- China, Asia cushion global alumina output decline

- Regional production shifts reshape global alumina supply

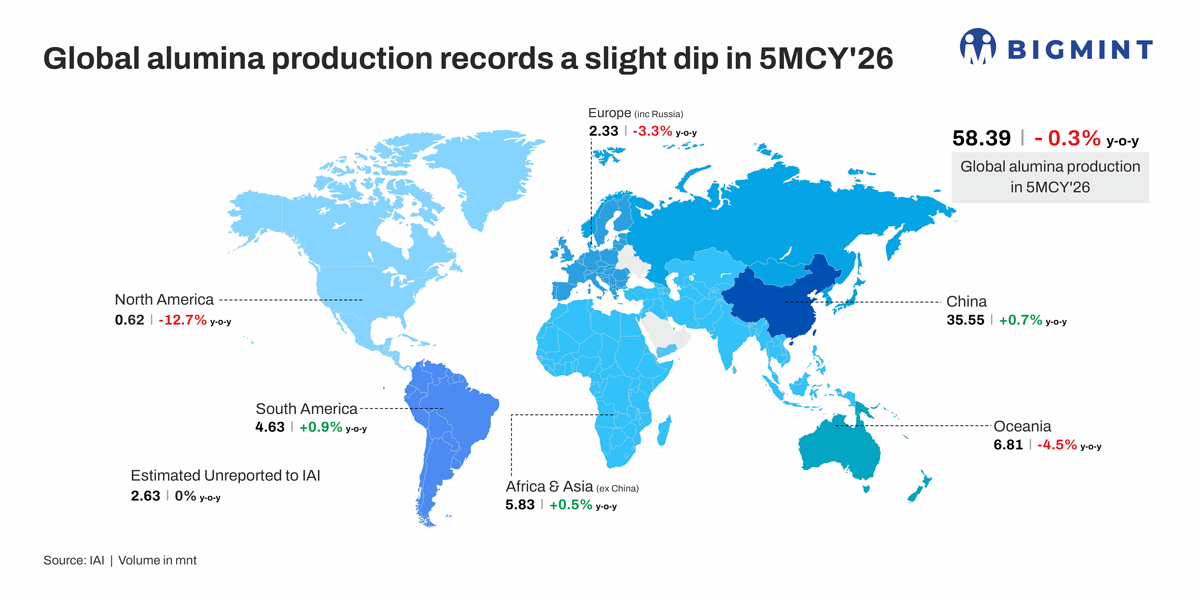

Global alumina production declined marginally by 0.3% y-o-y to 58.39 million tonnes (mnt) during January-May 2026 (5MCY’26) from 58.56 mnt in the corresponding period last year, according to the International Aluminium Institute (IAI). The slight decline reflected mixed regional production trends, with higher output in Asia and South America partially offsetting weaker production across North America, Europe, and Oceania.

Regional drivers shaping global metallurgical alumina output

China, the world’s largest alumina producer, recorded an estimated 35.55 mnt, up 0.7% y-o-y from 35.29 mnt. Production remained supported by stable refinery utilisation, adequate bauxite availability, and the ramp-up of newly commissioned refining capacity. However, output growth was moderated by scheduled maintenance and environmental-related shutdowns across key producing provinces such as Henan, Guangxi, and Guizhou, although the country continued expanding long-term refining capacity.

Production in Africa & Asia (excluding China) increased by 0.5% y-o-y to 5.83 mnt, supported by higher refinery operating rates, refinery expansions in India and Indonesia, and improved bauxite availability. Indonesia’s PT Bintan Alumina Indonesia continued to contribute to regional growth through ongoing capacity ramp-ups, while downstream aluminium investments across Southeast Asia also supported production.

South America registered a 0.9% y-o-y increase to 4.63 mnt, mainly driven by stable operations at Hydro’s Alunorte refinery in Brazil, supported by adequate bauxite supply and improved operational reliability. However, infrastructure constraints and elevated power costs continued to affect Brazilian operations, including Albras and Alupar, limiting stronger production growth.

Conversely, North America recorded the steepest decline among major producing regions, with output falling 12.7% y-o-y to 0.62 mnt. Production remained under pressure from lower refinery utilisation, planned maintenance, elevated labour and energy costs, structural supply constraints, and weaker refining margins, despite operational improvements at the Gramercy refinery.

Europe (including Russia) saw production decline 3.3% y-o-y to 2.33 mnt, as elevated gas and electricity costs, maintenance shutdowns, and operational disruptions continued to weigh on refinery economics. Several European and Russian producers also undertook scheduled maintenance and anode-change programmes during the period.

Meanwhile, Oceania recorded a 4.5% y-o-y decline to 6.81 mnt, reflecting planned maintenance at Australian refineries, weather-related disruptions, ageing refinery infrastructure, and higher operating costs. Production was also impacted by the gradual closure of Alcoa’s Kwinana refinery

Outlook

Global alumina production is expected to remain broadly stable over the coming months, with China continuing to drive global output through high refinery utilisation and incremental capacity additions, while India and Indonesia are likely to contribute further growth as new refining projects ramp up. Steady downstream aluminium demand and adequate bauxite availability should provide additional support to production levels.

However, the pace of growth may remain limited due to scheduled refinery maintenance, elevated energy and labour costs, weather-related disruptions, and logistical challenges across several regions. Europe and Oceania are expected to face continued pressure from weak refinery economics, while North American output may recover only gradually. Overall, the global alumina market is likely to remain adequately supplied, although regional supply disruptions and cost pressures could keep market conditions volatile in the near term.

Leave a Reply