- Portside inventories in India down 6.1% w-o-w on lower arrivals

- Sponge iron prices in eastern India drop w-o-w

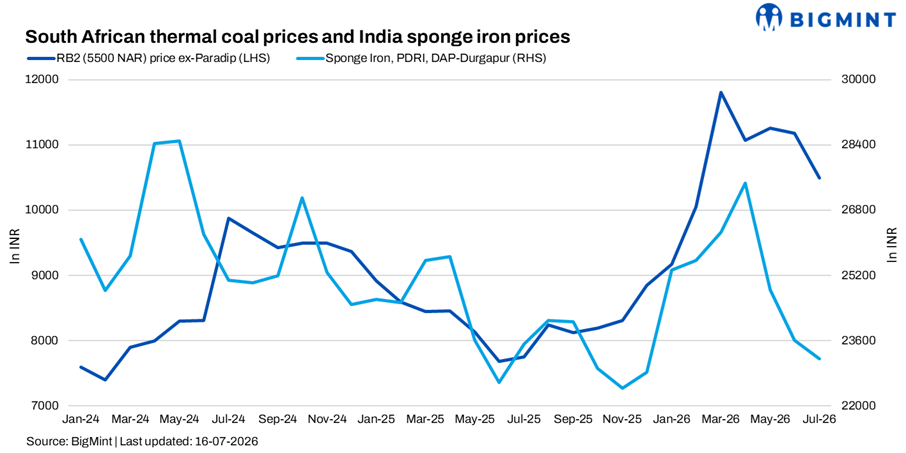

South African thermal coal prices at Indian ports remained largely stable during the week ended 16 July despite firm global FOB offers, as weak sponge iron demand and comfortable domestic coal availability continued to suppress buying interest.

While overseas suppliers raised offer levels following higher freight and energy costs amid geopolitical tensions, Indian buyers largely stayed away from the market, resulting in a widening gap between bids and offers.

As per BigMint’s assessment, RB2 (5,500 NAR) ex-Paradip remained stable at INR 10,450/t, while RB3 (4,800 NAR) increased by INR 50/t w-o-w to INR 8,900/t. At Vizag, RB2 rose by INR 100/t to INR 10,350/t, while RB3 remained unchanged at INR 8,850/t.

India’s thermal coal inventories at major ports declined 6.1% w-o-w to 14.15 mnt from 15.07 mnt in the previous week, primarily due to lower import arrivals and steady cargo offtake. However, inventory levels remained comfortable as consumers continued relying on domestic coal and restricted imports to immediate operational requirements.

Global offers strengthen, buyers stay away

Market participants reported that the imported coal market remained largely inactive, with almost no fresh enquiries or bookings during the week. FOB Richards Bay Coal Terminal (RBCT) offers for 5,500 NAR coal increased to around $88-90/t, while 4,800 NAR material was heard at $68-70/t FOB. On a CFR basis, the lowest offers for 5,500 NAR coal were heard around $105-106/t, whereas Indian buyers were bidding closer to $99-101/t, leaving a significant bid-offer gap.

Participants attributed the increase in FOB offers to higher energy costs and geopolitical tensions, although the higher prices failed to generate buying interest in India. Traders noted that liquidity at portside markets remained weak, with buyers continuing to favour domestic coal over imported material.

Spot offers at eastern ports were heard around INR 10,500-10,600/t ex-Paradip for RB2, while Dhamra offers were near INR 11,000/t. At Mangalore, RB2 offers were heard around INR 10,400-10,600/t, while RB3 was indicated near INR 9,000/t. Despite the firmer offers, market participants reported negligible transactions during the week.

Domestic coal continues to dominate

Domestic coal remained the preferred fuel source due to its competitive pricing and reliable availability. BigMint assessed 5,000 GCV coal unchanged w-o-w at INR 5,500/t exw Bilaspur, while 4,500 GCV coal remained steady at INR 4,050/t.

Meanwhile, the sponge iron market weakened further, with PDRI DAP-Durgapur declining by INR 400/t w-o-w to INR 22,700/t. Weak finished steel demand and continued pressure on producer margins kept coal procurement strictly need-based, further weighing on imported thermal coal consumption.

Outlook

The imported South African thermal coal market is expected to remain subdued in the coming weeks unless buying interest revives. Although firmer global FOB prices are supporting seller offers, comfortable domestic coal availability and weak sponge iron demand are likely to keep Indian buyers on the sidelines. Market participants will also monitor movements in energy prices and geopolitical developments, which could continue to influence international offer levels.

Leave a Reply