- LME zinc remains rangebound w-o-w as inventory fluctuations offset demand optimism

- Prices recover from mid-week weakness while Chinese holiday period tempers market activity

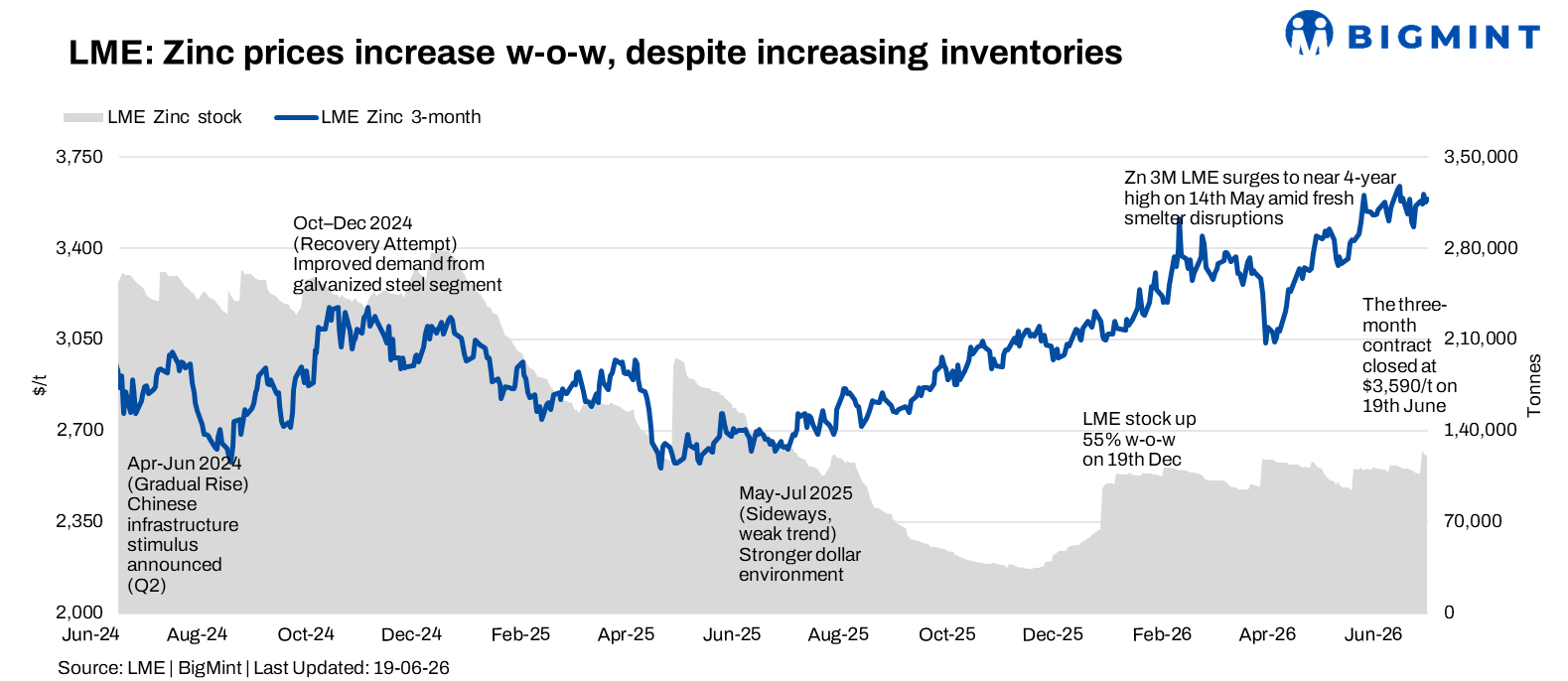

London Metal Exchange (LME) zinc prices traded within a narrow range during the week ended 19 June 2026 as market participants balanced improving buying interest against fluctuating exchange inventories and ongoing uncertainty surrounding Chinese demand. While prices witnessed periods of volatility during the reporting week, the market remained broadly resilient and closed marginally higher compared with the previous week.

On a w-o-w basis, LME zinc cash settlement prices increased slightly by 0.8% to $3,584.5/t on 19 June from $3,557/t recorded on 12 June. Despite intermittent corrections, zinc continued to trade at elevated levels, supported by healthy physical market fundamentals and expectations of balanced supply conditions.

Price trends

LME zinc cash settlement prices opened the week at $3,562/t on 15 June and eased to $3,550/t on 16 June amid cautious sentiment across the base metals complex.

Buying interest strengthened during the middle of the week, pushing prices higher to $3,592/t on 17 June, the highest level of the reporting period. However, profit-booking emerged thereafter, resulting in a slight correction to $3,565/t on 18 June before prices recovered to close at $3,584.5/t on 19 June.

The three-month contract mirrored movements in the cash market. Prices rose from $3,582/t on 15 June to a weekly high of $3,607/t on 17 June before easing to $3,577/t on 18 June and recovering to $3,590/t by week-end.

The relatively firm forward curve continued to indicate confidence in near-term zinc fundamentals despite short-term price volatility.

Inventory analysis

LME zinc inventories displayed significant fluctuations during the reporting week.

Stocks declined marginally from 107,750 t on 12 June to 107,150 t on 15 June before witnessing a sharp increase to 124,550 t on 16 June, largely reflecting fresh warehouse inflows.

Subsequently, inventories resumed their downward trend, falling to 122,375 t on 17 June and 120,900 t on 18 June before edging higher again to 123,775 t on 19 June.

Overall, exchange inventories increased by 16,025 t w-o-w. While the rise in stocks weighed on bullish sentiment at times, inventory levels remain relatively moderate by historical standards and continue to be monitored closely by market participants.

MCX zinc trends (15-19 June)

On the Multi Commodity Exchange (MCX), zinc futures traded within a broad range, broadly tracking movements in overseas markets.

The June contract settled at INR 369,900/t on 15 June before declining to INR 366,200/t on 16 June amid weaker global cues.

Prices subsequently recovered, advancing to INR 370,100/t on 17 June and INR 370,700/t on 18 June, supported by stronger LME performance. However, profit-booking ahead of the week-end led prices lower, with the contract settling at INR 366,500/t on 19 June.

Open interest declined steadily from 2,388 lots on 15 June to 1,922 lots on 19 June, indicating position unwinding and cautious participation amid ongoing market uncertainty.

Trading activity remained healthy as domestic consumers largely continued need-based procurement while monitoring international price movements and domestic producer pricing.

SHFE zinc trends

On the Shanghai Futures Exchange (SHFE), zinc prices remained relatively stable during the week despite mixed sentiment surrounding Chinese industrial demand.

SHFE zinc stood at $3,394/t on both 15 and 16 June before recovering to $3,455/t on 17 June and further to $3,466/t on 18 June.

Prices eased marginally to $3,455/t on 19 June as participants reduced activity ahead of the Dragon Boat Festival holiday period from 19-21 June.

The stable trend suggests that while immediate demand signals remain mixed, underlying market fundamentals continue to provide support to zinc prices.

Market updates

Market sentiment remained mixed during the week. While the mid-week recovery in LME zinc prices reflected renewed buying interest at lower levels, the sharp increase in exchange inventories following fresh warehouse inflows capped further upside. Domestic consumers largely continued need-based procurement, with adequate material availability limiting urgency for aggressive restocking.

In China, market activity remained cautious amid uncertainty over near-term demand prospects and the Dragon Boat Festival holiday period (19-21 June), which reduced trading activity towards the week-end. Nevertheless, zinc prices remained supported by resilient physical demand from galvanizing and infrastructure-linked sectors, helping the market maintain levels above the key $3,500/t support range.

Outlook

BigMint expects LME zinc prices to remain broadly rangebound in the near term as stable physical demand and resilient market fundamentals offset pressure from higher exchange inventories.

The market is likely to find immediate support in the $3,500-3,550/t range, while resistance is seen around $3,620-3,650/t. Developments in Chinese demand following the holiday period and inventory movements across LME warehouses will remain key indicators for future price direction.

Leave a Reply