- Monthly average sponge iron prices decline by INR 500-1,350/t

- Domestic sponge iron trade volumes rise 35% m-o-m on lower prices

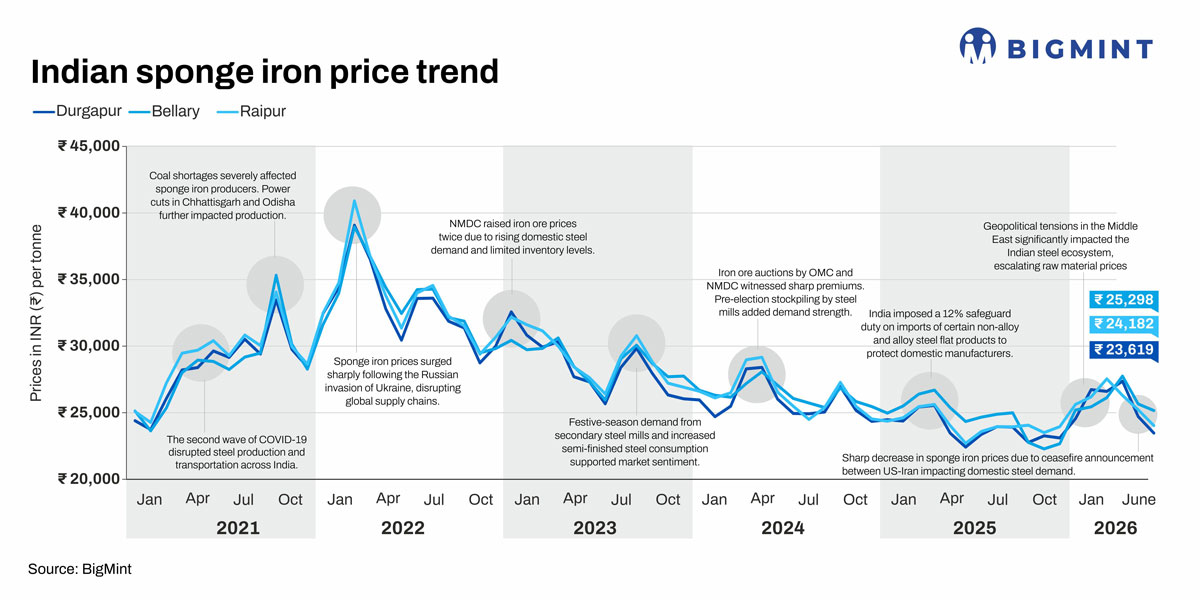

India’s sponge iron market remained under pressure in June 2026, with monthly average prices declining across all key producing regions on weak finished steel demand, cautious procurement, and lower export realisations. The benchmark pellet-based sponge iron (PDRI) prices in Raipur declined by INR 750/t m-o-m to INR 23,900/t exw-Raipur on 1 July, due to weakening demand and significant rise on competition from neighbouring regions.

Iron ore-based sponge iron records sharp correction

Average prices of iron ore lump-based sponge iron fell across all markets in June compared with May. Among the major producing regions, Mandi Gobindgarh registered the sharpest decline, with average prices falling by INR 1,357/t to INR 30,200/t. Rourkela followed, where prices dropped by INR 1,248/t to INR 25,236/t, while in Ramgarh prices declined by INR 1,177/t to INR 25,719/t.

Durgapur recorded a decrease of INR 1,017/t to INR 26,192/t, followed by Raigarh, where prices eased by INR 865/t to INR 25,265/t. Bellary witnessed the smallest correction among the different regions, with prices falling by INR 542/t to INR 26,392/t. The widespread decline indicates limited buying from steelmakers and re-rollers, who restricted purchases to immediate production requirements amid weak finished steel demand.

Major sponge iron producers in Maharashtra sold adequate volumes to nearby markets such as Jalna and Wada. They are also actively exploring new demand centres among induction furnace (IF) steelmakers in Telangana and Gujarat to broaden their market reach and liquidate inventories.

Meanwhile, leading sponge iron manufacturers from eastern India have continued supplying material to Maharashtra and Punjab through rakes. The sustained inflow of sponge iron into these scrap-based regions reflects healthy demand from induction furnace producers, who continue to prefer high-grade, consistent-quality sponge iron from major integrated mills to optimise metallic charge and improve production efficiency.

Pellet-based sponge iron follows similar trend

The pellet-based sponge iron segment mirrored the broader market trend. Ramgarh posted the steepest correction, with prices declining by INR 1,355/t to INR 23,496/t, followed by Durgapur, where prices fell by INR 1,233/t to INR 23,619/t. Raipur, India’s largest pellet-based sponge iron hub, recorded a decline of INR 1,175/t to INR 24,182/t. Raigarh and Jharsuguda witnessed corrections of INR 936/t and INR 902/t, respectively, while Hyderabad, Chennai, and Bellary recorded relatively smaller declines of INR 504-527/t.

Export DRI prices soften on weak regional demand

Export offers also came under pressure during June as buying interest from neighbouring countries remained subdued. DRI export prices to Nepal (CPT Raxaul) declined by $16/t m-o-m to $305/t, while offers to Bangladesh (CPT Benapole) fell by $18/t to $311/t. Softer international demand and competitive regional supply continued to pressure Indian export offers during the month. Lower prices stimulate higher trade

Lower prices stimulate higher trade

Despite the decline in prices, domestic market activity improved during June. Domestic sponge iron trade volumes increased to 322,996 t from 239,551 t in May, representing an increase of 83,445 t, or nearly 35% m-o-m. Similarly, DRI exports rose to 26,500 t from 23,500 t in May, registering a gain of 3,000 t (around 13% m-o-m). The increase suggests that lower prices encouraged selective procurement and improved export competitiveness, although overall demand remained below historical averages.

Capacity utilisation remains below optimal levels

Although production costs have eased with lower coal prices and improved domestic coal availability, sponge iron producers have not significantly increased operating levels due to insufficient downstream demand. Many producers continued to operate kilns intermittently or at reduced loads to avoid inventory accumulation.

Based on prevailing market conditions across major producing clusters, capacity utilisation during June is estimated to have remained around 70-80% for merchant coal-based sponge iron units, with considerable variation by region. Integrated steel producers generally operated at relatively higher utilisation levels because of captive billet consumption, while standalone merchant producers adjusted production as per order inflows and profitability.

Comparative analysis: May vs June

The June market demonstrated a correction cycle due to weak downstream steel demand rather than supply disruptions. Lower billet and finished steel prices reduced procurement appetite across sponge iron-consuming segments, forcing producers to gradually lower their offers throughout the month.

However, unlike periods of severe market weakness, the decline in prices translated into improved physical trade. Domestic buyers responded positively to more attractive and lower price levels, resulting in a substantial increase in transaction volumes. This indicates that the market remained fundamentally active, with buyers postponing purchases until prices reached acceptable levels rather than withdrawing completely.

Regional price corrections also highlighted differing market dynamics, northern and eastern markets, particularly Mandi Gobindgarh, Rourkela, Ramgarh, and Durgapur, experienced steeper declines due to weaker local steel demand and slower procurement. In contrast, Bellary, Hyderabad, and Chennai registered relatively modest corrections, supported by more balanced regional demand and supply conditions.

The export market presented a similar picture. Although Indian DRI suppliers reduced offers to Nepal and Bangladesh to remain competitive, export volumes still increased modestly, suggesting that lower prices helped revive slight buying interest despite a challenging regional demand environment.

Outlook for July

Producers adjusted offers and production levels in response to softer steel demand, while buyers gradually re-entered the market as prices became more attractive in June. The simultaneous decline in prices and increase in trade volumes suggests improving market acceptance at lower price levels, which could help stabilise trading activity if downstream steel demand strengthens in July.

Leave a Reply