- US-Iran deal lowers oil prices, weighs on freight sentiment

- Stronger Capesize fixtures lift BDI from 6-week low

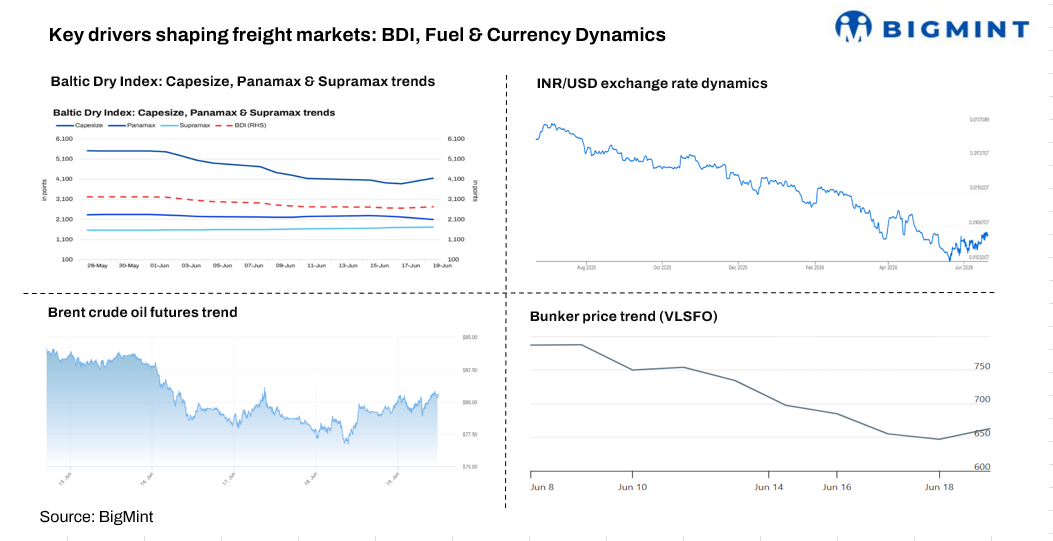

The global dry bulk freight market has experienced heightened volatility in recent weeks as the discussions regarding the resolution of the conflict between the United States and Iran influenced sentiment across commodity and shipping markets.

This week’s agreement has raised expectations of smoother oil flows through the Strait of Hormuz, a critical maritime chokepoint through which nearly one-fifth of global oil trade passes, easing concerns over supply disruptions and operational risks for shipowners.

The impact was immediately visible in energy markets. Brent crude oil prices, which had touched $125/barrel (bbl) during the peak of geopolitical uncertainty, fell sharply to around $78/bbl on 17 June, marking their lowest level in nearly three months. The decline reflected expectations of increased Middle Eastern oil exports and lower risk premiums, leading to a reduction in bunker fuel costs and voyage expenses across the shipping sector.

Following suit, bunker prices fell by $46/tonne (t) w-o-w to $667/t as of 19 June, compared with $713/t a week earlier, tracking softer fuel oil values and lower crude oil prices despite ongoing geopolitical uncertainties.

Freight markets initially came under pressure following the US-Iran agreement, as easing geopolitical risks and lower bunker fuel costs reduced the risk premium embedded in freight rates. At the same time, ample vessel availability and subdued cargo demand weighed on sentiment, particularly in the Pacific basin. The Australia-China iron ore route weakened to its lowest level in more than two months, while India-China freight rates also declined sharply. Consequently, the Baltic Dry Index (BDI) fell to a more than six-week low of 2,720 points on 15 June 2026, driven largely by continued weakness in the Capesize segment.

However, market conditions shifted rapidly in the following days. Limited vessel availability and stronger fixture activity at higher levels on key Australia-China iron ore routes improved vessel utilisation and boosted Capesize earnings, triggering a sharp rebound in freight levels. The recovery lifted the Baltic Dry Index to a one-week high of 2,722 points on 19 June, highlighting the market’s sensitivity to underlying supply-demand dynamics.

Market participants noted that despite the influence of geopolitics and fuel prices, freight fundamentals continue to be driven primarily by cargo demand and vessel availability. A market source said, “Demand is improving, but vessel supply remains the critical factor.” The comment reflects the current market environment, where fluctuations in prompt tonnage availability are having a greater impact on freight direction than changes in macroeconomic or geopolitical sentiment.

As a result, while the US-Iran resolution has eased operational concerns and reduced voyage costs, freight rates are likely to remain volatile, with the balance between cargo demand and vessel supply continuing to dictate market movements across key dry bulk routes.

Leave a Reply