- Vietnam shifts procurement towards domestic scrap

- Above 65% of scrap exports shipped to Vietnam and Bangladesh

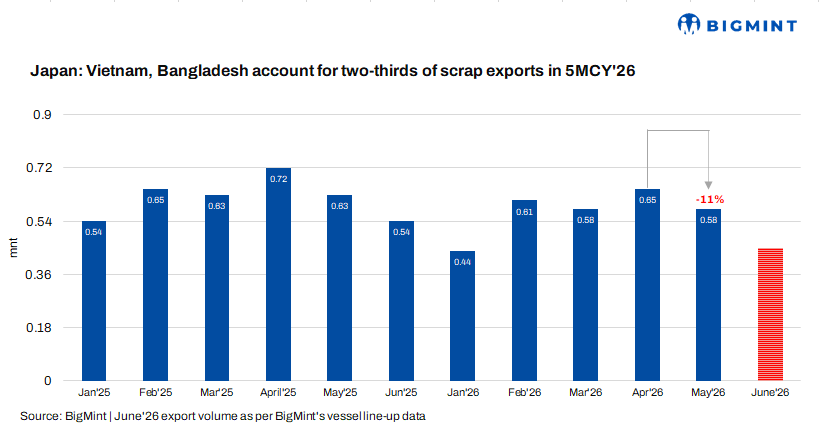

Japan’s ferrous scrap exports declined to 0.58 mnt in May 2026, down 11% m-o-m and 8.1% y-o-y, extending the downward trend as demand weakened across key Asian markets. During 5MCY’26, cumulative exports fell 10% y-o-y to 2.86 mnt, according to BigMint statistics.

Vietnam remained Japan’s largest export destination, accounting for around 40% of total May shipments. However, during 5MCY’26 (January-May 2026), exports to Vietnam declined 13% y-o-y to 1.26 mnt, as Vietnamese mills increasingly preferred domestically sourced scrap as it remained more price competitive than imported material.

Some mills also shifted part of their procurement to US deep-sea cargoes during April-May and showed greater interest in containerised scrap in June, while weak finished steel demand kept buying cautious.

Bangladesh recorded a softer May, with Japanese scrap imports declining 5% m-o-m to 0.19 mnt following strong purchases in April that helped mills build comfortable inventories. However, during 5MCY’26, imports increased 30% y-o-y to 0.70 mnt, compared with 0.54 mnt in 5MCY’25, making Bangladesh the only major export destination to register y-o-y growth. Demand remained comparatively resilient as domestic scrap availability was insufficient to support expanding steelmaking capacity, while supplies from the US and Europe remained relatively tight.

Despite the monthly slowdown, Vietnam and Bangladesh continued to strengthen their importance in Japan’s export portfolio. During 5MCY’26, the two countries imported a combined 1.96 mnt of Japanese ferrous scrap, accounting for 66% of total exports, compared with 61% during the same period last year. The higher share was primarily driven by stronger Bangladeshi demand, while exports to traditional destinations such as South Korea, Taiwan, and China continued to decline.

Elsewhere, exports to Thailand remained broadly stable at around 0.06 mnt in May and exceeded shipments to South Korea for the second consecutive month. During 5MCY’26, cumulative exports to Thailand reached 0.23 mnt, more than doubling y-o-y, supported by healthy steel demand, firm construction activity, and limited domestic scrap availability. Meanwhile, Indonesia’s share in Japan’s overall export mix moderated during the period.

Looking ahead, BigMint’s vessel line-up data indicates that Japan’s bulk ferrous scrap exports are likely to remain subdued during the rainy season. June shipments are estimated at around 0.37-0.40 mnt, while June total export volumes are projected at 0.40-0.45 mnt, — a limited improvement in overseas demand.

Export negotiations have slowed as the gap between relatively firm domestic scrap prices in Japan and weaker seaborne prices has widened. Supported by resilient domestic steel production and stable scrap consumption, local scrap prices are expected to remain firm, limiting Japan’s export competitiveness until buying interest from key overseas markets strengthens.

This article has been published in accordance with a content exchange agreement between Japan Metal Daily/Steel Daily and BigMint.

Leave a Reply