- Indonesia lifts benchmark prices for 2nd half of Jul’26 for most grades

- Coal stocks at Indian power plants inch down w-o-w but remain sufficient

Indian portside prices of Indonesian-origin thermal coal displayed mixed trends during the week ended 17 July 2026, as subdued domestic buying interest and ample availability of domestic coal continued to suppress import demand. Most consumers preferred to rely on Coal India supplies and existing inventories, limiting fresh import enquiries despite rising international price indications.

Mixed price movements reflect diverging demand across coal grades

Price movements varied across Indonesian coal grades, reflecting differences in end-user demand and competition from alternative fuels.

Prices of 5,000 GAR Indonesian coal declined by around INR 50/t w-o-w, settling at approximately INR 10,500/t at Kandla and INR 10,400/t at Vizag. The decline was primarily driven by limited buying activity and increased competition from higher-calorific-value South African 4,800 NAR coal, which remained competitively priced for several industrial consumers.

Similarly, 4,200 GAR coal prices eased by around INR 200/t, reaching nearly INR 8,700/t at Kandla and INR 8,600/t at Vizag, as weak industrial demand and comfortable domestic coal availability reduced spot procurement requirements.

In contrast, 3,400 GAR Indonesian coal prices increased by around INR 150/t to approximately INR 7,000/t at Navlakhi. The increase was supported by limited availability of lignite under existing allocation quotas and improved procurement from the ceramic sector, which continued to favour lower-calorific-value imported fuel.

A market participant noted, “Indonesian miners have started raising FOB offers following a revival in Chinese procurement after the recent price correction. However, the domestic market has yet to absorb these higher replacement costs, preventing traders from passing on the increase to Indian buyers.”

Another stated, “Prices are expected to gradually strengthen as a firmer US dollar has raised import costs and renewed Chinese buying is tightening export availability, although weak underlying demand in India continues to restrict immediate price gains.”

Freight costs rise amid renewed geopolitical tensions

Freights strengthened during the week, with Supramax rates on the East Kalimantan-Navlakhi route increasing by around $2.5/t w-o-w to nearly $20/t. The rise was largely attributed to renewed geopolitical tensions in the Middle East, particularly escalating concerns surrounding the US-Iran situation, which increased uncertainty in global shipping markets and lifted freight premiums.

Port inventories decline as imports remain restrained

India’s thermal coal inventories at major ports declined by 6.1% w-o-w to 14.15 million tonnes (mnt) in Week 28 from 15.07 mnt a week earlier. The reduction primarily reflected lower import arrivals alongside steady cargo offtake, as consumers continued to procure only immediate operational requirements while relying on adequate domestic coal supplies.

Regular dispatches from Coal India and the ongoing monsoon season further reduced the urgency for imported cargoes, preventing any meaningful inventory build-up despite lower port stocks.

Ample power plant stocks continue to provide supply cushion

Coal inventories at Indian thermal power plants declined marginally by around 1.4% w-o-w to approximately 42 mnt as of 16 July 2026, equivalent to nearly 13 days of consumption. Although inventories moderated during the week, stock levels remained adequate to comfortably meet power sector requirements.

However, around 28 thermal power plants continued to report critical inventory levels, indicating localised logistical and distribution challenges rather than any structural shortage in domestic coal availability.

Global market turns firmer on improving export fundamentals

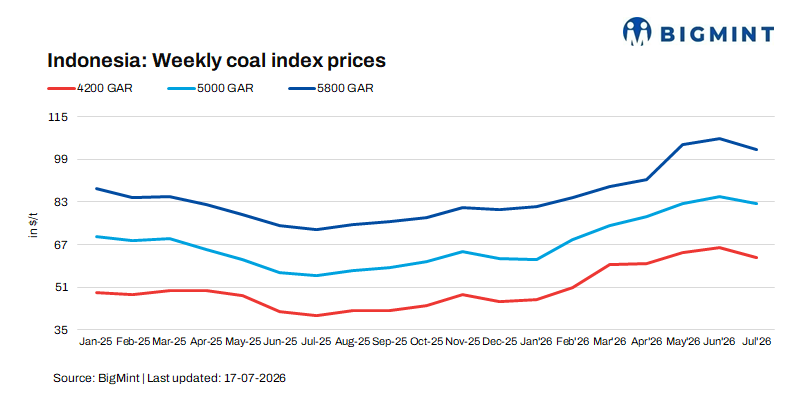

The international thermal coal market strengthened during the assessment week, with Indonesian benchmark prices for 5,800 GAR, 4,200 GAR and 3,400 GAR coal rising by around $0.5-1/t w-o-w. The improvement was supported by stronger Chinese procurement following the recent correction, firmer FOB offers from Indonesian miners and a gradual tightening in spot export availability.

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) raised HBA reference prices for most thermal coal grades in the second half of July. The 6,322 kcal/kg GAR benchmark increased 4% to $131.85/t, supported by tighter spot supply, resilient Asian utility demand and continued uncertainty over Indonesia’s evolving export policy. Meanwhile, HBA-I (5,300 GAR) slipped 1% to $89.9/t, marking its first decline since February 2026, while HBA-II (4,100 GAR) rose nearly 1% to $63.25/t and HBA-III (3,400 GAR) surged 8% to a record $45.08/t.

Outlook

Indian portside thermal coal prices are expected to remain largely stable with a marginal upward bias, supported by firmer Indonesian FOB offers, higher freight costs, a stronger US dollar and renewed Chinese buying. However, ample domestic coal availability, comfortable power plant inventories, monsoon-driven demand softness and subdued industrial consumption are likely to cap any significant price gains in the near term.

Leave a Reply