- Capesize weakness continues to weigh on BDI

- Smaller vessel strength may limit downside

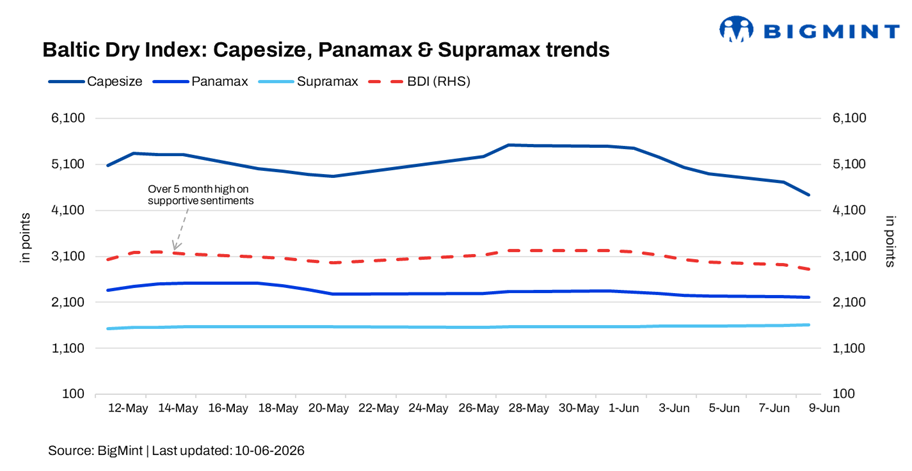

The Baltic Exchange’s Dry Bulk Index (BDI) fell by 3.4% d-o-d (98 points) to 2,818 points on 9 June 2026, reflecting a bearish overall market sentiment. It has been on a consistent downward trajectory since 28 May, indicating a sustained cooling in dry bulk freight sentiment.

The decline was primarily driven by weakness in the Capesize segment, which overshadowed the relatively stable performance of Panamax vessels and continued strength in the Supramax market.

Segment-wise performance

- Capesize: The Capesize index dropped by 5.9% (278 points) to 4,441 points, indicating a bearish sentiment amid softer iron ore cargo demand, particularly on major Brazil-China and Australia-China routes. Reduced fixture activity and easing freight negotiations pressured earnings in the segment.

- Panamax: The Panamax index declined marginally by 0.6% (13 points) to 2,205 points, reflecting a subdued-to-neutral sentiment. Grain and coal cargo demand remained steady, but limited fresh inquiries and cautious chartering activity capped rate improvements.

- Supramax: The Supramax index increased by 1.1% (18 points) to 1,614 points, signaling a bullish sentiment. Strong regional demand for minor bulks such as steel products, fertilizers, cement, and agricultural commodities supported vessel utilization and freight rates across key trading regions.

Outlook

The Baltic Dry Index is expected to remain under pressure in the near term, as persistent weakness in the Capesize segment continues to outweigh gains in smaller vessel segment.

However, support from Panamax and Supramax markets could help stabilize the index, with any meaningful recovery likely dependent on stronger iron ore shipment volumes and improved chartering activity on key long-haul routes.

Leave a Reply