- Retail NAPP demand weakened during the monsoon

- Port inventories remained comfortable across Kandla and Tuna

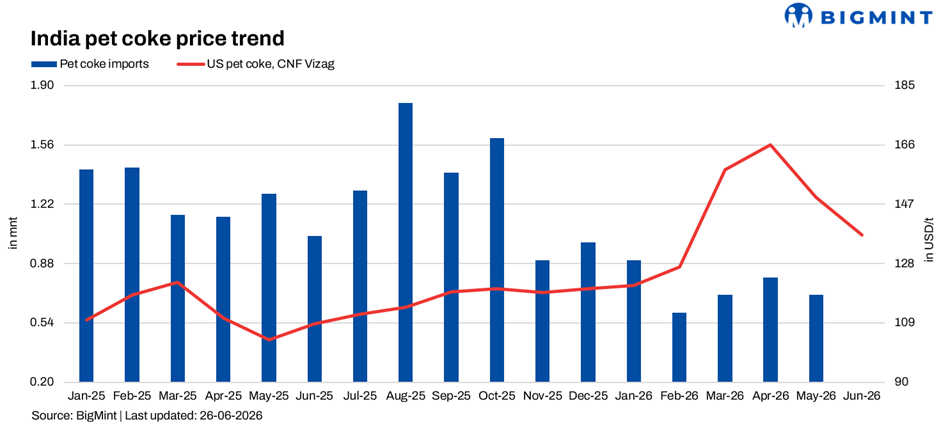

The global fuel-grade petroleum coke market has entered a new phase after several months of elevated prices. A broad correction in June has lowered delivered costs into India, restoring petcoke’s competitiveness against US Northern Appalachian (NAPP) thermal coal and prompting Indian cement manufacturers to rebalance their fuel mix.

While India’s cement production continues to grow strongly, the onset of the monsoon has reduced immediate fuel demand. Comfortable inventories across both petcoke and imported coal have shifted purchasing decisions increasingly towards economics rather than supply security.

US NAPP coal continues to enjoy healthy industrial demand in India, but the retail market has softened as cement producers increasingly favour cheaper petcoke.

Global Fuel-Grade Petroleum Coke Prices Continue to Correct

The seaborne petcoke market continued to weaken during June as buying interest remained subdued across major importing regions. Ample availability from US Gulf Coast refiners, together with softer demand from cement producers, has pushed prices steadily lower.

Global Fuel-Grade Petroleum Coke Price Snapshot

Fuel-grade petcoke prices continued to soften across major markets during the past month. FOB US Gulf Coast 6.5% sulphur prices declined by $6/t to $75.5/t from $81.5/t, while 4.5% sulphur material fell by $5/t to $81/t. In India, CFR west coast 6.5% sulphur prices eased by $1.5/t to $134.5/t, while 8.5% sulphur material declined by $1.5/t to $134/t. In China, both 6.5% and 8.5% sulphur petcoke prices fell by $3.5/t, to $132.5/t and $137.5/t, respectively, reflecting softer buying interest across key importing markets.

Although delivered Indian prices have declined less sharply than FOB US Gulf Coast values because of freight costs, the reduction has been sufficient to materially improve petcoke’s economics for Indian cement producers.

Current landed costs are estimated around $150/t, equivalent to approximately INR 1.93/Mcal, representing one of the most competitive fuel options currently available to the cement sector.

Indian Cement Industry Continues to Expand

The softer fuel market comes despite robust underlying cement demand.

Indian cement production increased by approximately 8.3% year-on-year during April-May 2026 to around 83 million tonnes, while May production alone rose to approximately 42 million tonnes.

Demand remains supported by infrastructure construction, housing activity and industrial investment. However, the arrival of the southwest monsoon has slowed construction activity across several regions, resulting in a seasonal moderation in cement dispatches.

This has encouraged producers to focus on reducing fuel costs while maintaining operating margins.

Petcoke Regains Its Competitive Advantage

The latest price correction marks an important reversal from conditions seen earlier this year.

During April and early May, elevated petcoke prices encouraged many cement manufacturers to increase purchases of imported US NAPP coal. At that time, the energy-adjusted cost of NAPP coal compared favourably with petcoke.

The recent decline in petcoke prices has reversed that relationship.

Many cement plants are once again increasing petcoke consumption because it now offers a lower energy cost than imported thermal coal while also delivering operational benefits in kiln performance.

Market participants report that several buyers who had switched to US thermal coal are now returning to petcoke for incremental purchases.

US NAPP Coal Continues to Find Industrial Demand

Despite the renewed competition from petcoke, India remains one of the world’s largest destinations for US thermal coal.

Industrial consumers—including cement manufacturers, captive power plants and other energy-intensive industries—continue to import significant volumes of high-calorific-value US NAPP coal.

Numerous cargoes are scheduled to arrive during June and July for major industrial consumers including Ultratech Cement, Ramco Cement, Bharathi Cement, Tata Steel, Wonder Cement, JSW-Dalmia and other industrial users.

These buyers continue to value NAPP coal for its high calorific value, low ash content and stable combustion characteristics.

Retail NAPP Coal Market Weakens

The retail market presents a noticeably different picture.

Portside trading activity has slowed during June as buyers delay purchases while evaluating the improving economics of petcoke.

Retail NAPP prices have eased from around INR 14,000-14,500/t earlier this month to approximately INR 13,300-13,600/t.

Recent trades have been concluded around INR 13,400-13,600/t, while offers continue to soften as suppliers compete for limited spot demand.

Weekly lifting has also moderated.

Retail dispatches declined from approximately 129,000 tonnes during Week 24 to around 93,000 tonnes during Week 25, while port inventories remain comfortable at roughly 313,000 tonnes across Kandla and Tuna ports.

Comfortable inventories have reduced urgency among buyers and increased competition among suppliers.

Fuel Competition Becomes the Dominant Market Driver

The interaction between petcoke and US NAPP coal has become the defining feature of India’s imported fuel market.

Earlier this year, high petcoke prices encouraged widespread substitution towards imported thermal coal.

Today, falling petcoke prices are encouraging the reverse.

Rather than reflecting any deterioration in US coal fundamentals, the slowdown in NAPP demand primarily reflects changing fuel economics.

This is particularly evident in the cement industry, where fuel flexibility allows producers to optimise procurement according to relative energy costs.

Current market conditions therefore favour increased petcoke consumption while limiting additional demand for imported thermal coal.

Retail Market Remains Well Supplied

Another notable feature of the market is the comfortable availability of imported US coal within India’s retail supply chain.

Port inventories remain healthy despite continued weekly dispatches, suggesting that import programmes earlier in the year successfully replenished stocks.

Most traders report that customers are purchasing only immediate requirements, with little evidence of speculative buying ahead of the monsoon.

The brick kiln sector has also entered its seasonal slowdown, further reducing spot demand for imported coal.

Outlook

The Indian cement fuel market appears to have entered another transition phase.

Petcoke has regained a meaningful cost advantage after its recent price correction and is likely to remain the preferred fuel while prices remain near current levels.

US NAPP coal is expected to continue serving large industrial consumers requiring premium-quality fuel, but retail demand is likely to remain subdued through the monsoon unless either petcoke prices recover or imported coal becomes materially cheaper.

The coming quarter will therefore be shaped less by supply availability and more by the evolving economics between these two competing fuels. For India’s cement producers, fuel optimisation has once again become the principal procurement strategy.

Leave a Reply