- Weak domestic demand keeps annualised output subdued at 80 mnt

- Chinese exports and rising protectionism intensify pressure on Japanese mills

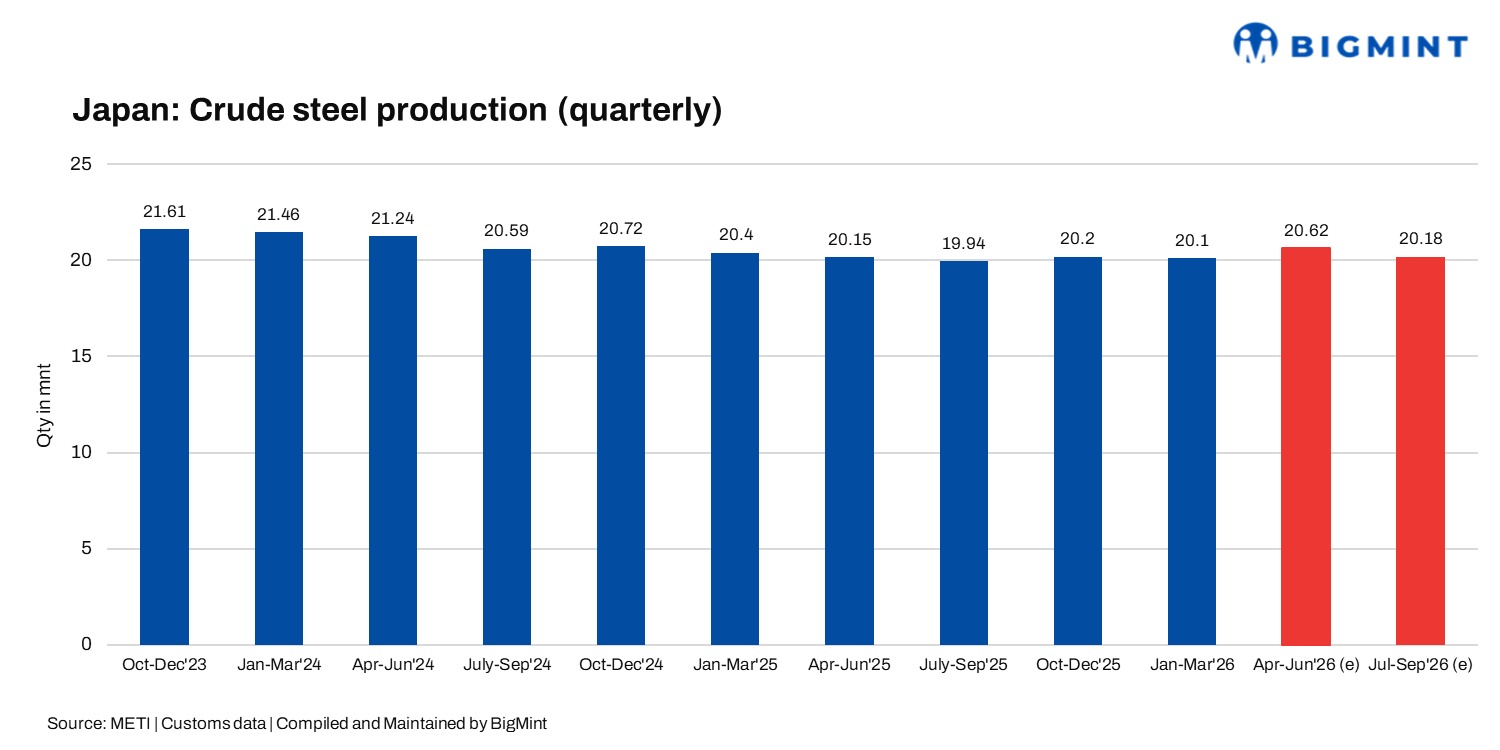

Japan’s Ministry of Economy, Trade and Industry (METI) has forecast crude steel production for the July-September quarter at 20.18 million tonnes (mnt), up 1.3% y-o-y, marking the second consecutive quarter of annual growth. The ministry also revised its April-June production estimate upward by around 600,000 tonnes (t) to 20.62 mnt, putting the quarter on track to record Japan’s first year-on-year increase in crude steel output in 10 quarters.

Despite the improvement, annualised production remains close to 80 mnt, underscoring the structural weakness facing Japan’s steel industry. Domestic demand remains subdued, exports continue to lose momentum, and Japanese mills face intensifying competition from Chinese steel alongside expanding protectionist measures across key export markets. The subdued outlook follows Japan’s loss of its position as the world’s third-largest crude steel producer to the United States last year, highlighting the gradual erosion of the country’s global steel footprint.

Domestic demand stabilises but remains insufficient to lift production

METI forecasts total steel demand during July-September at 18.05 mnt, down 3.1% y-o-y but marginally higher than the previous quarter. The annual decline primarily reflects an expected build-up in semi-finished steel inventories rather than any meaningful deterioration in end-use demand.

Demand conditions remain mixed across major steel-consuming sectors. Ordinary steel demand is projected to decline 3.0% y-o-y to 14.23 mnt, as continued weakness in construction outweighs relatively stable manufacturing activity. Within manufacturing, industrial machinery consumption is expected to improve gradually alongside recovering investment, while automotive steel demand is forecast to remain broadly unchanged. Shipbuilding demand, however, is expected to decline by around 1.5% y-o-y as labour shortages continue delaying vessel construction.

Recent industry data also suggest domestic steel consumption has stabilised despite subdued production. Japan’s apparent steel consumption reached 4.82 mnt in May, exceeding production growth during the month, indicating that domestic demand has become relatively more resilient even as overall steel output remains constrained.

Exports remain the industry’s principal weakness

Japan’s export market continues to present the largest challenge for steelmakers. METI expects ordinary steel exports to decline 6.3% y-o-y during the third quarter as weak demand across Asia combines with expanding trade protection measures in several importing countries.

The ministry warned that persistently high Chinese steel exports continue to intensify competition across regional markets, limiting Japanese mills’ ability to offset weak domestic demand through overseas sales. This pressure is being compounded by growing trade barriers, including higher tariffs and safeguard measures introduced across several key steel-importing markets.

The deterioration is also evident in Japan’s trade statistics, as steel exports have remained below year-earlier levels throughout much of 2026, while the export ratio has declined to around 37% of crude steel production compared with approximately 40-42% during much of 2025, highlighting the industry’s growing reliance on domestic demand. Although stronger manufacturing activity in the United States continues to support demand for steel-intensive products such as automobiles, industrial machinery and high-value manufactured goods, direct steel export opportunities remain constrained by trade restrictions and intensifying global competition. The continued application of US tariffs on Japanese automobiles also limits the potential upside for steel demand from one of Japan’s most important manufacturing sectors.

Competition intensifies as global steel production shifts

Japan’s production outlook also reflects broader changes in the global steel industry. While Japanese crude steel output has remained subdued, steel production has expanded across several competing economies, particularly India and the United States, supported by stronger manufacturing activity, infrastructure spending and resilient domestic demand. The United States overtook Japan as the world’s third-largest crude steel producer in CY25, while India continues to strengthen its position as the fastest-growing major steel-producing nation. By contrast, Japan continues to contend with sluggish domestic demand, weakening exports and increasing competition from Chinese steel across Asian markets, limiting any meaningful recovery in production.

Outlook

Japanese crude steel production is expected to remain subdued through the July-September quarter despite recording a second consecutive year-on-year increase. Weak construction activity, sluggish export orders and rising inventory levels are expected to continue limiting production, while expanding protectionist measures and sustained Chinese steel exports are likely to intensify pressure on Japanese mills. Although stable automotive demand and improving machinery consumption should provide some support to domestic steel demand, a sustained recovery in output will ultimately depend on stronger construction activity and a meaningful improvement in export markets. Until then, annualised crude steel production is likely to remain close to the 80 mnt level, well below the levels historically associated with Japan’s position among the world’s leading steel producers.

Leave a Reply