- Smelters ramping up production, restarting facilities

- Power costs remain major challenge for smelters

The US aluminium industry is showing early signs of revival following the introduction of higher import tariffs, but the country remains a long way from achieving self-sufficiency.

In April 2025, the US imposed a 25% tariff on aluminium imports, which was subsequently raised to 50% in July. The move was aimed at supporting domestic producers and reviving primary aluminium production.

The tariffs quickly lifted domestic aluminium premiums, improving smelter economics and making the restart of idle capacity more attractive. The Iran conflict further reinforced the need for greater domestic production by exposing vulnerabilities in global aluminium supply chains.

As a result, around 125,000 t/year of previously idle aluminium capacity is now being brought back online.

- Century Aluminum’s Mt. Holly smelter, which had been operating at roughly 75% of capacity, is ramping up to full production by adding approximately 50,000 t/year.

- Another significant development is the planned restart of the New Madrid smelter in Missouri, which has remained idle since 2016 due to high operating costs and unfavourable market conditions. The first potline is expected to resume operations in late 2026 with an initial capacity of around 75,000 t/year.

- Looking further ahead, the largest addition could come from a new greenfield project. Emirates Global Aluminium (EGA) and Century Aluminum have announced plans to build a 750,000 t/year primary aluminium smelter in Inola, Oklahoma. Construction is expected to begin by the end of 2026, with production targeted before 2030. If completed, it would be the first new primary aluminium smelter built in the US in nearly five decades.

While these developments signal renewed investment in domestic production, they represent only a small step toward reducing the country’s reliance on imports.

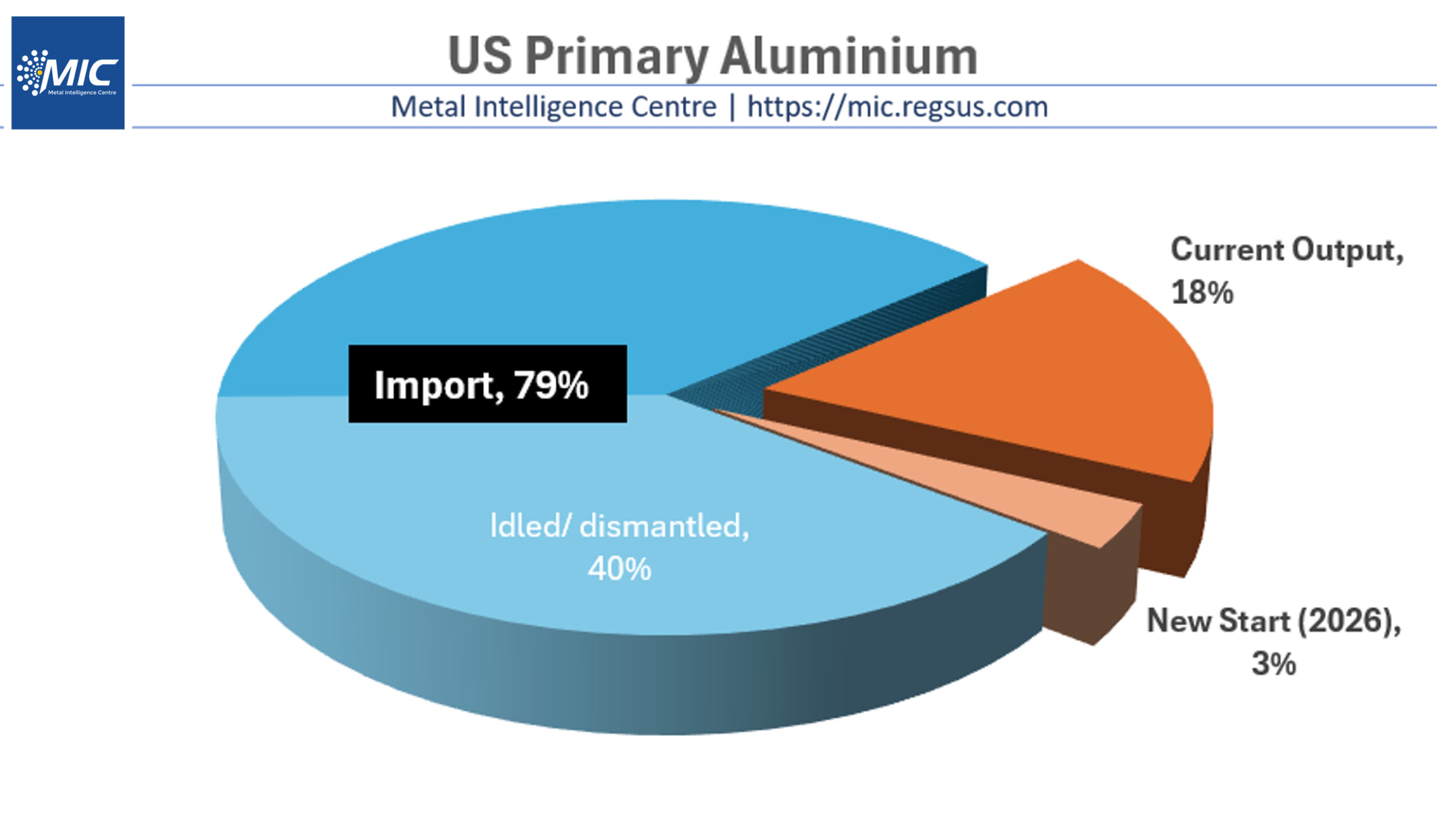

In 2025, the US produced just 664,000 t of primary aluminium, meeting only 18% of domestic consumption. To bridge the gap, the country imported approximately 3.03 million tonnes (mnt) of aluminium.

Moreover, a substantial share of existing US smelting capacity remains idle due to unfavourable production economics, particularly high electricity costs. These facilities alone have the potential to supply nearly 40% of current US aluminium demand, highlighting that restarting existing assets may offer a faster and more cost-effective solution than building entirely new smelters.

Ultimately, tariffs have provided the initial incentive for domestic production to recover, but long-term success will depend on competitive power costs, favourable operating economics and the successful restart of idle capacity. Until these structural challenges are addressed, the US is likely to increase domestic aluminium output while remaining heavily dependent on imports.

Note: This article has been published as part of a content partnership between Metal Intelligence Centre and BigMint.

Leave a Reply