- Higher replacement costs support secondary zinc prices

- Buyers continue order-linked procurement amid resistance at elevated levels

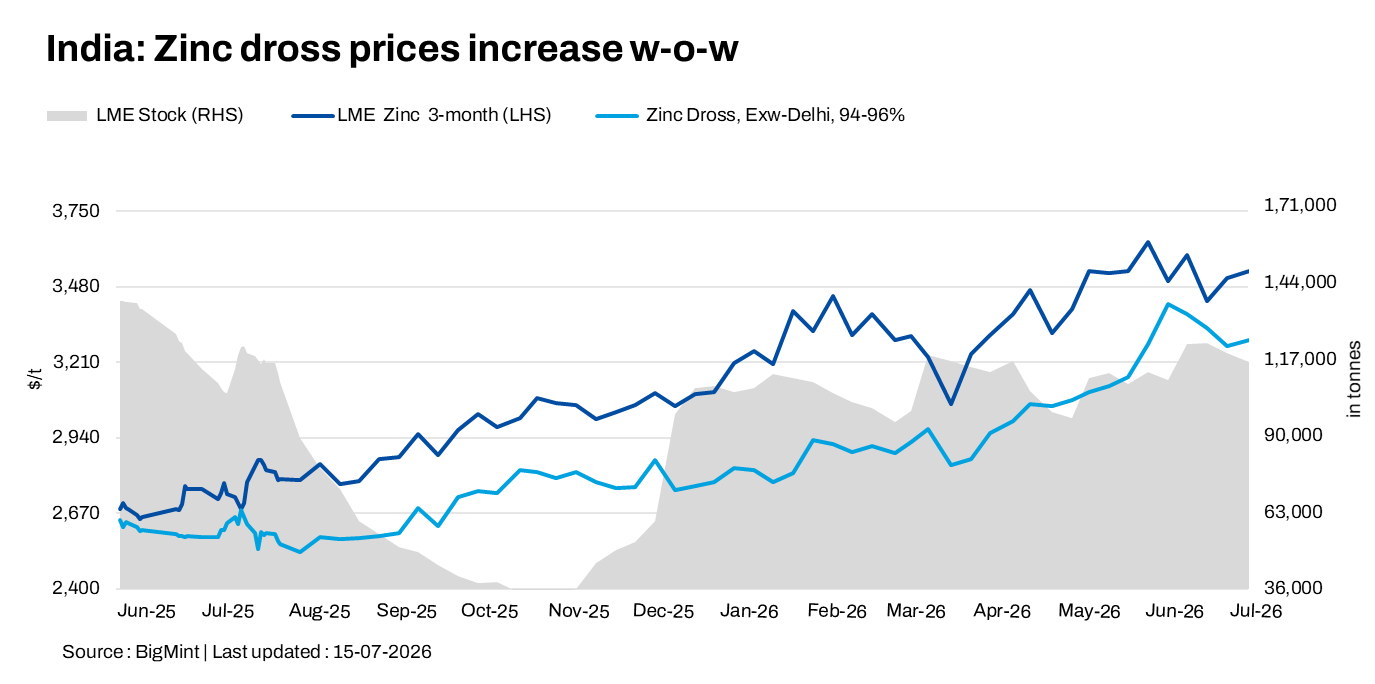

India’s zinc dross and zinc oxide prices extended their gains in the week ended 15 July 2026, supported by firmer London Metal Exchange (LME) zinc prices, continued declines in exchange inventories and higher replacement costs for secondary material. Despite the upward price movement, downstream buying remained disciplined, with most consumers procuring material only against confirmed production schedules as higher offers met resistance from value-conscious buyers.

Benchmark three-month LME zinc prices averaged around $3,573/t during the assessment week ended 15 July, up from approximately $3,536/t in the previous assessment period. Meanwhile, LME zinc inventories declined to 112,450 t on 15 July from 115,925 t on 8 July, extending the recent trend of warehouse drawdowns and reinforcing sentiment across the zinc value chain.

The firmer international market translated into higher replacement costs for domestic secondary zinc products, encouraging suppliers to revise offers upward. However, buyers remained selective, limiting purchases to immediate production needs as they assessed the sustainability of the recent rally in primary zinc prices.

Zinc dross, oxide price movements

Domestic zinc dross prices increased by INR 5,500/t w-o-w to INR 318,000/t ex-Delhi from INR 312,500/t a week earlier.

Meanwhile, zinc oxide (99% Zn) prices rose by INR 2,800/t w-o-w to INR 307,800/t ex-Delhi, compared with INR 305,000/t in the previous assessment.

The sharper increase in zinc dross reflected tighter replacement economics following the rise in primary zinc prices, while zinc oxide producers passed on part of the higher raw material costs amid stable downstream consumption from rubber, chemical and allied sectors.

Scrap segment trends

In the north Indian zinc scrap market, regular-grade Big Tukdi (97-98% Zn) was heard at around INR 308,000-309,000/t ex-Delhi, while Mid Tukdi (97-98% Zn) was assessed at INR 303,000-304,000/t.

Market participants reported that scrap quotations moved broadly in line with gains in primary zinc, although transaction volumes remained moderate. Suppliers showed greater confidence in maintaining higher offers after the latest increase in benchmark zinc prices, while buyers continued negotiating aggressively for spot requirements rather than building inventories.

Market sentiment

Market sentiment remained cautiously firm during the assessment period. Traders said stronger LME prices and successive increases in domestic primary zinc quotations had improved replacement costs, making it difficult for sellers to offer material at previous levels. However, higher prices also widened the bid-offer gap, with several consumers delaying purchases in anticipation of better clarity on the direction of international markets.

Participants noted that mills were increasingly reluctant to discount fresh material, citing higher input costs, while traders largely aligned their offers with replacement values instead of competing aggressively on price. Although enquiries improved following the latest rise in primary zinc, conversions into confirmed deals remained largely restricted to immediate production requirements.

Some processors also indicated that availability of quality zinc-bearing scrap remained adequate, preventing any significant supply squeeze despite the stronger pricing environment. As a result, the market stayed fundamentally balanced, with price gains driven more by replacement-cost adjustments than by any meaningful improvement in underlying demand.

Outlook

In the near term, zinc dross and zinc oxide prices are expected to remain supported by elevated LME zinc prices and firm replacement costs. Continued declines in exchange inventories could lend further support to global benchmark prices. However, domestic secondary zinc prices are likely to track primary zinc movements closely, with upside expected to remain gradual unless downstream consumers shift from order-linked buying to inventory replenishment. Market participants will also monitor whether recent price gains can be sustained without a corresponding improvement in end-user demand, as prolonged buying resistance could temper further increases.

Leave a Reply