- China slowdown drags Asian coal prices

- Weak demand pressures regional coal market

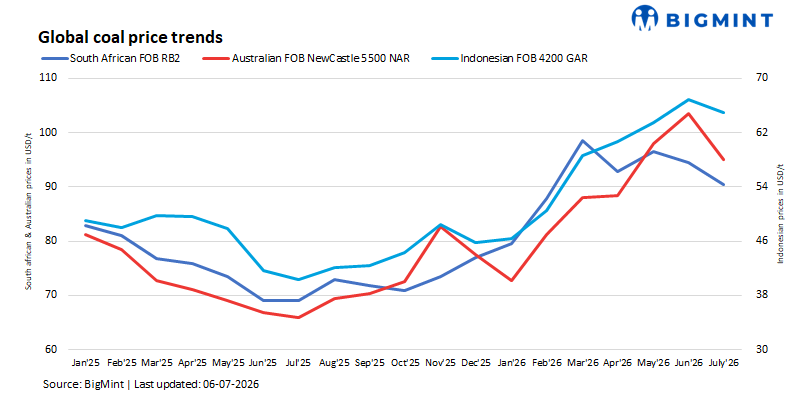

Asian thermal coal markets entered a decisive correction during the week ended 3 July as weakening Chinese demand removed the principal source of support for regional prices. What began as a gradual softening in China’s domestic market has spread across the Asian seaborne market, pulling down Australian Newcastle prices, Indonesian FOB values and imported coal assessments into India.

The market has undergone a marked shift from the conditions prevailing during May and early June, when supply concerns, Indonesian export uncertainty and seasonal demand underpinned prices. Comfortable utility inventories across Asia, weaker industrial activity, abundant domestic coal availability in both China and India, and the onset of the Indian monsoon have collectively reduced procurement activity, leaving buyers in no urgency to secure additional cargoes.

China leads the regional correction

China’s domestic thermal coal market has weakened rapidly over the past two weeks, removing the strongest source of support for regional prices. Concerns surrounding mine inspections, supply disruptions and Indonesian export availability have largely faded, giving way to a market characterised by rising inventories and slowing consumption.

Utilities remain comfortably stocked, inventories at northern ports continue to increase, South China terminals are operating close to capacity and imported cargoes are increasingly facing discharge delays. Heavy rainfall has boosted hydroelectric generation, reducing coal burn, while industrial consumers, including cement plants and chemical producers, have largely restricted purchases to immediate requirements.

Mine-mouth prices have fallen by RMB 5-20/t across several producing regions as traders report increasingly cautious downstream buying. Coastal freight has weakened even more sharply. Freight rates from Qinhuangdao to Shanghai have more than halved, falling from $7.09/t in mid-June to just $3.12/t in early July, indicating a pronounced slowdown in domestic coastal coal movements.

Australian export prices retreat

Newcastle thermal coal prices have corrected from the mid-$150s/t only three weeks ago to around $130/t as Chinese buying largely disappeared and other Asian utilities remained adequately supplied. The loss of China’s spot demand has exposed a market where buyers continue to purchase only immediate requirements while sellers have become progressively more willing to negotiate.

Bid-offer spreads widened through late June as buyers repeatedly lowered bids while producers attempted to defend prices using index-linked offers. Those premiums narrowed steadily into early July as physical sellers increasingly accepted prevailing market levels. SGX forward contracts continue to imply further weakness later in the year, reflecting expectations that elevated inventories may persist well into the third quarter.

Indonesian fundamentals soften despite domestic constraints

Domestic Market Obligation (DMO) requirements and increased deliveries to PLN continue to divert portions of Indonesia’s medium-calorific coal into the domestic market, with several producers reporting that much of their 5,000 GAR production is now committed locally following recent power shortages.

Those supply constraints, however, are no longer sufficient to offset weakening regional demand. Chinese buyers continue negotiating aggressively, trader-held cargoes purchased at higher prices are increasingly being discounted, and expectations that additional RKAB production quotas could be approved during the second half are weighing on market sentiment. Consequently, FOB prices have continued declining across almost every Indonesian coal grade despite comparatively tighter domestic fundamentals.

Indian imports remain subdued

The southwest monsoon, together with exceptionally comfortable domestic coal availability, has substantially reduced India’s discretionary import demand. Coal India continues offering large auction volumes while pithead inventories remain healthy, allowing utilities to rely predominantly on domestic coal. Imported purchases have therefore remained largely confined to blending requirements and plants specifically configured to consume imported fuel.

Portside prices for Indonesian and South African coal have continued to soften as buyers postpone purchases in anticipation of further declines. Sponge iron producers remain cautious amid weak steel demand, while cement producers have increasingly switched towards petroleum coke after international petcoke prices corrected by more than $20/t from their May highs. US Northern Appalachian coal has remained comparatively resilient, supported by steady demand from premium cement producers, although procurement by larger industrial consumers has also remained measured.

India has consequently become a largely price-responsive importer rather than an active driver of regional coal demand, removing another important source of support for seaborne prices.

Freight reflects weaker cargo demand

Shipping rates from East Kalimantan to western India continued easing as Indonesian export enquiries slowed, while Richards Bay routes also softened amid fewer cargo fixtures. Australian routes remained comparatively firm, although largely because of vessel availability rather than stronger coal demand. Lower bunker fuel prices have reduced delivered freight costs, but the decline has failed to stimulate additional buying, reinforcing the cautious procurement strategy adopted across the region.

Outlook

China has shifted from supporting Asian thermal coal prices to leading their correction, and that weakness is now being transmitted across Australia, Indonesia and India through lower procurement, weaker freight activity and softer seaborne benchmarks. Utilities across the region remain comfortably stocked, industrial demand continues to underperform expectations, and buyers are increasingly delaying purchases in anticipation of further price declines.

Unless sustained summer heat materially increases electricity demand across North Asia or fresh supply disruptions emerge, the combination of comfortable inventories, subdued industrial activity, expectations of higher Indonesian export availability and weak Indian import demand is likely to keep Asian thermal coal prices under pressure through July and potentially much of the third quarter.

Leave a Reply