- South and west India record sharpest price corrections

- Lower domestic scrap prices keep imports uncompetitive

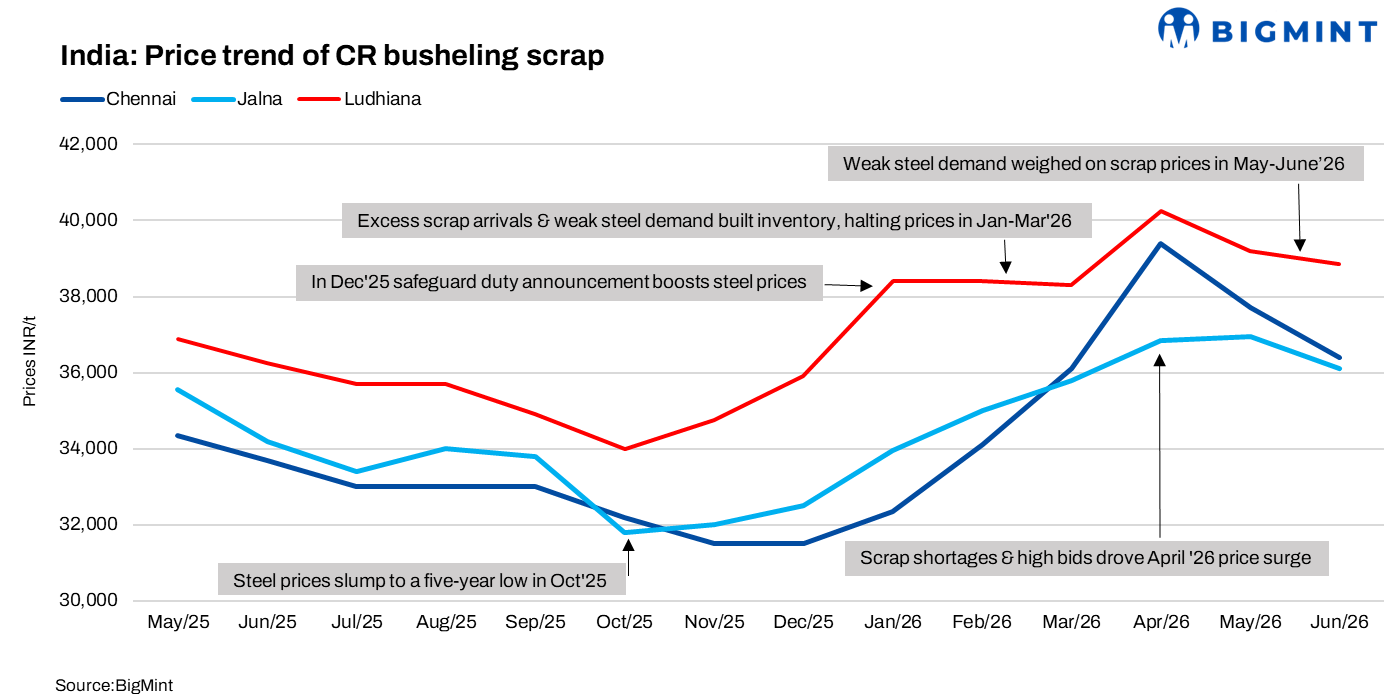

India’s CR busheling scrap market softened in June 2026 versus May, with the steepest declines recorded in the south and west, according to BigMint’s analysis. Prices in those regions fell by INR 1,300-1,600/t m-o-m as weak secondary steel demand, modest corrections in finished steel prices, and inventory pressure curtailed scrap buying.

Northern India saw milder falls of around INR 300-500/t; tight supply and moderate demand from foundries and local scrap-based mills limited downside in prices. Overall, OEM scrap trends broadly reflected a muted sentiment across the secondary steel sector.

CR busheling auction comparison m-o-m

Indian OEM scrap auctions saw m-o-m price corrections of roughly INR 500-1,500/t in June. The downturn was most pronounced in the west and south: Ahmedabad and Hosur led losses, plunging about 4%, while Pune fell roughly 3%. Major automotive hub Pantnagar recorded a smaller decline of around 1%. In contrast, Gurugram bucked the trend with a modest gain of about 3%.

HRC, CRC price trends

At the trade level, HRC prices edged down by INR 200/t m-o-m to INR 58,300/t in June from INR 58,500/t in May, while CRC prices remained stable at INR 65,200/t over the same period. The marginal decline in HRC prices was mainly attributed to weak market demand and procurement driven largely by immediate requirements.

Imported vs domestic scrap

Imported CR busheling scrap at Kandla and Mundra was priced at $410/t (approximately INR 41,200-41,400/t DAP after duties). In contrast, the average local busheling scrap price in Ahmedabad-Gujarat stood at INR 35,900/t DAP. As a result of cheaper domestic availability, there were no significant trades reported in June 2026.

Auto sector performance

The Indian passenger vehicle market showed strong y-o-y growth in June but corrected m-o-m, falling 11.1% to 3,91,900 units from 4,40,808 in May; several OEMs posted robust annual gains even as competition among the top four intensified. Maruti Suzuki remained the market leader, reporting a 23.8% y-o-y rise (to 1,18,906 units in June 2026 versus June 2025) but saw its market share slip 0.6 percentage points to 37.6% and experienced a sharp 22.7% m-o-m drop from 1,90,337 units in May, which weighed on the industry’s monthly numbers. Tata Motors delivered one of the strongest monthly performances with 62,076 units, retaining second place and expanding its presence, underscoring resilient annual demand amid short‑term volatility.

Upcoming scrap auctions

Outlook

Domestic CR busheling scrap prices are expected to remain under pressure in July as secondary steel demand stays subdued and buyers continue need-based procurement, although limited scrap availability in northern India may restrict sharper declines.

Leave a Reply