- Weaker JPY supports export competitiveness

- Vietnamese buyers delay purchases amid bearish outlook

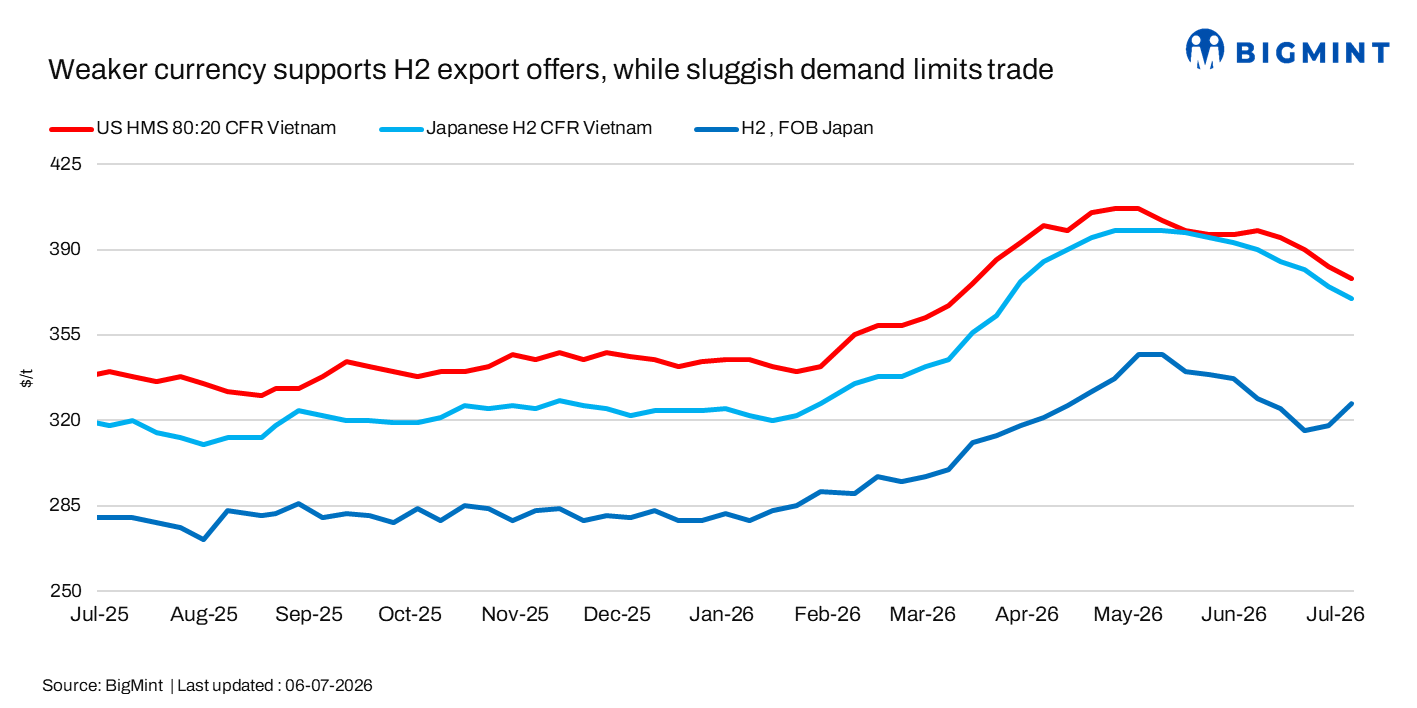

Japan’s H2 ferrous scrap export market remained under pressure during the week ended 6 July despite a weaker JPY, as sluggish demand across Southeast Asia and competitive deep-sea offers continued to weigh on trading activity. While the weaker Japanese currency improved exporters’ competitiveness by increasing JPY-denominated returns, market participants said domestic mill buying remained the key factor influencing export pricing.

Weekly assessments

- Japanese H2 scrap was at $370/t CFR Vietnam, down by $5/t w-o-w.

- Japanese H2 scrap was at JPY 53,000/t ($327/t) FOB Tokyo Bay, up by JPY 1,600/t ($10/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $378/t CFR Vietnam, down by 5/t w-o-w.

Japan market

Japan’s scrap export market remained mixed, as stronger JPY-based FOB prices contrasted with weaker CFR offers to Vietnam. H2 export offers were heard at $370-372/t CFR Vietnam, down from around $375-377/t CFR a week earlier, while buyers maintained bids near $365/t CFR, resulting in a persistent bid-offer gap.

Market participants said the weaker JPY improved exporters’ returns in local currency, but its impact on export pricing remained limited as overseas buyers continued to push for lower prices.

A Japanese market participant said, “The weaker JPY has yet to provide any meaningful boost to exports, as lower purchase prices sought by overseas buyers have largely offset the currency advantage.”

Tokyo Steel lowered H2 buying prices only at its Nagoya yard by JPY 500/t ($3/t) to JPY 53,500/t, indicating cautious procurement.

H2 collection prices were heard at JPY 52,000-53,500/t ($321-330/t) FAS, while FOB Tokyo Bay increased by JPY 16,000/t ($10/t) to JPY 53,000/t ($327/t), supported by exchange-rate movements.

Market participants also noted that Higher-value scrap is largely retained by domestic mills, with exports dominated by lower-grade material.

Vietnam market

Vietnamese buyers maintained a cautious procurement strategy during the week, delaying bookings amid weak finished steel demand and expectations of further price declines. Tradable levels for Japanese H2 were indicated around $365/t CFR, while most mills preferred to wait for additional corrections.

The deep-sea scrap market also weakened, with US and Australian-origin HMS 80:20 offered at around $380/t CFR Vietnam, while buyers targeted $370-375/t CFR.

A market participant said, “Sluggish downstream steel demand and competitive global scrap prices continued to pressure import sentiment, with only limited mills actively seeking deep-sea cargoes”.

Leave a Reply