- Australian and Brazilian loadings fuel rebound in shipments

- Capesize weakness tempers freight market sentiment

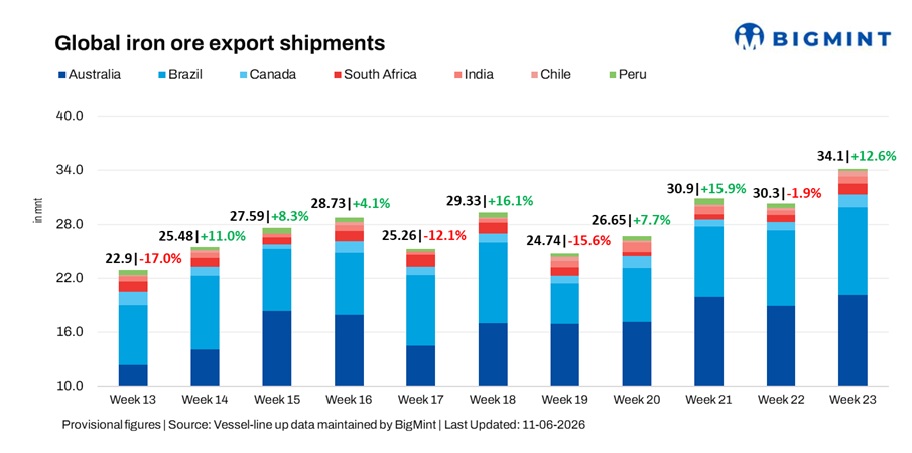

Global iron ore export shipments rose 12.6% w-o-w to 34.1 million tonnes (mnt) in the week ended 5 June, compared with 30.3 mnt a week earlier, according to BigMint data. The latest week’s volume marks the highest level recorded so far in CY’26, surpassing the previous peak of 33.7 mnt registered in the first week of January 2026.

The increase reflected stronger loadings across most major exporting regions, with gains from Australia and Brazil leading the recovery.

Australian exports recovered on stronger Dampier and Port Hedland loadings despite maintenance activity, while robust Vale programmes supported Brazilian shipments. Improved rail operations supported shipments from Canada and South Africa, and better cargo availability aided Indian exports. Peru remained the only major exporter to record a decline amid cargo constraints.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 12.4 mnt, Port Walcott 3.8 mnt, and Dampier 3.4 mnt. Rio Tinto exported 7.2 mnt, BHP shipped 6.6 mnt, and FMG exported 4.1 mnt. China remained the largest importer at 17.6 mnt, followed by South Korea (1.2 mnt).

- Brazil: Ponta da Madeira handled 4.4 mnt, Itaguai 2.1 mnt, and Tubarao 1.5 mnt. CSN & Vale exported 7.9 mnt, with China importing 5.5 mnt.

- Canada: Sept-Iles handled 0.9 mnt and Port Cartier 0.5 mnt. IOC exported 0.5 mnt, while AMNS and Guinea & Nimba Mines shipped 0.5 mnt each. China imported 0.4 mnt, followed by France (0.3 mnt).

- South Africa: Saldanha handled 1.2 mnt. China remained the largest importer at 0.6 mnt, followed by Japan (0.3 mnt).

- India: Paradip handled 0.3 mnt and Dhamra 0.3 mnt. China imported 0.5 mnt.

- Chile: Caldera and Totoralillo each handled 0.2 mnt. China imported 0.4 mnt, followed by Japan (0.2 mnt).

- Peru: San Nicolas handled 0.2 mnt. Shougang Hierro exported 0.2 mnt, with China importing 0.04 mnt.

Capesize softness offsets Supramax resilience

Dry bulk iron ore freight markets displayed mixed trends during the week. Capesize sentiment weakened amid lower fixture activity, cautious chartering interest, and declining iron ore futures, pressuring key long-haul routes. Softer demand and ample vessel availability in the Pacific basin further weighed on the segment.

In contrast, the Supramax market remained relatively resilient, supported by steady minor bulk cargo demand and improved vessel utilisation.

Outlook

Global iron ore shipments are expected to remain supported by healthy loading programmes across key exporting regions, though maintenance, weather, and Chinese steel demand trends will continue to influence trade flows. Freight sentiment is likely to remain mixed amid weak Capesize and resilient Supramax markets.

Leave a Reply