- European exporters face subdued overseas buying interest

- Seasonal slowdown continues to pressure export scrap markets

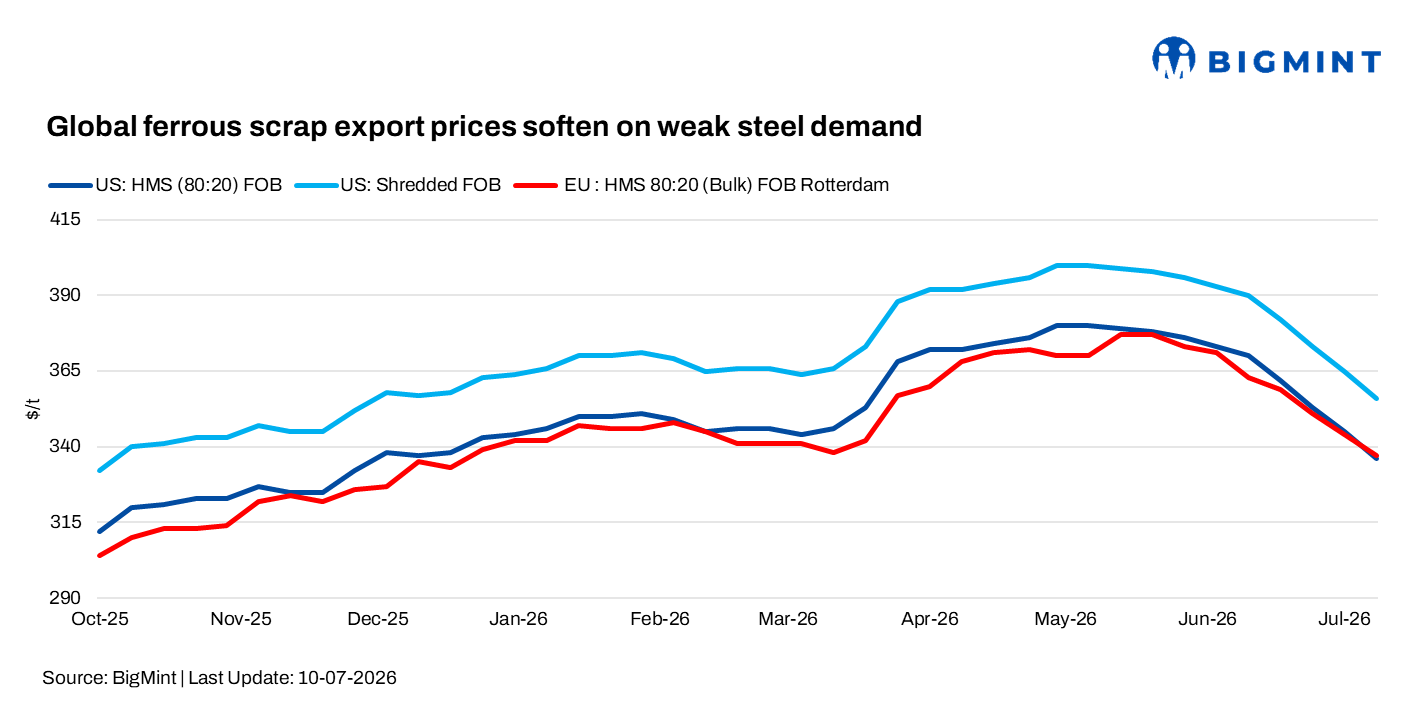

Ferrous scrap export markets remained under pressure during the week ended 10 July as weak finished steel demand, seasonal production slowdowns, and cautious mill procurement continued to weigh on trading activity.

Export prices declined across the US, Europe, and Brazil, with mills restricting purchases to immediate requirements amid comfortable scrap availability, squeezed steelmaking margins, and subdued downstream demand. Market participants expect sentiment to remain cautious in the coming weeks unless steel demand and production recover.

US

US ferrous scrap prices softened during the week, with HMS 80:20 FOB East Coast assessed at $336/t and shredded scrap FOB at $356/t, both declining by $9/t w-o-w.

Market sentiment weakened ahead of July trading as seasonal mill maintenance, extreme summer heat, and power curtailments are expected to reduce steel production and scrap consumption. Survey participants indicated that mills remain adequately supplied with scrap, while no single market factor is expected to drive prices in the near term.

Buyers and brokers remained cautious, citing ample scrap availability and limited improvement in finished steel demand, whereas sellers maintained a relatively firmer outlook. Overall, balanced scrap supply and weaker seasonal demand are expected to keep US scrap prices under pressure through July unless steel production and downstream demand recover.

Europe

European export ferrous scrap prices weakened during the week, with HMS 80:20 FOB assessed at $337/t, down $7/t w-o-w, as subdued buying interest from Turkiye and South Asia continued to weigh on market sentiment.

Weak long steel demand and squeezed mill margins kept deep-sea scrap procurement cautious, forcing exporters to lower workable price levels. Market participants believe further price corrections are possible unless finished steel demand improves.

The weaker export environment was also reflected in European dockside markets, where in the UK, HMS 80:20 dockside purchase prices declined to GBP 200-205/t ($268-275/t) DAP. Market participants indicated that dockside prices could soften by another GBP 5/t ($7/t) if export demand remains weak.

Brazil

Brazil’s ferrous scrap market weakened during the week as several domestic steelmakers reduced purchase prices following weaker-than-expected steel production and sluggish finished steel demand. Market participants also cited poor export sales and cautious buying sentiment as key factors weighing on prices.

Export offers softened, with HMS 80:20 declining to $290-295/t FOB and shredded scrap to $310-315/t FOB amid weaker demand from India. Market participants also warned that potential US tariffs on Brazilian pig iron could divert more material to the domestic market, increasing competition with scrap and further pressuring prices.

Leave a Reply