- Comfortable OEM inventories limit fresh procurement

- ADC12 imports surge on competitive overseas pricing

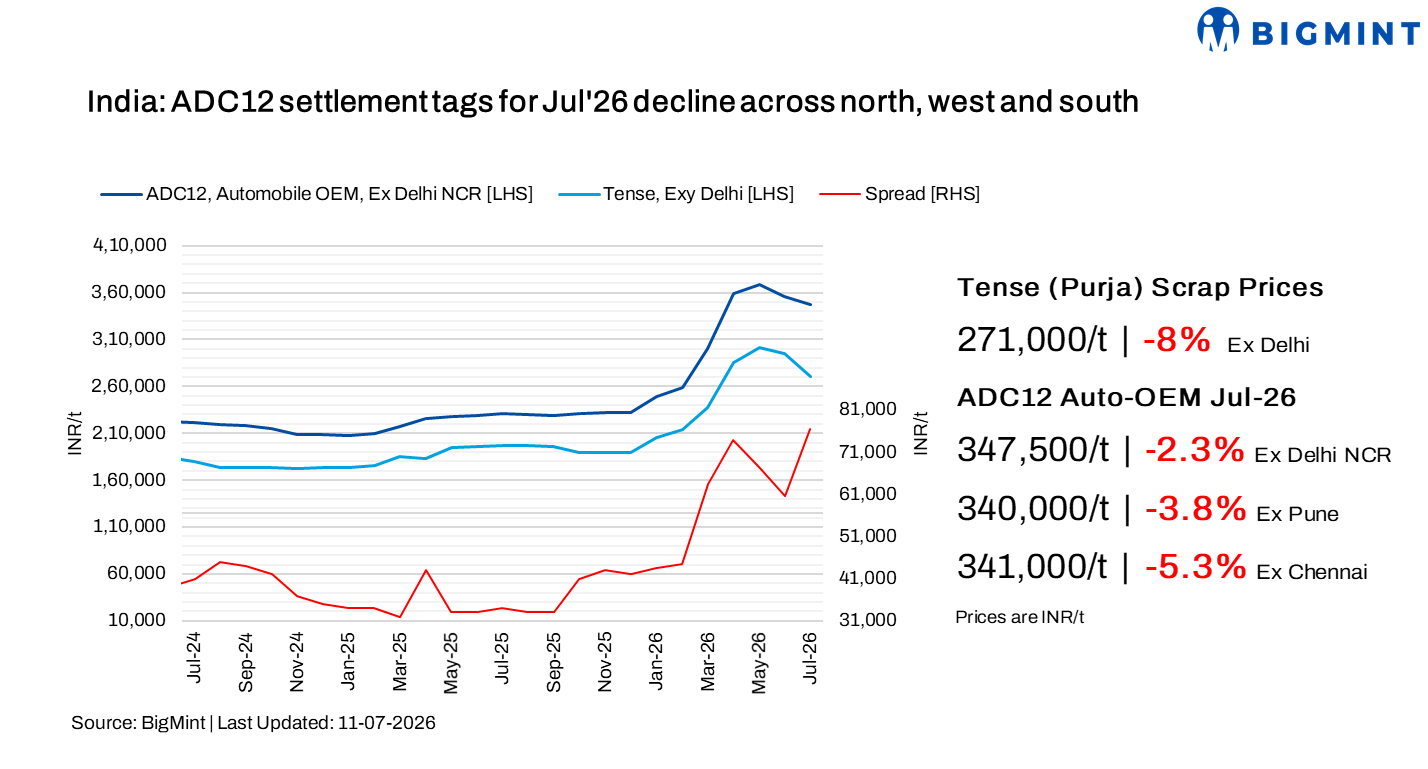

India’s ADC12 aluminium alloy ingot prices declined m-o-m in July 2026 after touching record highs in May, pressured by lower aluminium scrap costs, improved fuel availability, comfortable OEM inventories, subdued spot buying, and rising inflows of competitively priced duty-free ADC12 imports, particularly in southern India. Despite the correction, demand from the automotive sector remained healthy, while the availability of quality aluminium scrap continued to be a concern.

The spread between aluminium scrap and ADC12 alloy ingots narrowed to around INR 76,000-82,000/t in Delhi NCR and Chennai. The contraction was primarily driven by declines in both ADC12 alloy ingot and aluminium scrap prices during the month.

Market insights

ADC12 alloy ingot prices fell across major Indian markets amid softer raw material costs. Prices stood at:

- Chennai: INR 338-342/kg – all prices need to be in /t

- Delhi: INR 345-350/kg

- Pune: INR 338-340/kg

Overall, India’s ADC12 aluminium alloy market is currently trading in the INR 345,000-350,000/t range. Prices in southern India have corrected sharply, reflecting the steep decline in tense scrap prices, subdued ADC12 demand, and increased availability of competitively priced imports. Most OEMs continue to hold comfortable inventories built from previously booked Malaysian cargoes, reducing the need for fresh procurement and keeping buying activity subdued.

Meanwhile, most OEMs are yet to finalise their July 2026 ADC12 settlement prices. Negotiations have been prolonged as suppliers seek to secure higher settlement levels, while buyers continue to push for lower prices amid weaker market sentiment and expectations of further corrections.

ADC12 import bookings have also slowed in recent weeks. The correction in domestic prices has narrowed the import arbitrage, while a significant volume of previously booked cargoes is still arriving in India. Consequently, buying interest, particularly in southern India, has remained muted.

In contrast, the northern market has remained relatively firm, supported by the continued shortage of tense scrap and aluminium wheel scrap, which has helped sustain domestic ADC12 prices despite an overall weak demand environment.

In the near term, ADC12 prices are expected to remain under pressure as comfortable OEM inventories, cautious procurement strategies, and subdued spot demand continue to weigh on market sentiment, despite healthy automobile sales.

However, the medium-term outlook remains cautiously positive. Market participants are closely monitoring the European Union’s proposed 15% export duty on aluminium scrap, expected to be announced in September, along with the UAE government’s decision on whether to extend its aluminium scrap export ban beyond October 2026. Any further tightening in global scrap availability could support aluminium scrap prices and, in turn, provide renewed upside to India’s ADC12 alloy market in the coming months.

Alloy imports surge y-o-y in 5MCY’26

Imports: India’s ADC12 alloy ingot imports surged 637% y-o-y to 5,538 t during 5MCY’26, compared with 751 t in the corresponding period last year. The sharp increase was primarily driven by the widening price gap between domestic and imported material, encouraging buyers to source competitively priced ADC12 from FTA countries, particularly Malaysia.

Raw material trends

LME aluminium prices corrected in early July as concerns over Middle East supply disruptions eased following the reopening of the Strait of Hormuz and the faster-than-expected recovery at EGA’s Al Taweelah operations. The correction was further driven by profit booking after the geopolitical rally and expectations of higher global aluminium supply, supported by Slovalco’s planned restart, robust Chinese output, and expanding smelting capacity in Indonesia.

In line with the decline in imported scrap prices, domestic aluminium scrap values also eased during July, particularly for casting-grade scrap used in ADC12 production, with the sharpest corrections seen in southern India.

Among key imported grades, US-origin Tense declined by $282/t m-o-m to $2,441/t, while UK-origin Wheel scrap fell by $308/t to $3,145/t.

Meanwhile, China-origin silicon metal 553 prices decreased by $69/t to $1,357/t on a CFR Mundra basis, amid oversupply and weak downstream demand in China.

Outlook

India’s ADC12 market is expected to remain under pressure in the near term amid weaker LME aluminium prices, comfortable OEM inventories, subdued buying activity, and competitive imports from FTA countries, particularly Malaysia.

The correction in the leading automaker’s July settlement is also likely to weigh on domestic prices. However, tight availability of quality casting-grade scrap and ongoing scrap export restrictions in the UAE and proposed EU measures are expected to limit any sharp downside in ADC12 prices.

Leave a Reply