- West African demand and vessel enquiries support bulk freight

- Container bookings slow as carriers adjust capacity, route availability

India’s rice freight market witnessed a firmer trend in the week ended 8 July 2026, driven by steady African demand, tightening container availability and operational challenges across key routes. Breakbulk freight sentiment strengthened as restricted carrier bookings encouraged exporters to explore bulk shipments, while the container market remained mixed amid changing vessel availability and routing constraints.

West Africa supports breakbulk movement

West African demand remained firm, with steady cargo enquiries and continued shipment activity towards key destinations including Benin, Ivory Coast and Guinea. Limited container availability further accelerated the shift towards breakbulk shipments as exporters looked for alternative shipping options.

A shipbroker told BigMint, “Mainline container operators have restricted bookings on certain routes, leaving exporters with limited options and shifting some cargo movement towards breakbulk vessels.”

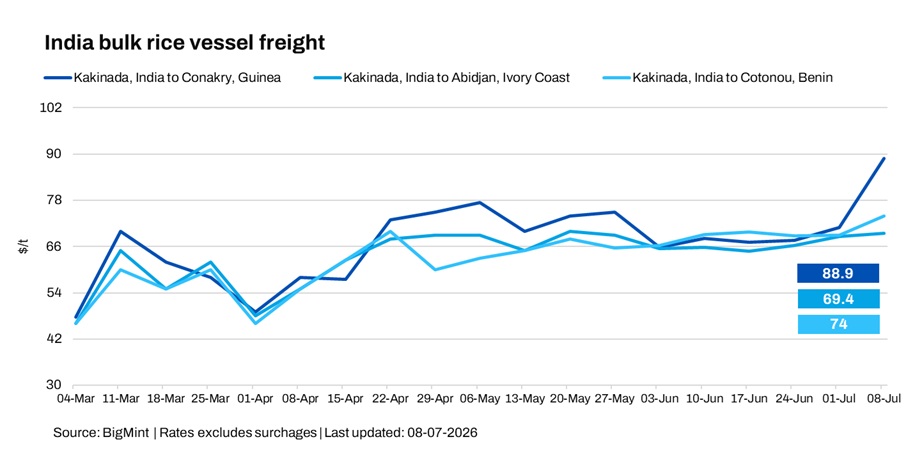

Another source shared with BigMint, “West African breakbulk freight levels remain elevated amid increased dependency on bulk shipments. Freight indications towards Conakry are being heard at around $90-100/t, while Cotonou and Abidjan routes are indicated at $75-85/t.”

Route-wise update

Container market mixed amid booking constraints

Container freight witnessed mixed sentiment during the week. Regular East African shipments continued, although limited carrier space, booking restrictions and vessel deployment adjustments kept the market cautious.

A rice trader said, “The East African market is witnessing firmer freight levels amid steady cargo movement. Demand from destinations like Mombasa remains healthy, supporting vessel enquiries.”

Meanwhile, a shipbroker noted, “Container freight movement has slowed as bookings for this month have largely been suspended. Fresh updates are expected after 10-15 July’26, while exporters continue to evaluate breakbulk options amid limited container availability.”

Weather and logistics challenges remain key focus

Seasonal monsoon conditions continued to affect cargo operations at Indian ports, leading to slower handling and scheduling challenges. Alongside weather-related disruptions, vessel repositioning issues and route limitations continued to influence freight sentiment.

Despite these challenges, Africa-bound cargo movement remained active, with steady enquiries supporting vessel demand.

“Breakbulk shipments from India to African destinations continue to remain active, with regular loadings underway for Mombasa, Tamatave and Berbera. Fresh shipments are also being planned towards Benin. Major export destinations currently include Tamatave, Maputo, Durban, Mombasa, Dar-es-Salam, Congo and Cotonou,” a shipbroker said.

Non-basmati rice export prices rise 1.5% w-o-w

BigMint’s assessment for Non-Basmati Parboiled Rice FOB Kakinada increased by $5/t w-o-w to $343/t as on 8 July 2026, compared with $338/t in the previous week. The rise was supported by steady buying interest from African markets and firmer freight sentiment amid ongoing shipment activity.

Outlook

Rice freight sentiment is expected to remain firm in the near term, particularly on Africa-bound routes, supported by container booking limitations and steady cargo enquiries. Market participants will closely track carrier updates after mid-July, along with monsoon-related disruptions, vessel availability and changes in global freight conditions.

Leave a Reply