- Weak demand continues to pressure coated steel prices

- Galvalume gains on thinner-gauge supply constraints

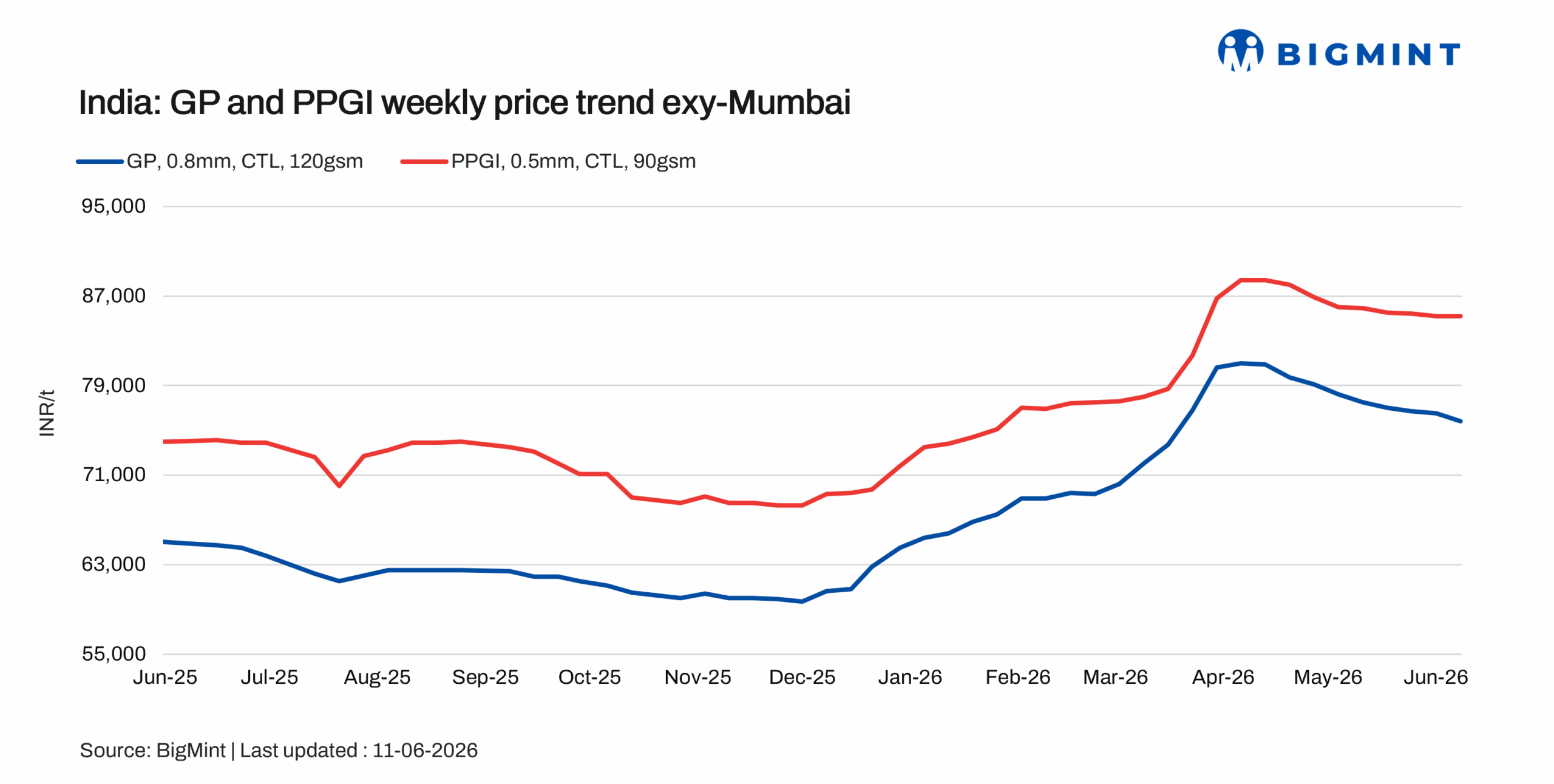

The Indian coated flat steel market remained under pressure during the assessment period, with prices declining by INR 600-700/t across major markets amid weak demand from key consuming sectors. Buying activity for galvanised products remained sluggish, with most customers limiting purchases to immediate requirements.

However, the colour-coated steel (PPGI) segment witnessed relatively better demand, supported by pre-monsoon procurement from roofing and infrastructure-related consumers. Market participants noted that overall inventory levels remain comfortable at around 1.5 months, although the availability of thinner gauge material has tightened, resulting in supply shortages in select specifications.

Current market prices stood at INR 74,300-78,500/t for GP, INR 83,300-85,200/t for PPGI, and INR 87,000-90,500/t for Galvalume.

Looking ahead, market participants expect overall demand to remain rangebound in GP after the pre-monsoon buying cycle eases. While ample inventories in are likely to keep the broader market under pressure, shortages in thinner gauges in BGL may continue to provide support to prices in select segments.

Price Update:

Galvanised Plain (GP) coil (exy-Mumbai, India; 0.8mm / CTL, 120 GSM, IS 277) was assessed at INR 75,800/t, down by INR 700/t w-o-w amid weak demand and subdued buying activity. Tradable offers were heard in the range of INR 75,500-76,500/t.

Pre-painted Galvanised Iron (PPGI) (exy-Mumbai, India; 0.5mm / CTL, 90 GSM, IS 14246) was assessed at INR 85,200/t, stable w-o-w. Offers were reported in the range of INR 84,500-86,500/t, with demand supported to some extent by pre-monsoon procurement, although overall booking activity remained moderate.

Galvalume/Bare Galvalume (BGL) (exy-Mumbai, India; 0.5mm / CTL, 1220mm, AZ150) was assessed at INR 90,500/t, up by INR 1,200/t w-o-w, supported by tighter availability, particularly in thinner gauges. Tradable offers were indicated in the range of INR 88,500-91,000/t, while overall market activity remained selective.

Raw material prices

India’s zinc ingot (99.995%) prices declined w-o-w by around INR 7,700/t ($90/t) to INR 376,300/t ($4,395/t) ex-Delhi on 9 June 2026, pressured by softer global zinc prices and weaker producer pricing. Demand from galvanisers and alloy manufacturers remained largely need-based, with buyers restricting purchases to immediate requirements amid sluggish downstream consumption.

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) in Mumbai edged down by INR 100/t ($1/t) w-o-w to INR 58,300/t ($611/t) as of 9 June, compared with INR 58,400/t ($612/t) on 2 June, reflecting continued weakness in the domestic flat steel market.

Meanwhile, BigMint’s benchmark assessment for CRC (IS513, Gr O, 0.9 mm/CTL) remained stable at INR 65,200/t ($684/t) over the same period. Both assessments are ex-Mumbai and exclude 18% GST.

Market update

The Indian coated flat steel market remained sluggish during the assessment period as weak end-user demand continued to weigh on trading activity across major consuming regions. According to market participants, the key reason behind the subdued demand was the relatively higher prices maintained by mills and the absence of any meaningful price support or additional discounts, prompting buyers to defer fresh purchases and procure only against immediate requirements.

Market sentiment remained cautious, with most participants adopting a wait-and-watch approach in anticipation of more competitive pricing from producers. While demand for galvanised products remained weak, the colour-coated (PPGI) segment witnessed a modest improvement in enquiries and buying activity, supported by selective demand from roofing and project-related applications.

The Galvalume (BGL) segment also witnessed upward price momentum during the week, primarily due to limited material availability, particularly in thinner gauges. The tighter supply supported prices despite the broader weakness in the coated flat steel market.

Overall, weak end-user consumption and cautious buying sentiment continued to keep the coated flat steel market under pressure. However, relatively better demand in the PPGI segment and supply tightness in Galvalume provided some support to select product categories.

Outlook

The coated flat steel market is expected to remain under pressure in the near term as weak end-user demand and cautious purchasing behaviour continue to outweigh any support from raw material costs. Unless mills offer additional price support or discounts, buying activity is likely to remain limited, with customers continuing to procure only against immediate requirements.

However, the PPGI segment may continue to perform relatively better than GP, supported by project-related demand and seasonal requirements. At the same time, limited availability of thinner-gauge Galvalume is expected to keep prices firm in that segment, even as the broader coated steel market remains subdued. Overall, the market is likely to witness range-bound pricing, with selective strength in supply-constrained products and continued pressure on mainstream coated grades.

Leave a Reply