- Aluminium leads LME declines despite continued inventory tightness

- China’s export surge highlights ongoing global supply disruptions

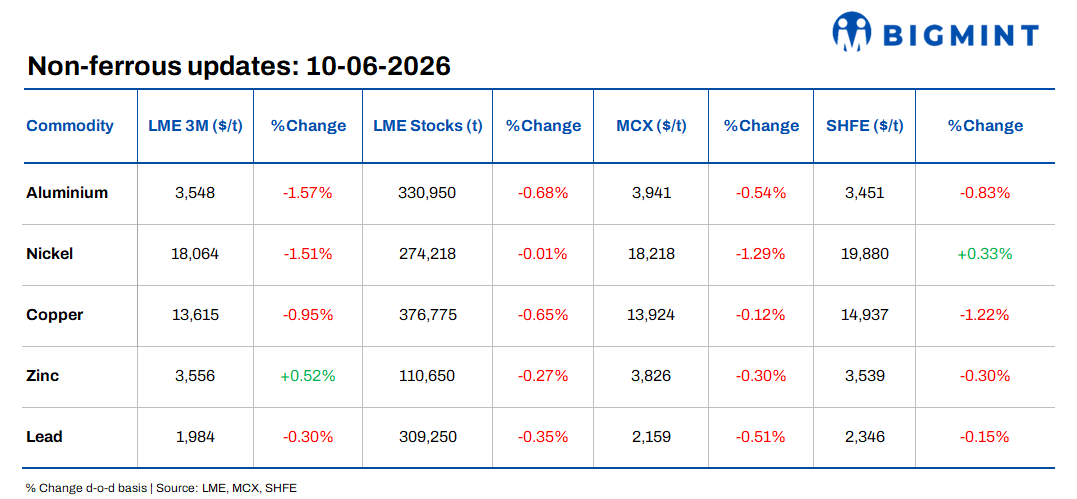

Base metals on the London Metal Exchange (LME) traded lower on 9 June 2026 amid subdued market sentiment and continued pressure across major exchanges. Aluminium recorded the steepest decline among key non-ferrous metals, falling 1.57% d-o-d to $3,548/t, followed by nickel, which dropped 1.51% to $18,064/t. Lead also edged down 0.3% to $1,984/t, while copper declined by 0.95% to $13,615/t. In contrast, zinc was the only gainer, rising 0.52% d-o-d to $3,556/t.

On the inventory side, aluminium stocks registered the sharpest decline, falling 0.68% d-o-d to 330,950 t, followed by copper inventories, which slipped 0.65% to 376,775 t. Lead and zinc stocks also eased by 0.35% and 0.27% to 309,250 t and 110,650 t, respectively, while nickel inventories remained nearly flat, down marginally by 0.01% to 274,218 t, indicating continued tightness in LME warehouse availability..

Domestic market overview

India’s non-ferrous scrap prices traded largely steady d-o-d on 10 June. Aluminium tense scrap (loose), ex-Delhi, remained unchanged at INR 304,000/t, while ex-Chennai prices were also stable at INR 307,000/t, indicating balanced buying activity across regional markets.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, increased by INR 15,000/t, or 1.2%, d-o-d to INR 1,260,000/t from INR 1,245,000/t, supported by improved copper market sentiment and firmer domestic trade activity.

Other updates

China’s aluminium exports jump 16% y-o-y in May

China’s aluminium exports rose 16% y-o-y and 6% m-o-m in May to around 630,000 t, according to data from the General Administration of Customs of China. The increase was driven by tighter global aluminium availability following supply disruptions and shipment constraints linked to the ongoing Middle East conflict.

During January-May, China’s cumulative aluminium exports increased 10.5% y-o-y to nearly 2.7 mnt. Chinese smelters reportedly operated at elevated utilisation rates to capitalise on firmer international prices and widening supply gaps in overseas markets.

Copper eases as macro concerns offset tariff-driven support

LME copper prices edged lower on 10 June 2026 as ongoing macroeconomic concerns and heightened Middle East tensions weighed on market sentiment, despite continued support from expectations of potential US copper import tariffs. Benchmark three-month copper on the LME declined 0.95% d-o-d to $13,615/t, while the most-active SHFE copper contract slipped 0.38% to RMB 104,010/t.

Rising oil prices following renewed US strikes on Iran intensified concerns over higher energy costs and weaker manufacturing activity, a key demand sector for copper. At the same time, stronger-than-expected US jobs data boosted the dollar and reinforced expectations of a possible Federal Reserve rate hike later this year, pressuring industrial metals sentiment.

However, downside pressure remained limited amid expectations of proposed US tariffs on copper imports and continued declines in LME copper inventories since 28 May, indicating ongoing tightness in exchange warehouse stocks.

Oil rebounds nearly 1% on tightening supply outlook

Global crude oil prices rose nearly 1% on 10 June 2026 after fresh US military strikes against Iran reignited concerns over potential supply disruptions in the Middle East. Brent crude futures increased 0.7% to around $91/bbl, while WTI crude rose to nearly $88.8/bbl, recovering from the previous session’s seven-week low.

Market sentiment strengthened amid fears of further escalation around the Strait of Hormuz, a key global oil transit route, alongside continued tightness in physical supply. According to industry data, US crude inventories declined by over 9 mn barrels for the eighth consecutive week, indicating tightening availability ahead of the peak summer demand season.

The rise in crude prices also added pressure across industrial commodities markets, as elevated energy costs could increase production expenses for energy-intensive sectors, including base metals and aluminium smelting operations.

Leave a Reply