- Weak construction demand limits scrap buying

- Need-based procurement keeps trading activity slow

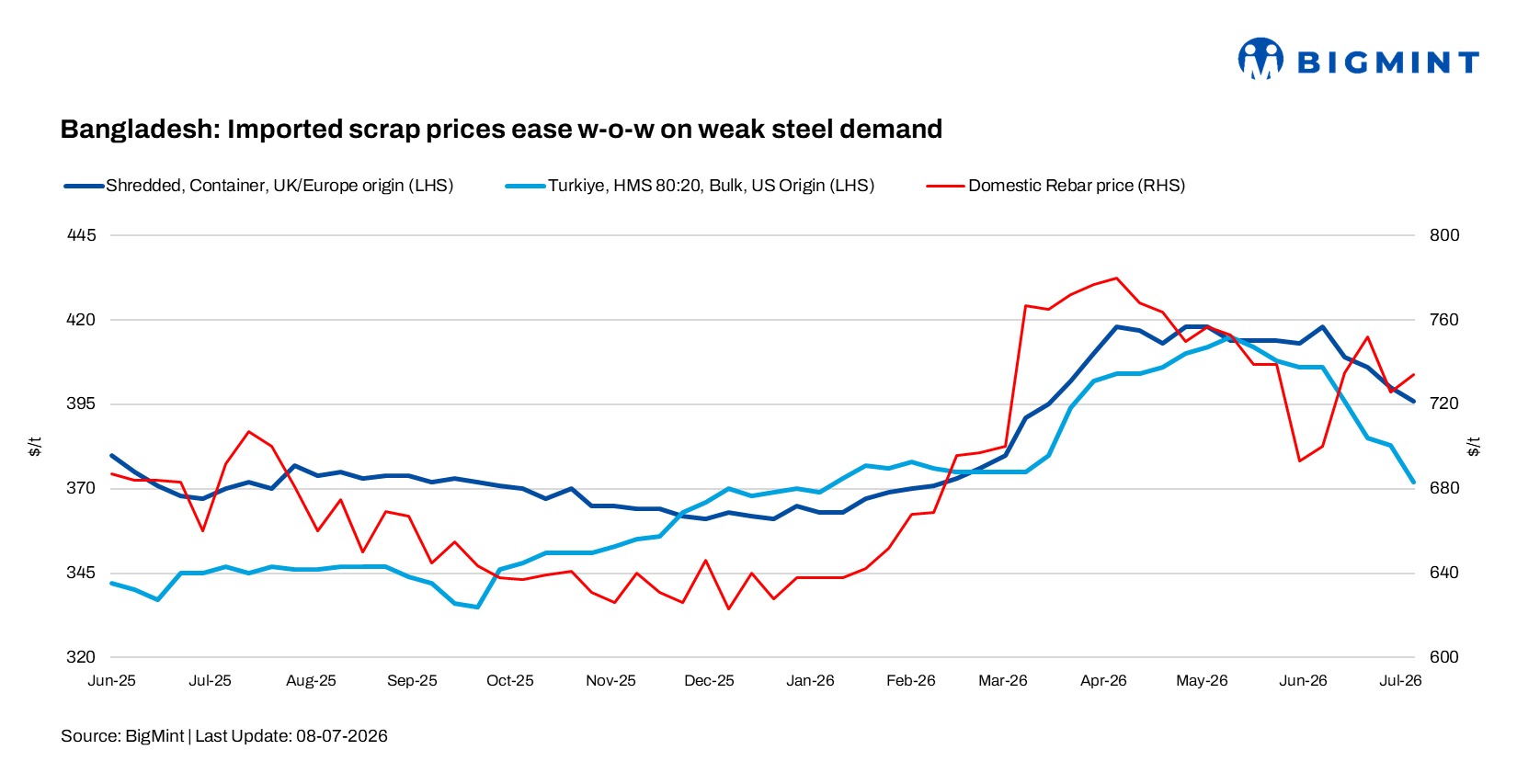

Bangladesh’s imported ferrous scrap market remained subdued during the week ended 8 July as monsoon-related disruptions continued to weigh on construction activity and finished steel demand. Mills limited purchases to immediate requirements, while wide bid-offer gaps restricted fresh import bookings.

Buying activity remained extremely weak as heavy rainfall continued to disrupt construction work across the country. Market participants described trading conditions as “very dull,” with mills making only selective, need-based inquiries for imported scrap.

BigMint’s weekly assessments, CFR Chattogram

- European-origin containerised HMS (80:20): $363/t, down $3/t w-o-w

- European-origin containerised shredded: $396/t, down by $4/t w-o-w

- Japanese-origin bulk H2: $384/t, down by $5/t w-o-w

- US-origin bulk HMS (80:20): $391/t, down by $4/t w-o-w

Market updates

Latin America-origin HMS 90:10 was offered at $385/t CFR against buyers’ bids of $370/t CFR. UK-origin HMS was available at $375/t CFR, while buyers targeted $365/t CFR. Philippines-origin GI bundles were offered at $340/t CFR, down from $345/t CFR previously, reflecting continued pressure on containerised scrap prices.

Buyers maintained bids at $355-356/t CFR for HMS and $385-390/t CFR for shredded scrap, while suppliers sought around $365/t CFR for HMS and above $400/t CFR for shredded. The wide gap between bids and offers prevented most transactions.

Despite subdued buying sentiment, BigMint captured two shredded scrap cargoes totalling 2,000 t during the week. One 1,000 t Australia-origin cargo was concluded at $390/t CFR Chattogram, while another 1,000 t UK-origin cargo was booked at $400/t CFR Chattogram.

Market participants said suppliers initially offered shredded scrap at $395-400/t CFR, while HMS offers were heard around $370/t CFR. However, buyers remained cautious amid weak downstream steel demand, rising electricity tariffs, higher production costs, and intermittent power shortages, limiting buying interest to need-based procurement.

A Dhaka-based participant said, “Mills were trying to raise finished steel prices to offset higher production costs, but weak demand continued to limit their pricing power.” Larger integrated producers are expected to manage the current market better, while small and mid-sized rerolling mills are likely to face greater pressure if demand remains weak.

The domestic steel market also remained sluggish. Local scrap prices were heard at BDT 52,000-53,000/t ($422-430/t), while billet indicative levels were heard at around BDT 70,000/t ($568/t). Rebar offers were reported at approximately BDT 90,000-92,000/t ($730-746/t) exw-Chattogram and BDT 85,000-86,000/t ($690-698/t) exw-Dhaka, although actual trading remained limited due to weak construction activity and subdued finished steel demand.

Production costs have also increased following higher electricity tariffs and the implementation of revised VAT and tax measures from July. Market participants estimate that electricity tariff revisions have added around BDT 2,000/t ($16/t) to steelmaking costs, while VAT and other tax changes have increased finished steel production costs by about BDT 4,000/t ($32/t).

At the same time, intermittent power shortages continue to affect rerolling and induction furnace mills, further discouraging scrap purchases.

Outlook

BigMint expects Bangladesh’s imported scrap market to remain under pressure in the coming week. Mills are likely to continue with need-based procurement until demand for finished steel improves. Rising production costs, power supply issues, and cautious buying sentiment are expected to keep scrap demand weak, particularly among small and medium-sized steelmakers.

Leave a Reply