- Bunker prices and DCE futures remain supportive

- Major Australian miners are actively booking

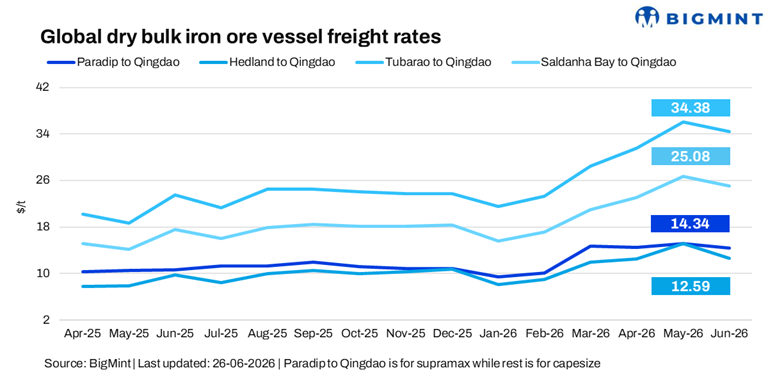

Dry bulk iron ore freight sentiment remained mixed w-o-w on 26 June, with Capesize routes showing divergent trends across the Atlantic and Pacific, while Supramax rates strengthened on improved regional cargo demand and steady export activity from India’s east coast.

Supramax market remained supported by firmer iron ore export enquiries from India and steady vessel demand, reflecting resilient regional trade despite the broader weakness in the dry bulk market. Capesize sentiment remained mixed, with strong cargo activity from Australia and Brazil offset by subdued export demand from South Africa.

A shipbroker stated, “Freight sentiment remained bearish, with Capesize and Supramax rates softening on weak cargo demand and subdued chartering activity. Panamax appeared to be stabilizing on steady grain and coal shipments, while Handymax remained largely unchanged.”

Route-wise update

Factors influencing freight rates

- Baltic Dry Index (BDI) declined w-o-w: The BDI fell 2.3% (62 points) w-o-w to 2,591 on 25 June, weighed down by continued weakness in the Capesize segment. The Capesize index declined 1.2% (50 points) to 3,827, amid softer iron ore cargo demand and subdued chartering activity. Meanwhile, the Supramax index slipped 1.5% (27 points) to 1,678, reflecting weaker minor bulk cargo demand and limited fresh fixtures across key trading regions.

- Bunker prices surge w-o-w: Bunker prices surged by $46/tonne (t) w-o-w to $713/t as of 26 June, supported by a rebound in marine fuel demand and higher refining margins following the stabilization of crude markets after the Middle East ceasefire.

- Brent crude futures decline w-o-w: Brent crude oil (August 2026 contract) was assessed at $72.78/barrel (bbl) on 26 June, down $7.12/bbl w-o-w, as easing geopolitical tensions in the Middle East and the resumption of oil shipments through the Strait of Hormuz reduced the geopolitical risk premium.

- DCE iron ore futures remained largely stable w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) remained largely unchanged at RMB 748/t ($110/t) on 26 June, as cautious optimism over China’s infrastructure-led steel demand offset pressure from elevated port inventories and subdued property-sector activity.

Outlook

Dry bulk iron ore freight rates are expected to remain under pressure in the near term, as cautious chartering activity and softer Capesize demand continue to weigh on market sentiment.

Ongoing geopolitical risks also remain a key upside risk, with any disruption to shipping routes potentially tightening vessel supply and supporting freight rates.

Leave a Reply