- Indian sponge iron prices range-bound

- Thermal coal port stocks rise w-o-w

South African thermal coal sentiment remained weak during the week despite continued softening in prices across key Indian ports. Lower imported coal prices failed to stimulate fresh buying interest as consumers continued favouring domestic coal, which remained readily available at more competitive rates. Market participants reported limited enquiries and negligible spot activity, with most buyers remaining on the sidelines amid weak steel market fundamentals and expectations of further corrections in imported coal offers.

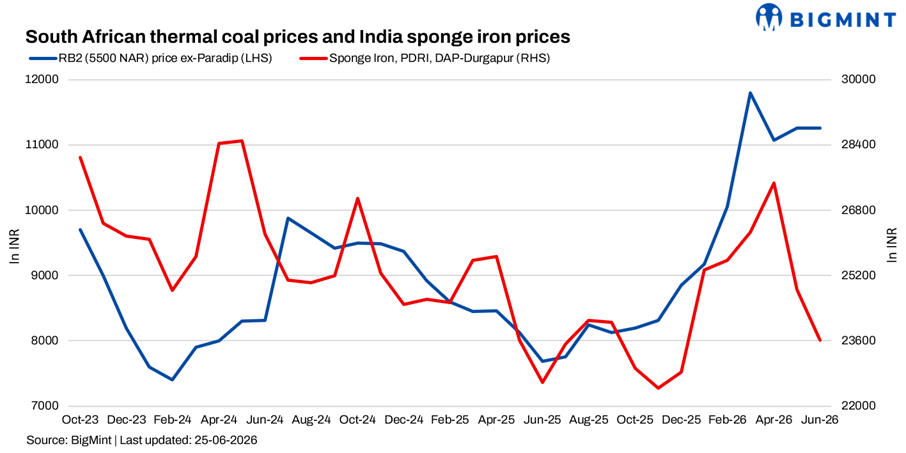

As per BigMint’s assessment as on 25 June 2026, ex-Paradip RB2 (5,500 NAR) declined by INR 250/t w-o-w to INR 10,800/t, while RB3 (4,800 NAR) fell by INR 100/t to INR 9,600/t. At Vizag, both RB2 and RB3 declined by INR 200/t w-o-w to INR 10,600/t and INR 9,500/t, respectively.

India’s coal inventories at major ports increased by 11.4% w-o-w to 15.07 mnt in week 25 from 14.72 mnt in week 24, supported by higher arrivals and slower evacuation. The increase reflected subdued import consumption and comfortable stock availability across major consuming regions.

Lower prices fail to attract buyers

Market participants noted that enquiry levels remained largely unchanged despite the recent correction in South African coal prices. Traders reported that most consumers continued delaying purchases as domestic coal remained available at significantly lower rates.

The market also witnessed a persistent gap between buyer expectations and seller offers. FOB RBCT offers for 5,500 NAR coal were heard at $89.5-92/t, while buyers were bidding closer to $85-86/t. Similarly, 4,800 NAR coal offers were reported at $70-72.5/t FOB RBCT against bids of $68-69/t.

On a CFR India basis, offers for 5,500 NAR coal were heard at $112-116/t, while 4,800 NAR coal offers were reported at $93-95/t. Despite softer offers, market participants indicated that buyers remained reluctant to commit volumes, anticipating further downside in prices.

Domestic coal continues to dominate

Domestic coal remained the biggest challenge for imported coal suppliers. BigMint assessed 5,000 GCV coal stable at INR 5,500/t, while 4,500 GCV coal remained unchanged at INR 4,050/t w-o-w.

Participants highlighted that Coal India subsidiaries continued conducting frequent auctions during June, offering substantial volumes into the market. Although auction absorption rates remained relatively low, with around 20-50% of offered quantities getting sold in several auctions, buyers continued securing their requirements through domestic channels. Select grades continued attracting decent premiums, while others cleared near base prices, reflecting adequate coal availability and the absence of supply concerns.

The comfortable domestic supply situation reduced the urgency for imported coal procurement and kept buying activity largely requirement-based.

Sponge iron market shows early signs of improvement

The sponge iron market performed relatively better during the week compared with previous weeks. PDRI DAP-Durgapur prices remained stable w-o-w at INR 23,600/t.

Market participants reported an improvement in enquiries and fresh bookings, resulting in better order volumes. Demand from the finished steel segment also improved, supporting sponge iron consumption and helping sentiment recover modestly.

However, participants noted that the improvement was not yet sufficient to trigger meaningful imported coal purchases. Most sponge iron producers continued relying on domestic coal due to its cost advantage and readily available supply.

Market awaits post-monsoon recovery

Market participants believe the recent geopolitical improvement has not yet been reflected in Indian buying behaviour. While global freight and energy market sentiment has softened, consumers continue focusing on domestic coal procurement and immediate operational requirements.

Traders indicated that the market could remain subdued throughout the monsoon season, particularly if domestic coal supplies remain uninterrupted. Imported coal demand is expected to improve only if domestic coal movement slows during heavy rainfall or if consumers face supply disruptions.

For now, weak steel market fundamentals, comfortable domestic coal availability and the continuing bid-offer disparity are keeping market activity limited despite lower South African coal prices.

Leave a Reply