- Rising inventories, lower cost support prompt list price cuts, higher trade discounts

- Buyers defer purchases in hopes of price cuts despite INR 2,100/t drop in July so far

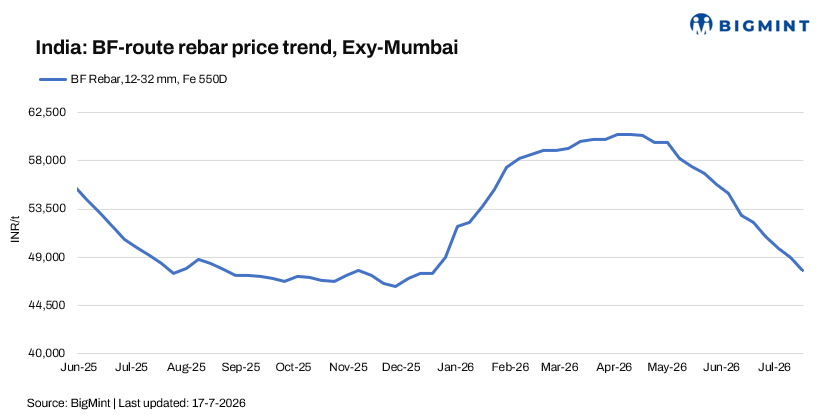

India’s blast furnace (BF)-route rebar market remained under pressure during the assessment week ended 17 July 2026, as weak construction activity amid the monsoon, cautious distributor procurement, and comfortable inventory levels continued to weigh on demand. BigMint’s benchmark assessment for BF-route rebar (IS 1786 Fe550D, 12-32 mm) declined by INR 1,00/t w-o-w to INR 47,900/t ex-Mumbai (distributor-to-dealer, excluding GST).

In response to sluggish buying interest, major steelmakers reduced list prices further by INR 1,000-1,500/t ($ 10-15/t) in mid-July to improve sales and maintain dispatch volumes. Primary steelmakers reported an increase in finished steel inventories as previously booked project orders were largely executed, while fresh order inflows remained weak. Consequently, mills increased trade discounts and adopted more competitive pricing strategies to improve inventory turnover and sustain dispatch volumes.

Demand across western, southern, and central India remained largely need-based, with distributors limiting purchases to confirmed project requirements. Buying interest continued to be restrained as market participants anticipated further price corrections, while project execution slowed due to persistent rainfall and reduced construction activity.

Despite Mumbai BF-route rebar prices declining by around INR 2,100/t so far this month, buying interest has remained subdued, with procurement continuing on a strictly need-based basis as market participants anticipate further price corrections.

Factors driving market

1. IF route rebar prices decline: IF-route rebar prices fell across major regions during the week , while trading activity remained limited to moderate throughout the week. A wide bid-offer gap encouraged active negotiations between buyers and sellers, with most transactions concluded at levels below the initial offer prices.

However, the overall decline in prices remained limited as tight raw material availability and firm input costs restricted mills from offering steeper discounts. Mill inventories were maintained at around 10-15 days, while order booking visibility remained limited to approximately 3-5 days, indicating continued short-term procurement.

In Mumbai, IF-route rebar trade prices declined by INR 200/t ($2/t) w-o-w to INR 42,700/t ($455/t) ex-works as of 16 July.

Meanwhile, the BF-IF rebar price spread in Mumbai narrowed further w-o-w to INR 4,400/t ($45). IF-route rebar continues to hold a 65-70% share of India’s long steel market, remaining the dominant supply route.

2. Raw material prices weaken: Raw material cost support weakened following NMDC’s reduction in domestic iron ore prices for July, while pellet availability remained comfortable across key producing regions. The decline in input costs enabled primary steelmakers to announce fresh reductions in rebar list prices amid slow market demand.

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 4,900/t ($53/t) ex-mines as of 11 July. Meanwhile, premium hard coking coal (PHCC) prices declined by $8/t w-o-w to $250/t CNF Paradip, further easing production costs for BF-route steelmakers.

Project update

The pipeline for infrastructure projects remained strong, driven primarily by the announcement of key highway projects. Key developments included the INR 14,115 crore Delhi-UP highway approval, Ashoka Buildcon’s INR 2,360 crore Vadhavan Port Connectivity Expressway contract, Ceigall India’s INR 704.7 crore Arunachal Pradesh highway project, Coal India’s INR 2,831 crore Jalaun Solar Park, and HUDCO’s INR 1 lakh crore infrastructure funding MoU with Odisha, highlighting sustained investment across transport, energy, and urban infrastructure.

Outlook

Market participants expect the BF-route rebar market to remain subdued through the rest of July, with monsoon-related disruptions continuing to weigh on construction activity and procurement sentiment. Buying is likely to remain need-based, while prices are expected to stay weak until distributor inventories decline and project execution gathers pace.

Leave a Reply