- Fresh Australia coal fixtures support Panamax freight levels

- Muted Indonesia demand weighs on Supramax sentiment

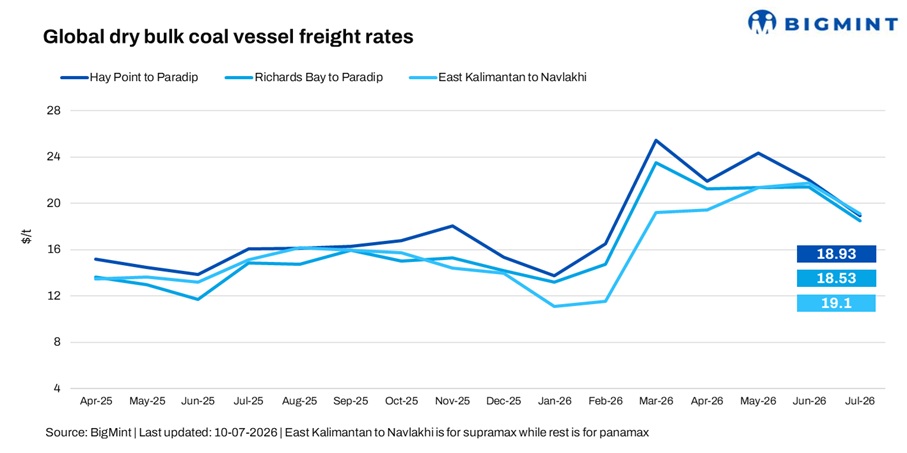

India’s dry bulk coal freight market witnessed mixed trends in the week ended 10 July 2026. Firm Australian fixtures and stronger fixing levels improved Panamax sentiment, while softer cargo activity across parts of Asia kept Supramax movement under pressure.

The Panamax market remained firm as improved cargo activity and tighter prompt vessel availability strengthened owner sentiment. However, adequate tonnage supply in the Pacific and slower fresh cargo replenishment capped further gains.

A shipbroker told BigMint, “Panamax sentiment improved slightly amid firm fixing activity, although fresh cargo flows remain key for further momentum.”

Meanwhile, Supramax sentiment remained cautious as Pacific activity stayed subdued amid slower cargo flows. However, weather-related vessel delays and port congestion across parts of Asia limited prompt vessel availability, preventing sharper corrections.

Another shipbroker said, “Demand remains soft in the Pacific, but hire rates are slightly firmer due to vessel delays caused by adverse weather.”

The broader dry bulk market showed mixed momentum during the week. Capesize and Handysize segments softened slightly amid slower activity, while Panamax and Supramax witnessed marginal improvement backed by selective cargo demand and vessel availability dynamics.

Route-wise update

Market highlights

- Baltic Dry Index (BDI) rises w-o-w: The BDI increased by 9.8% (260 points) w-o-w to 2,910 as of 9 July, compared with 2,650 a week earlier, supported by improved dry bulk market sentiment. The Panamax index rose by 2.6% (58 points) w-o-w to 2,253, driven by firm Atlantic demand and tighter vessel availability, although sufficient Pacific tonnage restricted further gains. Meanwhile, the Supramax index gained 1.5% (25 points) w-o-w to 1,700, supported by firmer Atlantic activity, vessel delays, and selective Indonesia–India enquiries despite subdued Pacific cargo demand.

- Brent crude futures rise w-o-w: Brent crude oil (September 2026 contract) stood at $76.65/barrel (bbl) on 10 July, up $4.91/bbl w-o-w from $71.74/bbl a week earlier, supported by renewed supply concerns and stronger market sentiment amid uncertainty around global crude availability.

- Bunker prices decline w-o-w: Bunker prices edged lower by $9/tonne (t) w-o-w to $652/t as of 10 July, compared with $661/t a week earlier, amid softer fuel oil values and easing energy market sentiment. Lower geopolitical risk premiums and cautious demand trends contributed to the decline.

- DCE coke futures decline w-o-w: Coke futures on the Dalian Commodity Exchange for the September 2026 contract fell to RMB 1,913/t ($281.62/t) as of 10 July, compared with RMB 1,938/t ($285.46/t) in the previous week. The decline reflected cautious sentiment amid subdued steel demand, weak coke fundamentals, and uncertainty over China’s steel production outlook.

Outlook

Coal freight rates to India are expected to remain range-bound in the near term, with fresh cargo enquiries and tonnage availability likely to determine market direction. Panamax sentiment may remain supported by steady fixture activity, although ample Pacific vessel supply could cap significant gains.

Meanwhile, Supramax movement is expected to track Indonesia-India cargo demand. Weather-related disruptions may provide short-term support by tightening vessel availability, while slower coal activity could keep sentiment cautious.

Leave a Reply