as participants balanced supply concerns against profit-booking and uncertain demand prospects.

Outlook

BigMint expects LME zinc prices to remain volatile in the near term, with continued exchange inventory drawdowns providing underlying support. However, the market may remain sensitive to profit-booking, movements in the US dollar, broader base-metal sentiment and developments in Chinese downstream demand.

Immediate support is expected around the $3,500-3,530/t range, while resistance is seen near $3,590-3,630/t. Inventory movements, Chinese demand, global macroeconomic developments and the pace of physical buying will remain key indicators for zinc’s near-term price direction.

Leave a Reply