- EU safeguard quotas keep export bookings muted

- Higher zinc costs fail to lift prices

India’s coated flat steel market remained subdued during the week ended 16 July 2026, with transaction levels largely unchanged as persistent demand weakness continued to weigh on market activity. The ongoing monsoon season and muted construction activity kept buying interest low, resulting in sluggish trading across major markets. Market participants continued to report weak enquiries and slow material movement, with the absence of any demand-side trigger preventing any meaningful improvement in market sentiment.

Price update

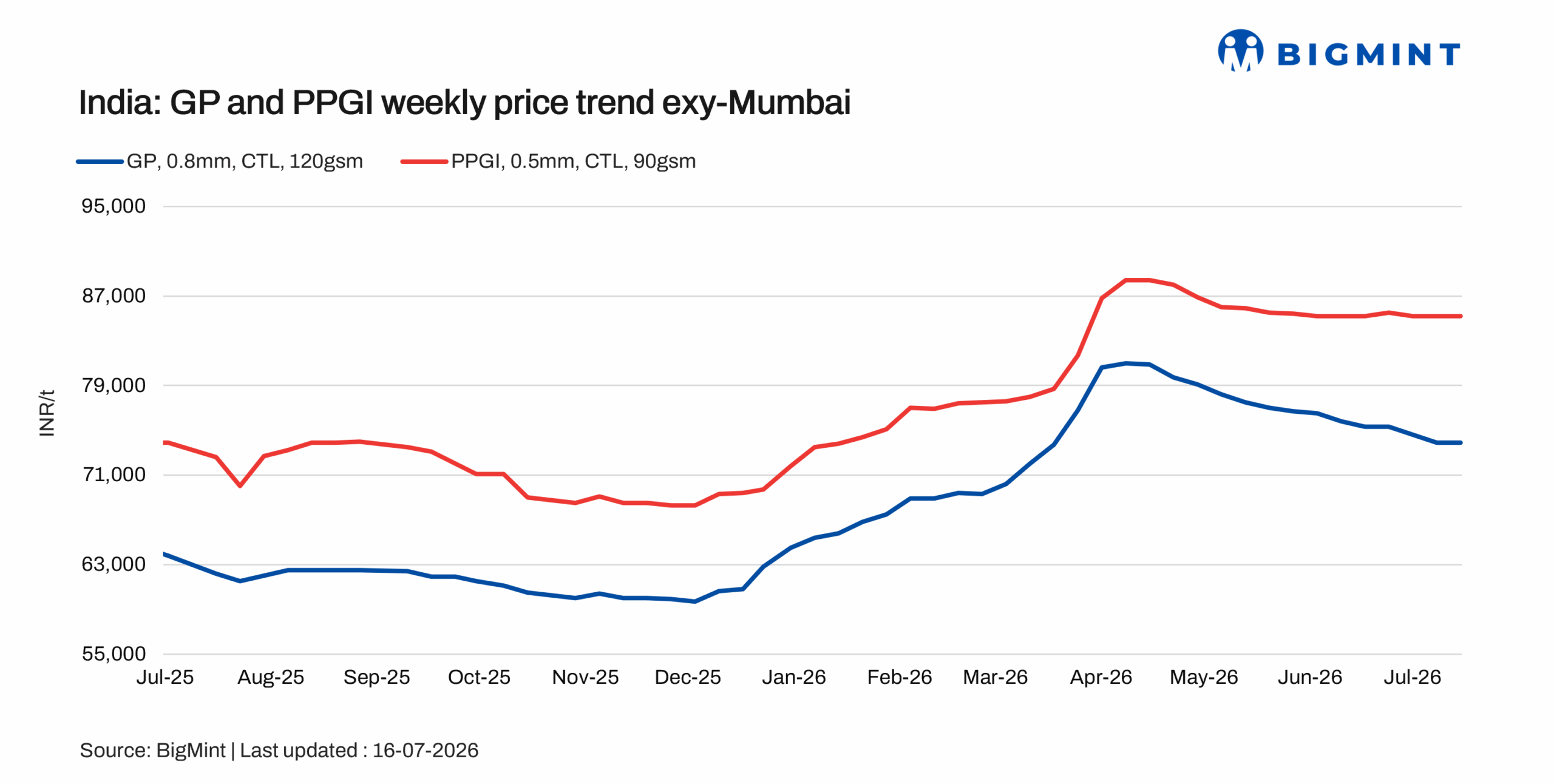

BigMint’s benchmark assessment for Mumbai GP coil (0.8 mm/CTL, 120 GSM, IS 277) remained stable w-o-w at INR 73,900/t ex-Mumbai, as subdued demand and slow market activity kept transaction levels unchanged.

Meanwhile, Mumbai PPGI (0.5 mm/CTL, 90 GSM, IS 14246) also remained stable w-o-w at INR 85,200/t, with weak buying interest and limited trading activity restricting any significant price movement.

Similarly, Mumbai BGL (0.5 mm/CTL, 1220 mm, AZ150) remained unchanged w-o-w at INR 89,500/t, as sluggish demand and muted booking activity continued to keep prices range-bound during the week.

Export offers:

HDGI export offers to the EU remained stable w-o-w at $790/t FOB India. European buyers continued to assess their allocated quota volumes under the EU’s new safeguard regime, with no fresh bookings reported during the assessment week. As a result, export activity remained limited and market sentiment was mixed.

Raw material prices

India’s zinc ingot (99.995%) prices increased by INR 5,000/t w-o-w to INR 382,000/t ex-Delhi, according to BigMint’s latest assessment. The increase was driven by Hindustan Zinc Ltd’s (HZL) latest benchmark price revision, supported by tightening global supply fundamentals and continued constraints on imported material availability. Despite firmer zinc prices, downstream demand from galvanisers and alloy manufacturers remained largely need-based, as monsoon-related disruptions continued to weigh on buying activity.

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) declined by INR 300/t w-o-w to INR 57,900/t ($602/t) ex-Mumbai, exclusive of 18% GST, as weak spot demand and competitive market offers continued to pressure prices. Trade offers were heard in the range of INR 54,900-58,800/t ($571-611/t).

Meanwhile, CRC (IS513, Grade O, 0.9 mm/CTL) remained stable w-o-w, reflecting cautious market sentiment and muted buying activity. BigMint’s benchmark assessment stood unchanged at INR 65,000/t ($676/t) ex-Mumbai, exclusive of 18% GST, as of 14 July.

Market update:

The Indian coated flat steel market remained subdued during the assessment period, with buying activity continuing to remain weak across major regions. Material lifting was limited as demand from the construction and infrastructure sectors remained affected due to monsoons. Stockists largely refrained from building fresh inventories, preferring to align procurement with prevailing consumption levels. As a result, inventory levels remained comfortable, with adequate material availability across the supply chain.

Regional sentiment remained uniformly weak across the western, northern and southern markets. Market participants reported sluggish trading activity, with enquiries remaining limited and transaction volumes subdued. While the galvanised (GP) segment continued to witness dull demand, some buying interest was reported in the colour-coated (PPGI) segment from select distribution partners in the western region. However, this was insufficient to improve the overall market sentiment.

The spread between hot-rolled coil (HRC) and galvanised (GP) coil widened further during the week. BigMint’s benchmark HRC assessment stood at INR 57,900/t ex-Mumbai, while GP coil was assessed at INR 72,400/t ex-Mumbai, widening the HRC-to-GP spread to INR 14,500/t. The wider spread reflected the relative stability in coated steel prices despite softer HRC values, although weak downstream demand continued to limit any meaningful recovery in coated steel transactions.

Looking ahead, market participants expect demand to remain subdued over the near term as monsoon-related disruptions continue to affect construction activity. Procurement is likely to remain consumption-driven, while adequate material availability and cautious inventory management are expected to keep trading activity muted across the coated flat steel market.

Outlook

The coated flat steel market is expected to remain range-bound in the near term, with monsoon-related disruptions continuing to cap demand. While higher zinc prices may increase production costs, weak consumption is likely to limit mills’ ability to pass on the increase. Market sentiment will hinge on a post-monsoon recovery in domestic demand and the pace of export bookings, particularly to the EU under the revised safeguard regime.

Leave a Reply