- BDI falls for 6th straight session, hits lowest level since mid-Apr

- Subdued iron ore trade, ample vessel availability weigh on index

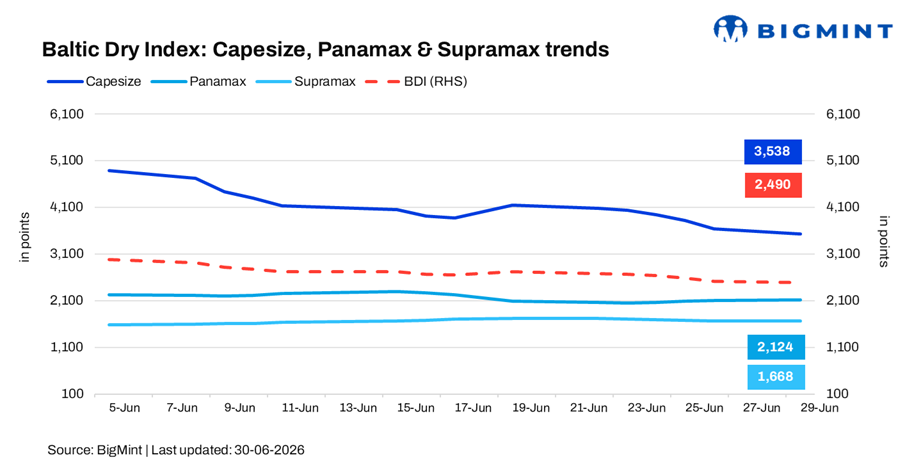

The Baltic Exchange’s Dry Bulk Index (BDI) declined by 1.4% (34 points) to 2,490 points on 29 June 2026 against 26 June, marking its sixth consecutive daily decline and the lowest level since 15 April.

The decline was largely attributed to persistent weakness in the Capesize segment, as subdued iron ore trade and ample vessel availability weighed on earnings. Meanwhile, Panamax rates remained supported by healthy grain and coal cargo demand, particularly from the Atlantic basin, helping offset some of the broader market weakness.

Segment-wise performance

- Capesize: The Capesize index fell sharply by 2.8% (102 points) to 3,538 points, extending losses amid softer iron ore and coal cargo enquiries, particularly in the Pacific basin. Increased vessel availability and cautious chartering activity continued to pressure spot freight rates.

- Panamax: The Panamax index rose 0.7% (14 points) to 2,124 points, supported by steady grain exports from South America and sustained coal shipments. Healthy cargo volumes helped offset broader market weakness and kept chartering sentiment relatively firm.

- Supramax: The Supramax index edged down 0.1% (2 points) to 1,668 points, reaching its lowest level since 15 June. Sentiment remained subdued amid limited minor bulk cargo enquiries and ample vessel availability across Asian trading routes.

Outlook

The Baltic Dry Index is expected to remain under pressure in the near term, with continued weakness in the Capesize segment likely to outweigh the resilience in Panamax. However, any pickup in iron ore shipments from Australia and Brazil, along with firmer Chinese import demand, could help stabilise overall dry bulk freight rates.

Leave a Reply