- Manufacturing optimism boosted industrial metal sentiment

- Late-week inventory inflows trimmed further price gains

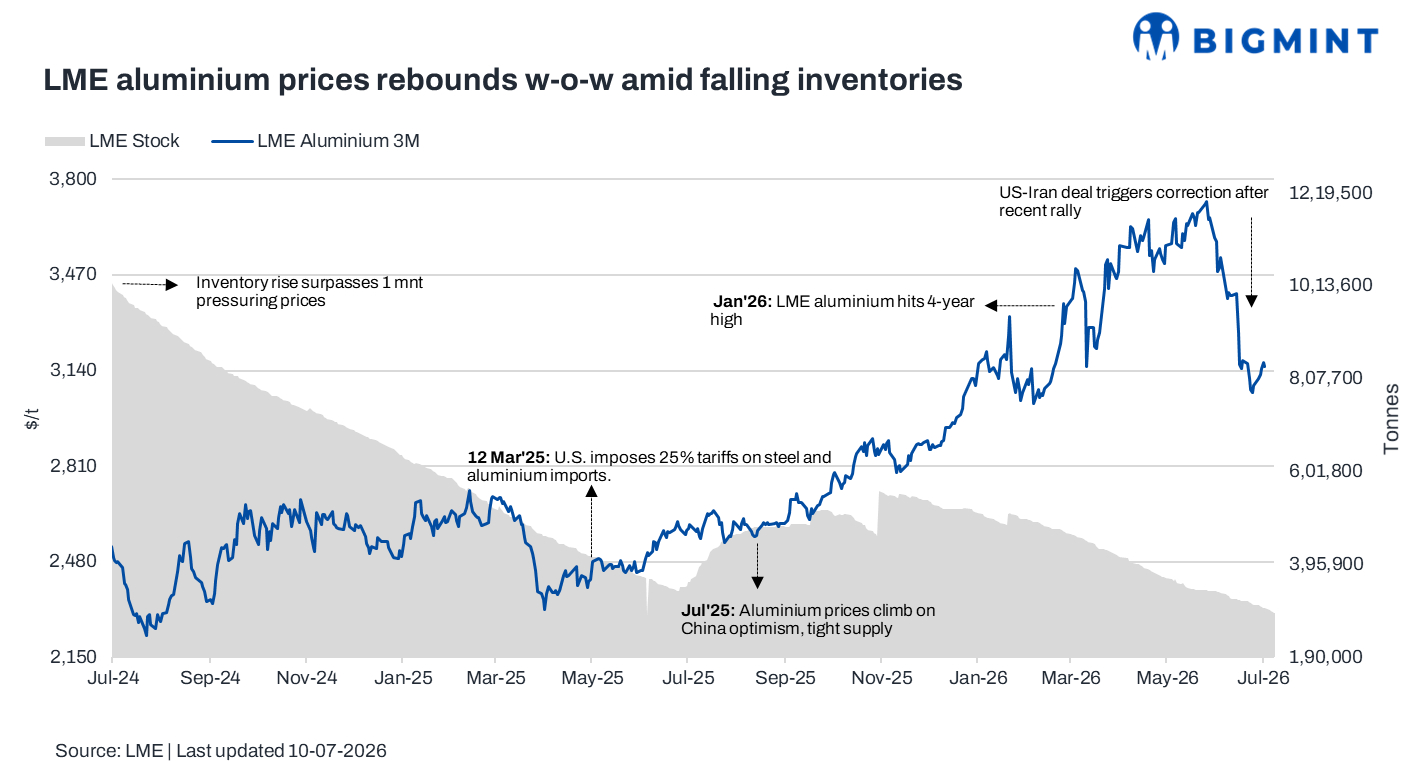

LME aluminium prices edged higher w-o-w, with the three-month contract settling at $3,142/t in the week ended 10 July 2026, up 1.4% from $3,100/t a week earlier.

Prices opened the week at around $3,113/t and climbed to an intra-week high of approximately $3,169/t on supply concerns. However, gains were partially pared towards the end of the week as fresh inflows into LME warehouses over the last 48 hours eased immediate concerns over exchange stock availability, pulling prices back to around $3,153/t.

On a weekly basis, however, LME aluminium inventories continued to decline, falling 3.6% w-o-w to 291,150 t from 301,945 t. This indicates that, despite the late-week replenishment, visible exchange stocks remained tight overall, lending underlying support to aluminium prices.

What impacted aluminium prices?

LME aluminium prices extended gains during the week ended 10 July, supported by a combination of supply-side concerns and persistent tightness in exchange inventories. Market sentiment remained underpinned by worries over the availability of primary aluminium, as production outside China continues to face structural constraints, while China’s smelting capacity remains close to its government-imposed ceiling. Expectations of tighter regional supply also kept buyers cautious despite signs of improving global production. On the macro front, easing concerns over global trade and resilient manufacturing sentiment across key economies provided additional support to industrial metals. Meanwhile, LME aluminium inventories remained below 300,000 t for another week, reinforcing expectations of a tight physical market and encouraging speculative buying. Although fresh inflows into LME warehouses towards the end of the week prompted some profit-booking.

Outlook

LME aluminium prices are expected to remain range-bound with a firm bias in the near term. Persistent tightness in exchange inventories, supply-side constraints outside China, and China’s capacity ceiling are likely to provide underlying support. However, improving primary aluminium supply, inventory inflows into LME warehouses, and evolving macroeconomic developments may limit further upside, keeping market sentiment cautious.

Leave a Reply